Stay informed

Stay informed with what’s going on. Browse posts that might be helpful to you or check out an event happening in your area. Come back regularly as this page is kept up-to-date with a lot of relevant information.

Provincial health care will cover your treatment. What it will not cover is everything else.

Think about what a serious diagnosis actually looks like in real life. You may need weeks or months away from work. Your income drops, but your mortgage, car payment, and household bills do not.

You might need to travel to a specialist in another city. You may want access to treatments or second opinions that fall outside of what your province covers. Your partner may need to take time off to support you.

Group benefits help, but they have limits. And they do not follow you if you leave your job.

A critical illness payout gives you a tax-free lump sum to use however your situation demands.

If you want to understand what your current coverage protects, reach out. We are happy to take a look with you.

Think about what a serious diagnosis actually looks like in real life. You may need weeks or months away from work. Your income drops, but your mortgage, car payment, and household bills do not.

You might need to travel to a specialist in another city. You may want access to treatments or second opinions that fall outside of what your province covers. Your partner may need to take time off to support you.

Group benefits help, but they have limits. And they do not follow you if you leave your job.

A critical illness payout gives you a tax-free lump sum to use however your situation demands.

If you want to understand what your current coverage protects, reach out. We are happy to take a look with you.

When most people hear "critical illness insurance," they tend to picture cancer.

And well cancer is covered, it’s only part of the story.

Critical illness insurance can pay out a tax-free lump sum if you are diagnosed with a heart attack, stroke, multiple sclerosis, Parkinson's disease, kidney failure, major organ transplants, and more. Depending on the policy, you may be covered for 25 or more conditions.

When the policy pays out, that money is yours to use however you need. You can pay down debts, cover living expenses, fund treatment that you may need, or take time away from work to recover.

Most people have no idea how wide the coverage actually is until someone sits down and walks them through it.

That is exactly what we are here for. Reach out and let's talk.

And well cancer is covered, it’s only part of the story.

Critical illness insurance can pay out a tax-free lump sum if you are diagnosed with a heart attack, stroke, multiple sclerosis, Parkinson's disease, kidney failure, major organ transplants, and more. Depending on the policy, you may be covered for 25 or more conditions.

When the policy pays out, that money is yours to use however you need. You can pay down debts, cover living expenses, fund treatment that you may need, or take time away from work to recover.

Most people have no idea how wide the coverage actually is until someone sits down and walks them through it.

That is exactly what we are here for. Reach out and let's talk.

Staying the course in a volatile market

Watch video

Most people put off critical illness insurance because they feel fine right now. That is exactly the wrong time to wait.

The younger and healthier you are when you apply, the lower your premiums are locked in at.

A 35-year-old in good health will pay significantly less than a 45-year-old applying for the same coverage. And if a health condition shows up between now and when you finally decide to apply, you may not qualify at all.

Critical illness insurance is one of those things that is easy to get when you do not need it, and hard to get when you do.

If you have been putting this off, let's have a quick conversation. Reach out and we can walk through what coverage might look like for you.

The younger and healthier you are when you apply, the lower your premiums are locked in at.

A 35-year-old in good health will pay significantly less than a 45-year-old applying for the same coverage. And if a health condition shows up between now and when you finally decide to apply, you may not qualify at all.

Critical illness insurance is one of those things that is easy to get when you do not need it, and hard to get when you do.

If you have been putting this off, let's have a quick conversation. Reach out and we can walk through what coverage might look like for you.

The Case for Global Funds: Risk-adjusted Return, The Sharpe Ratio

Watch video

Most people think of Critical Illness insurance as a safety net for the unexpected, and it is. But there is a feature that not enough people are taking advantage of: the Return of Premium option.

How it works is that you pay your premiums over the life of your policy. If you never make a claim, you get that money back.

Why this matters:

• You are creating a structured savings plan with a built-in safety net

• If a critical illness like cancer, a heart attack, or stroke occurs, you receive a tax-free lump sum to use however you need

• If you stay healthy and never claim, your premiums are returned to you at expiry, often at age 65 or at the end of the term

• Unlike a traditional savings account, this money is set aside and not easily touched, making it a true forced savings vehicle for people who find it hard to save consistently

The bottom line is that you are either protecting your financial future from a health crisis, or you are getting your money back. There is no losing scenario.

If you want to understand how a Return of Premium rider could fit into your overall financial plan, reach out and we would be happy to walk you through the numbers.

How it works is that you pay your premiums over the life of your policy. If you never make a claim, you get that money back.

Why this matters:

• You are creating a structured savings plan with a built-in safety net

• If a critical illness like cancer, a heart attack, or stroke occurs, you receive a tax-free lump sum to use however you need

• If you stay healthy and never claim, your premiums are returned to you at expiry, often at age 65 or at the end of the term

• Unlike a traditional savings account, this money is set aside and not easily touched, making it a true forced savings vehicle for people who find it hard to save consistently

The bottom line is that you are either protecting your financial future from a health crisis, or you are getting your money back. There is no losing scenario.

If you want to understand how a Return of Premium rider could fit into your overall financial plan, reach out and we would be happy to walk you through the numbers.

Most people think of Critical Illness insurance as a safety net for the unexpected, and it is. But there is a feature that not enough people are taking advantage of: the Return of Premium option.

How it works is that you pay your premiums over the life of your policy. If you never make a claim, you get that money back.

Why this matters:

• You are creating a structured savings plan with a built-in safety net

• If a critical illness like cancer, a heart attack, or stroke occurs, you receive a tax-free lump sum to use however you need

• If you stay healthy and never claim, your premiums are returned to you at expiry, often at age 65 or at the end of the term

• Unlike a traditional savings account, this money is set aside and not easily touched, making it a true forced savings vehicle for people who find it hard to save consistently

The bottom line is that you are either protecting your financial future from a health crisis, or you are getting your money back. There is no losing scenario.

If you want to understand how a Return of Premium rider could fit into your overall financial plan, reach out and we would be happy to walk you through the numbers.

How it works is that you pay your premiums over the life of your policy. If you never make a claim, you get that money back.

Why this matters:

• You are creating a structured savings plan with a built-in safety net

• If a critical illness like cancer, a heart attack, or stroke occurs, you receive a tax-free lump sum to use however you need

• If you stay healthy and never claim, your premiums are returned to you at expiry, often at age 65 or at the end of the term

• Unlike a traditional savings account, this money is set aside and not easily touched, making it a true forced savings vehicle for people who find it hard to save consistently

The bottom line is that you are either protecting your financial future from a health crisis, or you are getting your money back. There is no losing scenario.

If you want to understand how a Return of Premium rider could fit into your overall financial plan, reach out and we would be happy to walk you through the numbers.

The Case for Global Funds: Maximum Drawdown

Watch video

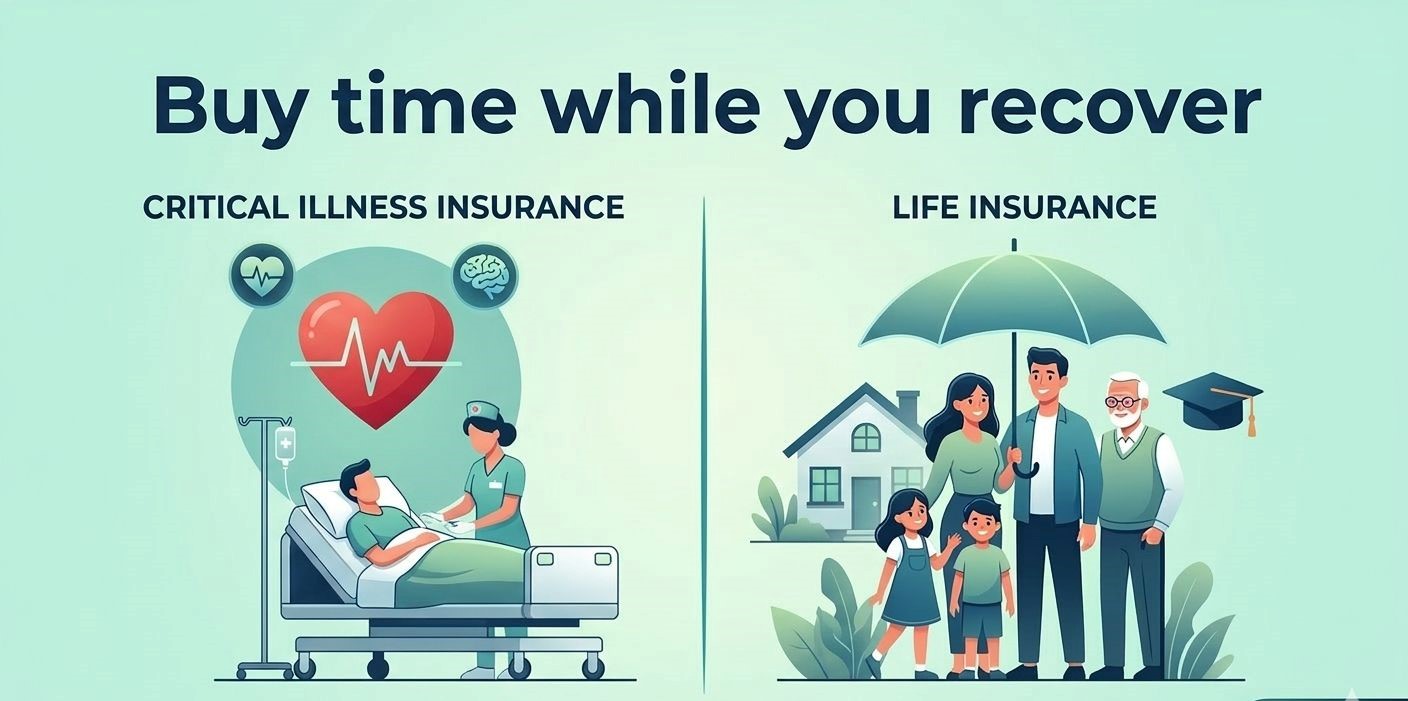

When most people think of insurance, they think of Life insurance, but there is another type of coverage that is highly beneficial to young people that is just as important.

Critical Illness Insurance vs. Life Insurance: What's the Difference?

Life Insurance is designed to protect the people who depend on you. If you pass away, your policy pays a tax-free lump sum to your beneficiaries to help cover things like lost income, a mortgage, or ongoing living expenses. It answers the question: "What happens to my family financially if I'm gone?"

Critical Illness Insurance is different. It is designed to protect you. If you are diagnosed with a covered condition such as cancer, a heart attack, or a stroke, you receive a tax-free lump sum while you are still alive. No receipts required, no justification needed. You decide how to use the money.

Now you may be thinking, "That won't happen to me!"

Nearly 50% of Canadians will be diagnosed with cancer in their lifetime. Survival rates are improving, which is great news, but it also means more people are living through serious illnesses and facing the financial weight that comes with them.

The goal of Life insurance is to protect your loved ones after you are gone. The goal of Critical Illness insurance is to protect your financial life while you are still living it.

If you have questions about whether Critical Illness coverage makes sense for your situation, we would be happy to walk you through it.

Critical Illness Insurance vs. Life Insurance: What's the Difference?

Life Insurance is designed to protect the people who depend on you. If you pass away, your policy pays a tax-free lump sum to your beneficiaries to help cover things like lost income, a mortgage, or ongoing living expenses. It answers the question: "What happens to my family financially if I'm gone?"

Critical Illness Insurance is different. It is designed to protect you. If you are diagnosed with a covered condition such as cancer, a heart attack, or a stroke, you receive a tax-free lump sum while you are still alive. No receipts required, no justification needed. You decide how to use the money.

Now you may be thinking, "That won't happen to me!"

Nearly 50% of Canadians will be diagnosed with cancer in their lifetime. Survival rates are improving, which is great news, but it also means more people are living through serious illnesses and facing the financial weight that comes with them.

The goal of Life insurance is to protect your loved ones after you are gone. The goal of Critical Illness insurance is to protect your financial life while you are still living it.

If you have questions about whether Critical Illness coverage makes sense for your situation, we would be happy to walk you through it.

When most people think of insurance, they think of Life insurance, but there is another type of coverage that is highly beneficial to young people that is just as important.

Critical Illness Insurance vs. Life Insurance: What's the Difference?

Life Insurance is designed to protect the people who depend on you. If you pass away, your policy pays a tax-free lump sum to your beneficiaries to help cover things like lost income, a mortgage, or ongoing living expenses. It answers the question: "What happens to my family financially if I'm gone?"

Critical Illness Insurance is different. It is designed to protect you. If you are diagnosed with a covered condition such as cancer, a heart attack, or a stroke, you receive a tax-free lump sum while you are still alive. No receipts required, no justification needed. You decide how to use the money.

Now you may be thinking, "That won't happen to me!"

Nearly 50% of Canadians will be diagnosed with cancer in their lifetime. Survival rates are improving, which is great news, but it also means more people are living through serious illnesses and facing the financial weight that comes with them.

The goal of Life insurance is to protect your loved ones after you are gone. The goal of Critical Illness insurance is to protect your financial life while you are still living it.

If you have questions about whether Critical Illness coverage makes sense for your situation, we would be happy to walk you through it.

Critical Illness Insurance vs. Life Insurance: What's the Difference?

Life Insurance is designed to protect the people who depend on you. If you pass away, your policy pays a tax-free lump sum to your beneficiaries to help cover things like lost income, a mortgage, or ongoing living expenses. It answers the question: "What happens to my family financially if I'm gone?"

Critical Illness Insurance is different. It is designed to protect you. If you are diagnosed with a covered condition such as cancer, a heart attack, or a stroke, you receive a tax-free lump sum while you are still alive. No receipts required, no justification needed. You decide how to use the money.

Now you may be thinking, "That won't happen to me!"

Nearly 50% of Canadians will be diagnosed with cancer in their lifetime. Survival rates are improving, which is great news, but it also means more people are living through serious illnesses and facing the financial weight that comes with them.

The goal of Life insurance is to protect your loved ones after you are gone. The goal of Critical Illness insurance is to protect your financial life while you are still living it.

If you have questions about whether Critical Illness coverage makes sense for your situation, we would be happy to walk you through it.

Global Investment Funds and Concentration Risk

Watch video

Global Economic Update for Our Clients:

Recent military escalation in the Middle East is creating ripple effects that could impact your finances. Here's what to watch out for:

Energy Costs Rising

Oil prices have jumped, and if they stay elevated, expect higher gas prices, increased airfare, and rising shipping costs, which flow through to your grocery bills.

Inflation Pressure

Economists are flagging the risk of a "stagflation" environment, where prices rise while economic growth slows. The Bank of Canada and U.S. Federal Reserve are closely monitoring the situation before making any rate moves.

What This Means for You

Now is a smart time to:

• Review your monthly budget for discretionary spending

• Lock in any large purchases you've been delaying (travel, appliances, vehicles)

• Ensure your emergency fund can cover 3-6 months of expenses

The Silver Lining: Most economists agree that if the situation stabilizes quickly, economic effects will be short-lived. Staying informed and proactive is your best defense.

As always, we're here to help you navigate uncertainty. Reach out if you'd like a quick financial check-in.

Recent military escalation in the Middle East is creating ripple effects that could impact your finances. Here's what to watch out for:

Energy Costs Rising

Oil prices have jumped, and if they stay elevated, expect higher gas prices, increased airfare, and rising shipping costs, which flow through to your grocery bills.

Inflation Pressure

Economists are flagging the risk of a "stagflation" environment, where prices rise while economic growth slows. The Bank of Canada and U.S. Federal Reserve are closely monitoring the situation before making any rate moves.

What This Means for You

Now is a smart time to:

• Review your monthly budget for discretionary spending

• Lock in any large purchases you've been delaying (travel, appliances, vehicles)

• Ensure your emergency fund can cover 3-6 months of expenses

The Silver Lining: Most economists agree that if the situation stabilizes quickly, economic effects will be short-lived. Staying informed and proactive is your best defense.

As always, we're here to help you navigate uncertainty. Reach out if you'd like a quick financial check-in.

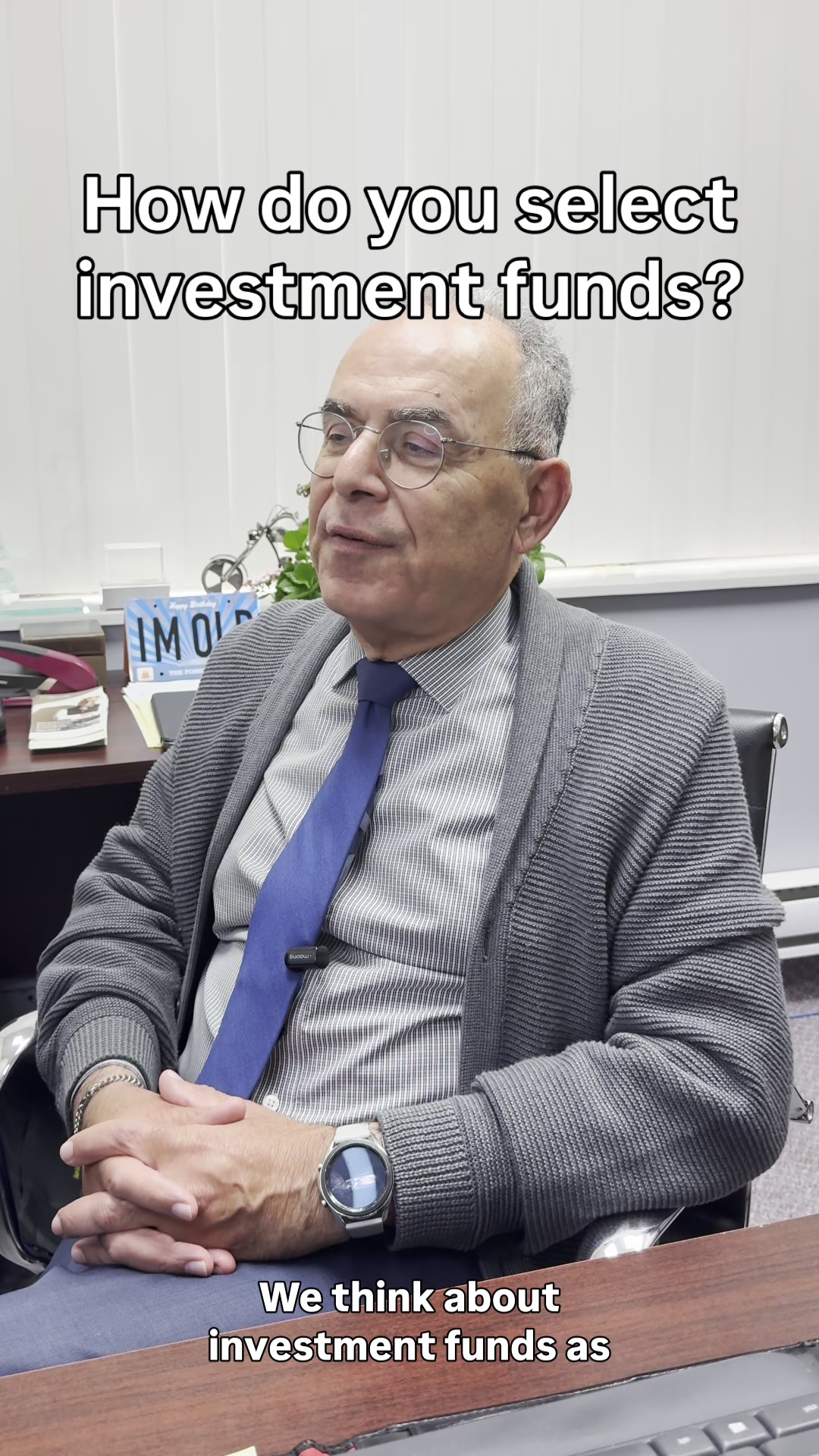

Selecting Investment Funds

Watch video

The March 2nd deadline gets a lot of attention, and rightfully so. But treating RRSP contributions as your once-a-year tax move means leaving a lot on the table.

Tax planning is a year-round (or in all honestly, a lifelong) conversation. Whether it's TFSA contributions, income splitting, capital gains timing, tracking business expenses, or planning for major life changes. The decisions you make in June or October can matter just as much as the ones you make in February.

If you scrambled to find contribution room before the deadline, that's actually a great signal to start a more intentional plan now, before next year sneak up on you.

We're always happy to sit down and talk through what a year-round strategy could look like for you.

Tax planning is a year-round (or in all honestly, a lifelong) conversation. Whether it's TFSA contributions, income splitting, capital gains timing, tracking business expenses, or planning for major life changes. The decisions you make in June or October can matter just as much as the ones you make in February.

If you scrambled to find contribution room before the deadline, that's actually a great signal to start a more intentional plan now, before next year sneak up on you.

We're always happy to sit down and talk through what a year-round strategy could look like for you.

The March 2nd deadline gets a lot of attention, and rightfully so. But treating RRSP contributions as your once-a-year tax move means leaving a lot on the table.

Tax planning is a year-round (or in all honestly, a lifelong) conversation. Whether it's TFSA contributions, income splitting, capital gains timing, tracking business expenses, or planning for major life changes. The decisions you make in June or October can matter just as much as the ones you make in February.

If you scrambled to find contribution room before the deadline, that's actually a great signal to start a more intentional plan now, before next year sneak up on you.

We're always happy to sit down and talk through what a year-round strategy could look like for you.

Tax planning is a year-round (or in all honestly, a lifelong) conversation. Whether it's TFSA contributions, income splitting, capital gains timing, tracking business expenses, or planning for major life changes. The decisions you make in June or October can matter just as much as the ones you make in February.

If you scrambled to find contribution room before the deadline, that's actually a great signal to start a more intentional plan now, before next year sneak up on you.

We're always happy to sit down and talk through what a year-round strategy could look like for you.

Happy Valentine's Day Everyone!

While flowers and dinner are lovely, one of the most everlasting things you can do for your relationship is get on the same page financially.

As you might know, money is one of the leading sources of stress within a relationship. With some simple planning it really doesn’t have to be.

Whether you're newly together or have been sharing finances for years, February is a great time to have an honest conversation about:

• Your shared goals (home, travel, retirement)

• How you should split your day-to-day expenses

• Any debt each person is carrying

• And how your emergency fund is looking

It doesn't have to be a heavy conversation, even a casual 15-minute chat over dinner can make a big difference.

If you'd like a simple framework for starting your joint financial planning conversation or need help setting up a joint budget, we're always happy to help!

While flowers and dinner are lovely, one of the most everlasting things you can do for your relationship is get on the same page financially.

As you might know, money is one of the leading sources of stress within a relationship. With some simple planning it really doesn’t have to be.

Whether you're newly together or have been sharing finances for years, February is a great time to have an honest conversation about:

• Your shared goals (home, travel, retirement)

• How you should split your day-to-day expenses

• Any debt each person is carrying

• And how your emergency fund is looking

It doesn't have to be a heavy conversation, even a casual 15-minute chat over dinner can make a big difference.

If you'd like a simple framework for starting your joint financial planning conversation or need help setting up a joint budget, we're always happy to help!

Happy Valentine's Day Everyone!

While flowers and dinner are lovely, one of the most everlasting things you can do for your relationship is get on the same page financially.

As you might know, money is one of the leading sources of stress within a relationship. With some simple planning it really doesn’t have to be.

Whether you're newly together or have been sharing finances for years, February is a great time to have an honest conversation about:

• Your shared goals (home, travel, retirement)

• How you should split your day-to-day expenses

• Any debt each person is carrying

• And how your emergency fund is looking

It doesn't have to be a heavy conversation, even a casual 15-minute chat over dinner can make a big difference.

If you'd like a simple framework for starting your joint financial planning conversation or need help setting up a joint budget, we're always happy to help!

While flowers and dinner are lovely, one of the most everlasting things you can do for your relationship is get on the same page financially.

As you might know, money is one of the leading sources of stress within a relationship. With some simple planning it really doesn’t have to be.

Whether you're newly together or have been sharing finances for years, February is a great time to have an honest conversation about:

• Your shared goals (home, travel, retirement)

• How you should split your day-to-day expenses

• Any debt each person is carrying

• And how your emergency fund is looking

It doesn't have to be a heavy conversation, even a casual 15-minute chat over dinner can make a big difference.

If you'd like a simple framework for starting your joint financial planning conversation or need help setting up a joint budget, we're always happy to help!

We wanted to give you a heads up that the GST/HST break that the federal government put into place in early December comes to an end on February 15th, 2026. So, if you notice your grocery receipts or kids’ clothing bills looking higher than usual, you aren’t imagining it.

Items that Qualified:

• Food

• Beverages

• Restaurants, Catering, or other food/drink establishments

• Kid’s Clothing & Footwear

• Children’s Diapers & Car Seats

• Kid’s toys & Puzzles

• Video game Consoles, Controllers, and Physical Video Games

• Physical Books & Newspapers

• Christmas/ Holiday Decorative Tress

While that tax break provided some short-term relief, many Canadians are now feeling the "rebound" as prices return to normal. Now is a great time to do a quick 10-minute audit of your monthly spending.

If you are looking for resources or a simple spreadsheet to track your expenses, feel free to reach out to us and we’d be happy to help.

Link: https://www.canada.ca/en/services/taxes/child-and-family-benefits/gst-hst-holiday-tax-break.html

Items that Qualified:

• Food

• Beverages

• Restaurants, Catering, or other food/drink establishments

• Kid’s Clothing & Footwear

• Children’s Diapers & Car Seats

• Kid’s toys & Puzzles

• Video game Consoles, Controllers, and Physical Video Games

• Physical Books & Newspapers

• Christmas/ Holiday Decorative Tress

While that tax break provided some short-term relief, many Canadians are now feeling the "rebound" as prices return to normal. Now is a great time to do a quick 10-minute audit of your monthly spending.

If you are looking for resources or a simple spreadsheet to track your expenses, feel free to reach out to us and we’d be happy to help.

Link: https://www.canada.ca/en/services/taxes/child-and-family-benefits/gst-hst-holiday-tax-break.html

We wanted to give you a heads up that the GST/HST break that the federal government put into place in early December comes to an end on February 15th, 2026. So, if you notice your grocery receipts or kids’ clothing bills looking higher than usual, you aren’t imagining it.

Items that Qualified:

• Food

• Beverages

• Restaurants, Catering, or other food/drink establishments

• Kid’s Clothing & Footwear

• Children’s Diapers & Car Seats

• Kid’s toys & Puzzles

• Video game Consoles, Controllers, and Physical Video Games

• Physical Books & Newspapers

• Christmas/ Holiday Decorative Tress

While that tax break provided some short-term relief, many Canadians are now feeling the "rebound" as prices return to normal. Now is a great time to do a quick 10-minute audit of your monthly spending.

If you are looking for resources or a simple spreadsheet to track your expenses, feel free to reach out to us and we’d be happy to help.

Link: https://www.canada.ca/en/services/taxes/child-and-family-benefits/gst-hst-holiday-tax-break.html

Items that Qualified:

• Food

• Beverages

• Restaurants, Catering, or other food/drink establishments

• Kid’s Clothing & Footwear

• Children’s Diapers & Car Seats

• Kid’s toys & Puzzles

• Video game Consoles, Controllers, and Physical Video Games

• Physical Books & Newspapers

• Christmas/ Holiday Decorative Tress

While that tax break provided some short-term relief, many Canadians are now feeling the "rebound" as prices return to normal. Now is a great time to do a quick 10-minute audit of your monthly spending.

If you are looking for resources or a simple spreadsheet to track your expenses, feel free to reach out to us and we’d be happy to help.

Link: https://www.canada.ca/en/services/taxes/child-and-family-benefits/gst-hst-holiday-tax-break.html

February is Heart Health Month. Heart disease affects 1 in 12 Canadian adults – a reminder of why protecting both your health and your financial wellbeing matters.

Critical illness insurance can help provide financial support when you need it most, helping you focus on recovery without the added stress of financial uncertainty. Find out more. Let's connect!

Critical illness insurance can help provide financial support when you need it most, helping you focus on recovery without the added stress of financial uncertainty. Find out more. Let's connect!

February is Heart Health Month. Heart disease affects 1 in 12 Canadian adults – a reminder of why protecting both your health and your financial wellbeing matters.

Critical illness insurance can help provide financial support when you need it most, helping you focus on recovery without the added stress of financial uncertainty. Find out more. Let's connect!

Critical illness insurance can help provide financial support when you need it most, helping you focus on recovery without the added stress of financial uncertainty. Find out more. Let's connect!

Time flies by, and tuition costs fly sky-high. 🕰️💸 When it comes to education costs for your kid(s), it pays to start early and save consistently. Small RESP contributions can add up over time.

Want to explore how to optimize saving for your child(ren)’s education? Let's chat about creating a plan that fits your family's budget. https://advisor.sunlife.ca/joe.salib

Want to explore how to optimize saving for your child(ren)’s education? Let's chat about creating a plan that fits your family's budget. https://advisor.sunlife.ca/joe.salib

Time flies by, and tuition costs fly sky-high. 🕰️💸 When it comes to education costs for your kid(s), it pays to start early and save consistently. Small RESP contributions can add up over time.

Want to explore how to optimize saving for your child(ren)’s education? Let's chat about creating a plan that fits your family's budget. https://advisor.sunlife.ca/joe.salib

Want to explore how to optimize saving for your child(ren)’s education? Let's chat about creating a plan that fits your family's budget. https://advisor.sunlife.ca/joe.salib

Life changes, goals evolve and your estate plan should too.

Whether navigating business succession, protecting family wealth or maximizing tax efficiency, we can help ensure your legacy reflects your current vision and helps protect what matters most.

Ready to review your plan? Reach out today. https://advisor.sunlife.ca/joe.salib

Whether navigating business succession, protecting family wealth or maximizing tax efficiency, we can help ensure your legacy reflects your current vision and helps protect what matters most.

Ready to review your plan? Reach out today. https://advisor.sunlife.ca/joe.salib

Life changes, goals evolve and your estate plan should too.

Whether navigating business succession, protecting family wealth or maximizing tax efficiency, we can help ensure your legacy reflects your current vision and helps protect what matters most.

Ready to review your plan? Reach out today. https://advisor.sunlife.ca/joe.salib

Whether navigating business succession, protecting family wealth or maximizing tax efficiency, we can help ensure your legacy reflects your current vision and helps protect what matters most.

Ready to review your plan? Reach out today. https://advisor.sunlife.ca/joe.salib

Dreaming big for your future? Let's talk about how we help turn those dreams into reality. Whether it's early retirement or a new business venture, let's create a strategy to get you there.

Reach out to start your journey!

Reach out to start your journey!

Dreaming big for your future? Let's talk about how we help turn those dreams into reality. Whether it's early retirement or a new business venture, let's create a strategy to get you there.

Reach out to start your journey!

Reach out to start your journey!

Financial advice that fits your needs. Let Sun Life One Plan help.

Create your personalized roadmap with Sun Life One Plan! This powerful tool helps you set achievable goals and brings your financial dreams closer to reality. https://sunlife.hubs.vidyard.com/watch/ksLWJjT43furjobhkXkgiQ

Take control of your financial future. Reach out today to get started!

#RetirementPlanning #SunLifeOnePlan

Take control of your financial future. Reach out today to get started!

#RetirementPlanning #SunLifeOnePlan

Watch video

As a business owner, your personal and professional finances are intertwined. Let's create a financial roadmap that aligns your business growth with your personal goals.

Reach out to discuss how we can help you build a brighter future for both you and your company.

Reach out to discuss how we can help you build a brighter future for both you and your company.

As a business owner, your personal and professional finances are intertwined. Let's create a financial roadmap that aligns your business growth with your personal goals.

Reach out to discuss how we can help you build a brighter future for both you and your company.

Reach out to discuss how we can help you build a brighter future for both you and your company.

Have questions?

Here to help answer your questions, provide clarity about products and get you started on the road to achieving your goals.