Stay informed

Stay informed with what’s going on. Browse posts that might be helpful to you or check out an event happening in your area. Come back regularly as this page is kept up-to-date with a lot of relevant information.

Life is unpredictable. What if you got an unexpected diagnosis? I'm here to help! Learn how critical illness insurance could help protect your finances.

Life is unpredictable. What if you got an unexpected diagnosis? I'm here to help! Learn how critical illness insurance could help protect your finances.

Many business owners reinvest every dollar back into their business. Having a strategic plan helps you decide what to reinvest and what to set aside for your future.

Book a Sun Life One Plan conversation to map out your next steps. https://advisor.sunlife.ca/hao.li1/

#SunLifeOnePlan

Book a Sun Life One Plan conversation to map out your next steps. https://advisor.sunlife.ca/hao.li1/

#SunLifeOnePlan

Many business owners reinvest every dollar back into their business. Having a strategic plan helps you decide what to reinvest and what to set aside for your future.

Book a Sun Life One Plan conversation to map out your next steps. https://advisor.sunlife.ca/hao.li1/

#SunLifeOnePlan

Book a Sun Life One Plan conversation to map out your next steps. https://advisor.sunlife.ca/hao.li1/

#SunLifeOnePlan

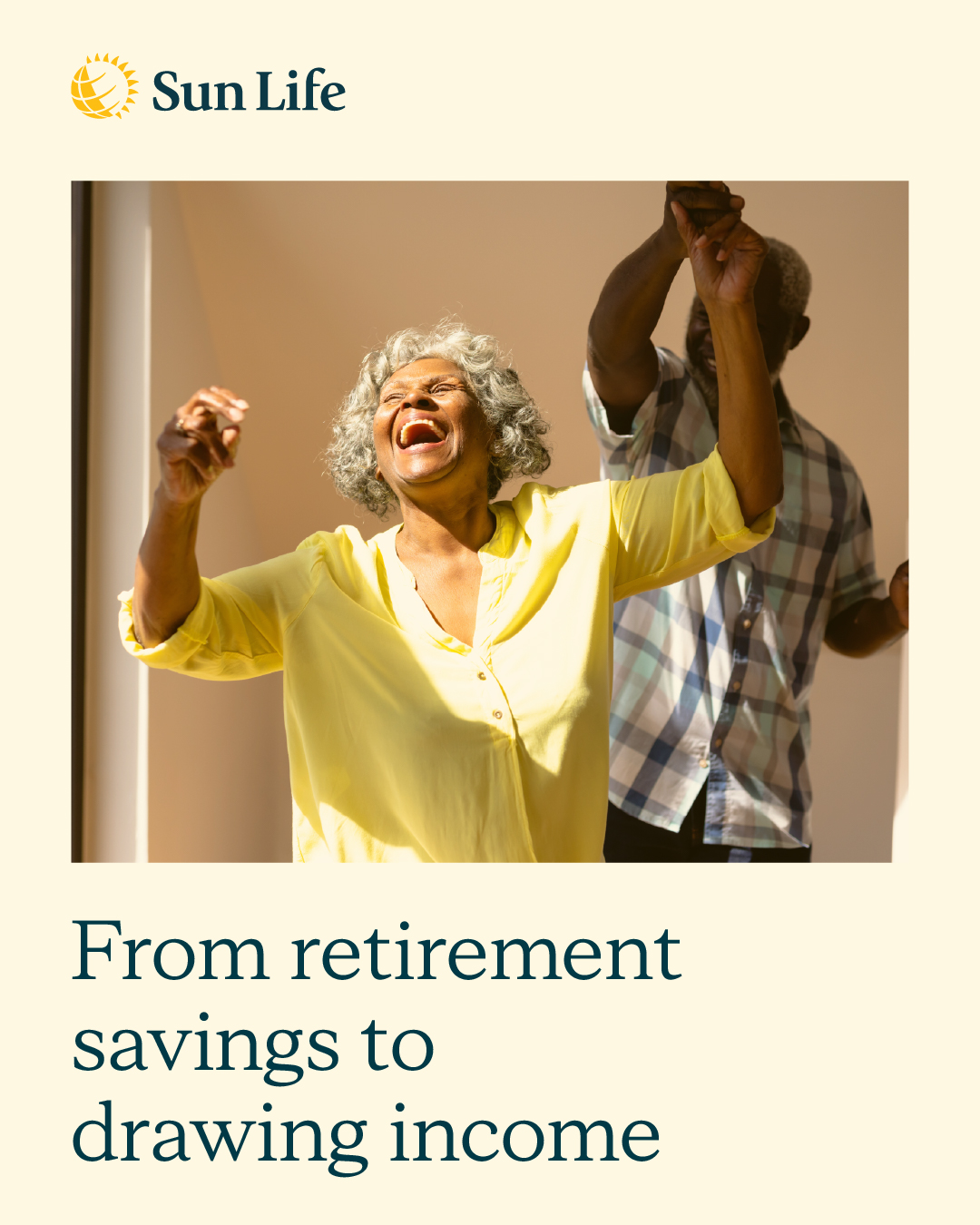

Retirement isn’t a number — it’s a roadmap. We’ll outline how your savings can become a reliable source of income. Together, let's build your withdrawal strategy.

#RetirementStrategy #Retirement #SunLife

#RetirementStrategy #Retirement #SunLife

Retirement isn’t a number — it’s a roadmap. We’ll outline how your savings can become a reliable source of income. Together, let's build your withdrawal strategy.

#RetirementStrategy #Retirement #SunLife

#RetirementStrategy #Retirement #SunLife

报税季不仅仅是提交申报表——更重要的是提前做好规划。从 RRSP (注册退休储蓄计划)供款到收入分拆策略,现在就可以采取行动,为明年及未来更好地规划您的财务。

欢迎与我们联系,了解哪些策略最适合您。

欢迎与我们联系,了解哪些策略最适合您。

报税季不仅仅是提交申报表——更重要的是提前做好规划。从 RRSP (注册退休储蓄计划)供款到收入分拆策略,现在就可以采取行动,为明年及未来更好地规划您的财务。

欢迎与我们联系,了解哪些策略最适合您。

欢迎与我们联系,了解哪些策略最适合您。

From health spending accounts to enhanced benefits, there are ways to cover what provincial plans don't — and sometimes save on taxes too. Let's explore what fits your needs and budget.

From health spending accounts to enhanced benefits, there are ways to cover what provincial plans don't — and sometimes save on taxes too. Let's explore what fits your needs and budget.

Tax season isn't just about filing — it's about planning ahead. From RRSP contributions to income splitting strategies, there are things you can do now to better position your finances for next year and beyond.

Get in touch to find out what strategies work best for you. https://advisor.sunlife.ca/hao.li1/

Get in touch to find out what strategies work best for you. https://advisor.sunlife.ca/hao.li1/

Tax season isn't just about filing — it's about planning ahead. From RRSP contributions to income splitting strategies, there are things you can do now to better position your finances for next year and beyond.

Get in touch to find out what strategies work best for you. https://advisor.sunlife.ca/hao.li1/

Get in touch to find out what strategies work best for you. https://advisor.sunlife.ca/hao.li1/

A withdrawal strategy can help create dependable income while helping you manage risk. Let’s chat about income planning basics that fit your needs. https://advisor.sunlife.ca/hao.li1/

A withdrawal strategy can help create dependable income while helping you manage risk. Let’s chat about income planning basics that fit your needs. https://advisor.sunlife.ca/hao.li1/

When it comes to your savings, don’t let common TFSA mistakes tip you overboard. Read this article on the 4 mistakes to avoid and then let’s connect to discuss how I can help you.

When it comes to your savings, don’t let common TFSA mistakes tip you overboard. Read this article on the 4 mistakes to avoid and then let’s connect to discuss how I can help you.

Tax time is also estate-planning time. Reviewing your return helps ensure beneficiary designations, ownership structures and transfer plans align with your wishes, while reducing potential taxes on asset transfers.

Tax time is also estate-planning time. Reviewing your return helps ensure beneficiary designations, ownership structures and transfer plans align with your wishes, while reducing potential taxes on asset transfers.

Winter is still here, but your financial wellbeing can shine. Now's the perfect time to review your savings and investments and help ensure you're on track for growth. Let’s connect to explore Sun Life's diverse wealth solutions that we can tailor to your goals.

https://advisor.sunlife.ca/hao.li1

https://advisor.sunlife.ca/hao.li1

Winter is still here, but your financial wellbeing can shine. Now's the perfect time to review your savings and investments and help ensure you're on track for growth. Let’s connect to explore Sun Life's diverse wealth solutions that we can tailor to your goals.

https://advisor.sunlife.ca/hao.li1

https://advisor.sunlife.ca/hao.li1

Did you know that payout annuities can help provide financial predictability in retirement?

Benefits include:

• Reliable monthly income

• Protection against market volatility

• No investment management required

• Peace of mind planning

Discover how guaranteed income streams can complement retirement portfolios and provide stability. Let’s chat! https://advisor.sunlife.ca/hao.li1

Benefits include:

• Reliable monthly income

• Protection against market volatility

• No investment management required

• Peace of mind planning

Discover how guaranteed income streams can complement retirement portfolios and provide stability. Let’s chat! https://advisor.sunlife.ca/hao.li1

Did you know that payout annuities can help provide financial predictability in retirement?

Benefits include:

• Reliable monthly income

• Protection against market volatility

• No investment management required

• Peace of mind planning

Discover how guaranteed income streams can complement retirement portfolios and provide stability. Let’s chat! https://advisor.sunlife.ca/hao.li1

Benefits include:

• Reliable monthly income

• Protection against market volatility

• No investment management required

• Peace of mind planning

Discover how guaranteed income streams can complement retirement portfolios and provide stability. Let’s chat! https://advisor.sunlife.ca/hao.li1

Did you know you can still contribute to your 2025 RRSP before March 2, 2026? Get in touch with me to find out if that’s a good idea for you!

Did you know you can still contribute to your 2025 RRSP before March 2, 2026? Get in touch with me to find out if that’s a good idea for you!

Do you want to keep more money in your business? Let's talk about smart tax strategies that fit your company to make it more tax efficient. 📊

Ready to save? Visit my website to set up time to chat. https://advisor.sunlife.ca/hao.li1

Ready to save? Visit my website to set up time to chat. https://advisor.sunlife.ca/hao.li1

Do you want to keep more money in your business? Let's talk about smart tax strategies that fit your company to make it more tax efficient. 📊

Ready to save? Visit my website to set up time to chat. https://advisor.sunlife.ca/hao.li1

Ready to save? Visit my website to set up time to chat. https://advisor.sunlife.ca/hao.li1

Feeling the winter blahs? You're not alone. There’s still time to prioritize your mental wellbeing this winter. Many Sun Life plans offer coverage for mental health services. Let's discuss how your insurance can support you.

Feeling the winter blahs? You're not alone. There’s still time to prioritize your mental wellbeing this winter. Many Sun Life plans offer coverage for mental health services. Let's discuss how your insurance can support you.

感到冬季情绪低落?遇到这种情况的并非只有您一人。这个冬天,您仍有机会优先关注心理健康。多款永明金融计划涵盖心理健康服务。让我们探讨保险如何为您提供支持。

感到冬季情绪低落?遇到这种情况的并非只有您一人。这个冬天,您仍有机会优先关注心理健康。多款永明金融计划涵盖心理健康服务。让我们探讨保险如何为您提供支持。

Navigating life insurance options can be overwhelming. Whether finishing school, buying a first home or starting a family, finding the right plan that fits life's unique journey is essential.

We can help secure your future together. Let us know how we can help.

We can help secure your future together. Let us know how we can help.

Navigating life insurance options can be overwhelming. Whether finishing school, buying a first home or starting a family, finding the right plan that fits life's unique journey is essential.

We can help secure your future together. Let us know how we can help.

We can help secure your future together. Let us know how we can help.

Family is everything! When you meet with me, we’ll discuss how you can plan to protect them no matter what life throws at you, the expected and the unexpected.

Family is everything! When you meet with me, we’ll discuss how you can plan to protect them no matter what life throws at you, the expected and the unexpected.

Thoughtful planning ensures your assets reach the right people at the right time — with minimal tax impact.

Key considerations include:

-Estate planning strategies

-Tax-efficient wealth transfer

-Protecting family harmony

-Preserving your legacy

Start planning today for a seamless transition tomorrow. Get in touch today. https://advisor.sunlife.ca/hao.li1

Key considerations include:

-Estate planning strategies

-Tax-efficient wealth transfer

-Protecting family harmony

-Preserving your legacy

Start planning today for a seamless transition tomorrow. Get in touch today. https://advisor.sunlife.ca/hao.li1

Thoughtful planning ensures your assets reach the right people at the right time — with minimal tax impact.

Key considerations include:

-Estate planning strategies

-Tax-efficient wealth transfer

-Protecting family harmony

-Preserving your legacy

Start planning today for a seamless transition tomorrow. Get in touch today. https://advisor.sunlife.ca/hao.li1

Key considerations include:

-Estate planning strategies

-Tax-efficient wealth transfer

-Protecting family harmony

-Preserving your legacy

Start planning today for a seamless transition tomorrow. Get in touch today. https://advisor.sunlife.ca/hao.li1

Building wealth is about more than growing your money – it's about creating lasting financial security. 💖💰

Your financial wellbeing matters at every stage of life. Whether you're just starting out or well into your journey, now is the right time to take action.

Ready to connect? Let's work together to help you set achievable long-term wealth goals and build a brighter financial future.

Your financial wellbeing matters at every stage of life. Whether you're just starting out or well into your journey, now is the right time to take action.

Ready to connect? Let's work together to help you set achievable long-term wealth goals and build a brighter financial future.

Building wealth is about more than growing your money – it's about creating lasting financial security. 💖💰

Your financial wellbeing matters at every stage of life. Whether you're just starting out or well into your journey, now is the right time to take action.

Ready to connect? Let's work together to help you set achievable long-term wealth goals and build a brighter financial future.

Your financial wellbeing matters at every stage of life. Whether you're just starting out or well into your journey, now is the right time to take action.

Ready to connect? Let's work together to help you set achievable long-term wealth goals and build a brighter financial future.

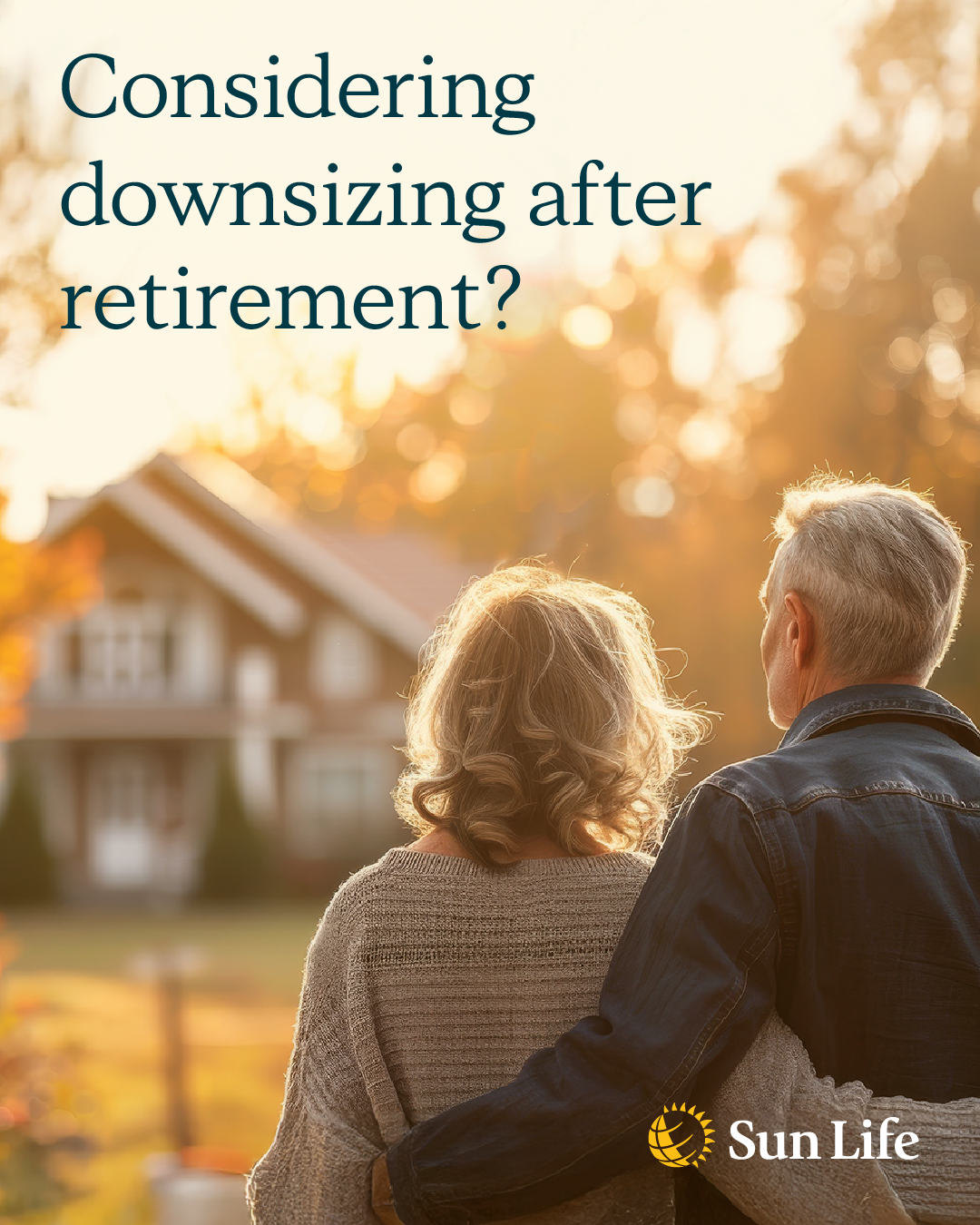

Strategic planning can help you make the most of housing transitions.

Have you considered:

-Capital gains implications?

-Mortgage protection during transition?

-Investment of home equity?

-Lifestyle considerations?

Professional advice ensures housing decisions align with your overall retirement goals. Let's discuss the financial aspects of downsizing.

#RetirementPlanning #Retirement

Have you considered:

-Capital gains implications?

-Mortgage protection during transition?

-Investment of home equity?

-Lifestyle considerations?

Professional advice ensures housing decisions align with your overall retirement goals. Let's discuss the financial aspects of downsizing.

#RetirementPlanning #Retirement

Strategic planning can help you make the most of housing transitions.

Have you considered:

-Capital gains implications?

-Mortgage protection during transition?

-Investment of home equity?

-Lifestyle considerations?

Professional advice ensures housing decisions align with your overall retirement goals. Let's discuss the financial aspects of downsizing.

#RetirementPlanning #Retirement

Have you considered:

-Capital gains implications?

-Mortgage protection during transition?

-Investment of home equity?

-Lifestyle considerations?

Professional advice ensures housing decisions align with your overall retirement goals. Let's discuss the financial aspects of downsizing.

#RetirementPlanning #Retirement

Have questions?

Here to help answer your questions, provide clarity about products and get you started on the road to achieving your goals.