Stay informed

Stay informed with what’s going on. Browse posts that might be helpful to you or check out an event happening in your area. Come back regularly as this page is kept up-to-date with a lot of relevant information.

Be prepared for whatever your next chapter brings. I can help you reach your financial goals.

Watch video

As a Canadian business owner, how you draw income matters. Salary, dividends or a mix? The right approach depends on your business goals and personal needs, and does impact your tax bill.

Let's talk about optimizing your compensation strategy.

https://advisor.sunlife.ca/mark.noble

#CanadianBusiness #TaxPlanning #IncomeTaxes

Let's talk about optimizing your compensation strategy.

https://advisor.sunlife.ca/mark.noble

#CanadianBusiness #TaxPlanning #IncomeTaxes

As a Canadian business owner, how you draw income matters. Salary, dividends or a mix? The right approach depends on your business goals and personal needs, and does impact your tax bill.

Let's talk about optimizing your compensation strategy.

https://advisor.sunlife.ca/mark.noble

#CanadianBusiness #TaxPlanning #IncomeTaxes

Let's talk about optimizing your compensation strategy.

https://advisor.sunlife.ca/mark.noble

#CanadianBusiness #TaxPlanning #IncomeTaxes

A holistic financial roadmap balances protection, investment and access to cash for life’s moments. Together we can tailor an approach that fits your financial needs. Ask me about Sun Life One Plan. https://advisor.sunlife.ca/mark.noble

#SunLifeOnePlan

#SunLifeOnePlan

A holistic financial roadmap balances protection, investment and access to cash for life’s moments. Together we can tailor an approach that fits your financial needs. Ask me about Sun Life One Plan. https://advisor.sunlife.ca/mark.noble

#SunLifeOnePlan

#SunLifeOnePlan

A simple plan helps balance today’s cost with tomorrow’s goals. Let’s build a family cash-flow roadmap that works for you.

https://advisor.sunlife.ca/mark.noble

https://advisor.sunlife.ca/mark.noble

A simple plan helps balance today’s cost with tomorrow’s goals. Let’s build a family cash-flow roadmap that works for you.

https://advisor.sunlife.ca/mark.noble

https://advisor.sunlife.ca/mark.noble

With Sun Life's free life insurance calculator, in just a few minutes you can easily predict how much life insurance you might need. Try it out, then let’s connect to chat more!

https://www.sunlife.ca/en/tools-and-resources/tools-and-calculators/life-insurance-calculator/

https://www.sunlife.ca/en/tools-and-resources/tools-and-calculators/life-insurance-calculator/

With Sun Life's free life insurance calculator, in just a few minutes you can easily predict how much life insurance you might need. Try it out, then let’s connect to chat more!

https://www.sunlife.ca/en/tools-and-resources/tools-and-calculators/life-insurance-calculator/

https://www.sunlife.ca/en/tools-and-resources/tools-and-calculators/life-insurance-calculator/

We help you align strategies to your goals and your comfort level with market volatility.

Have you had a risk conversation regarding your financial portfolio lately? Get in touch. https://advisor.sunlife.ca/mark.noble

Have you had a risk conversation regarding your financial portfolio lately? Get in touch. https://advisor.sunlife.ca/mark.noble

We help you align strategies to your goals and your comfort level with market volatility.

Have you had a risk conversation regarding your financial portfolio lately? Get in touch. https://advisor.sunlife.ca/mark.noble

Have you had a risk conversation regarding your financial portfolio lately? Get in touch. https://advisor.sunlife.ca/mark.noble

If there’s one thing that’s guaranteed, it’s that life is unpredictable. Let’s talk about how Sun Life can help you get prepared for whatever life brings.

Watch video

I can help you set up your TFSA so you’re ready for life’s expected and unexpected turns. Get in touch with me to get started!

I can help you set up your TFSA so you’re ready for life’s expected and unexpected turns. Get in touch with me to get started!

Your insurance needs are unique at every life stage.

Consider layering insurance policies to benefit from more flexible coverage.

Check out our article to learn more and see if it would suit you.

Consider layering insurance policies to benefit from more flexible coverage.

Check out our article to learn more and see if it would suit you.

How Gen Z is redefining retirement strategies

Better retirement benefits can support young talent as they juggle caregiving responsibilities, AI fears and high levels of burnout.

Life is unpredictable. What if you got an unexpected diagnosis? I'm here to help! Learn how critical illness insurance could help protect your finances.

Life is unpredictable. What if you got an unexpected diagnosis? I'm here to help! Learn how critical illness insurance could help protect your finances.

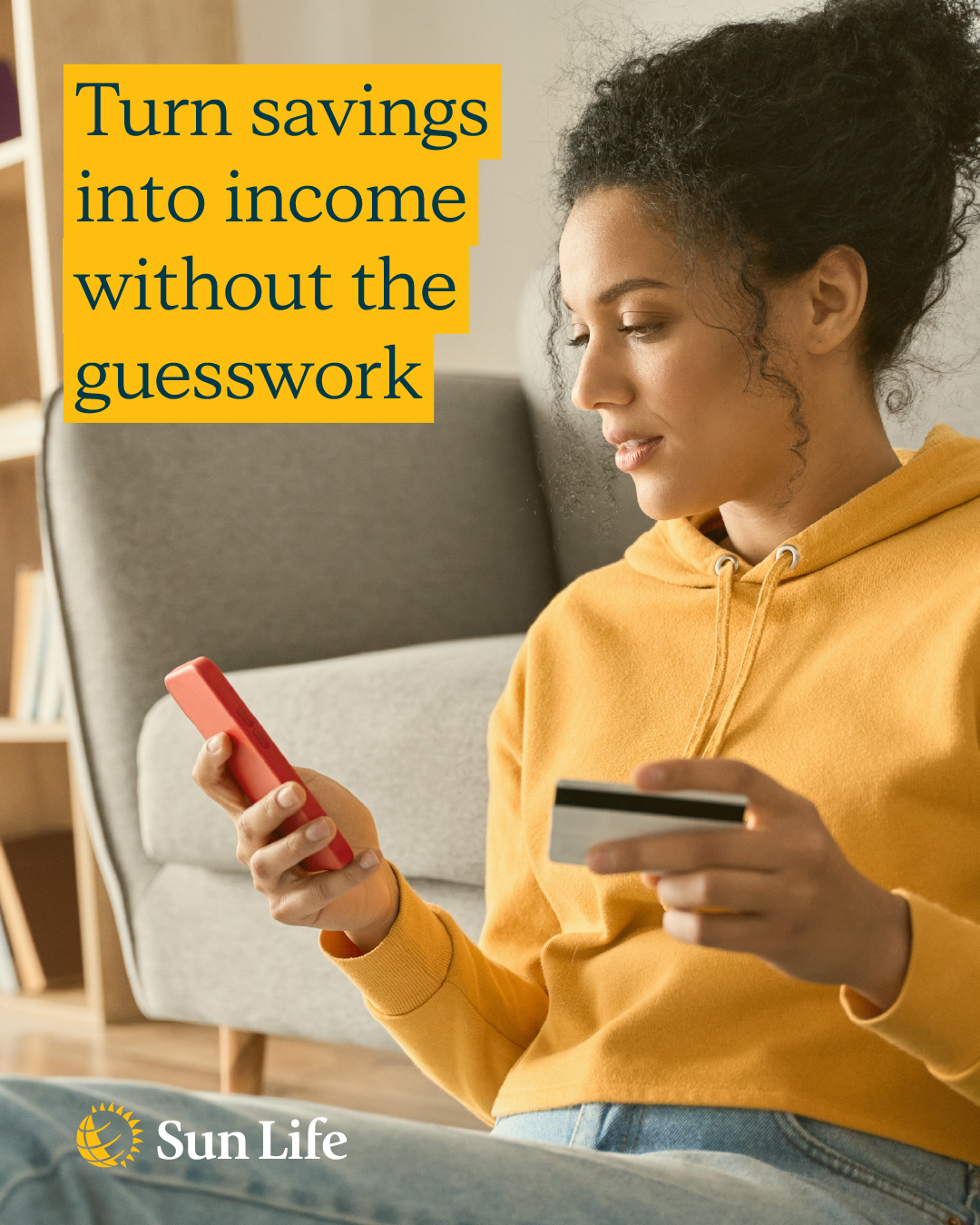

Retirement isn’t a number — it’s a roadmap. We’ll outline how your savings can become a reliable source of income. Together, let's build your withdrawal strategy.

#RetirementStrategy #Retirement #SunLife

#RetirementStrategy #Retirement #SunLife

Retirement isn’t a number — it’s a roadmap. We’ll outline how your savings can become a reliable source of income. Together, let's build your withdrawal strategy.

#RetirementStrategy #Retirement #SunLife

#RetirementStrategy #Retirement #SunLife

Many business owners reinvest every dollar back into their business. Having a strategic plan helps you decide what to reinvest and what to set aside for your future.

Book a Sun Life One Plan conversation to map out your next steps. https://advisor.sunlife.ca/mark.noble

#SunLifeOnePlan

Book a Sun Life One Plan conversation to map out your next steps. https://advisor.sunlife.ca/mark.noble

#SunLifeOnePlan

Many business owners reinvest every dollar back into their business. Having a strategic plan helps you decide what to reinvest and what to set aside for your future.

Book a Sun Life One Plan conversation to map out your next steps. https://advisor.sunlife.ca/mark.noble

#SunLifeOnePlan

Book a Sun Life One Plan conversation to map out your next steps. https://advisor.sunlife.ca/mark.noble

#SunLifeOnePlan

Five Mistakes to Avoid in Your First Year of Retirement

Retirement brings the freedom to choose how to spend your money and time. But choices made in the initial rush of excitement could create problems in future.

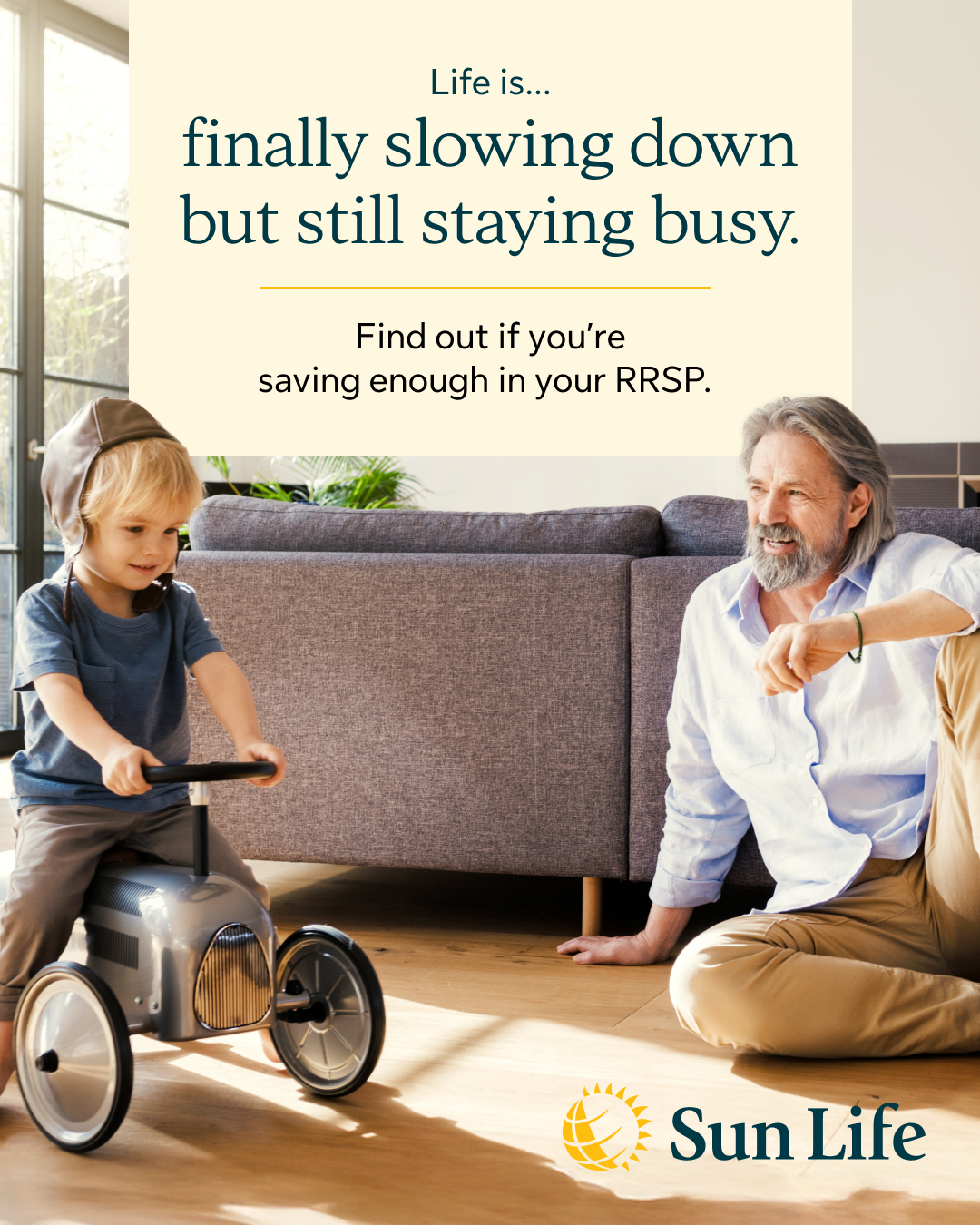

Are you saving enough in your RRSP for the retirement you want? Crunch the numbers in Sun Life's free RRSP calculator. Then, let’s connect and talk about your options.

https://www.sunlife.ca/en/tools-and-resources/tools-and-calculators/rrsp-calculator/

https://www.sunlife.ca/en/tools-and-resources/tools-and-calculators/rrsp-calculator/

Are you saving enough in your RRSP for the retirement you want? Crunch the numbers in Sun Life's free RRSP calculator. Then, let’s connect and talk about your options.

https://www.sunlife.ca/en/tools-and-resources/tools-and-calculators/rrsp-calculator/

https://www.sunlife.ca/en/tools-and-resources/tools-and-calculators/rrsp-calculator/

I can help you make the most of your savings, so you can be ready for what comes next. Let’s talk about your goals.

Watch video

From health spending accounts to enhanced benefits, there are ways to cover what provincial plans don't — and sometimes save on taxes too. Let's explore what fits your needs and budget.

From health spending accounts to enhanced benefits, there are ways to cover what provincial plans don't — and sometimes save on taxes too. Let's explore what fits your needs and budget.

Family is everything! When you meet with me, we’ll discuss how you can plan to protect them no matter what life throws at you, the expected and the unexpected.

Family is everything! When you meet with me, we’ll discuss how you can plan to protect them no matter what life throws at you, the expected and the unexpected.

Tax season isn't just about filing — it's about planning ahead. From RRSP contributions to income splitting strategies, there are things you can do now to better position your finances for next year and beyond.

Get in touch to find out what strategies work best for you. https://advisor.sunlife.ca/mark.noble

Get in touch to find out what strategies work best for you. https://advisor.sunlife.ca/mark.noble

Tax season isn't just about filing — it's about planning ahead. From RRSP contributions to income splitting strategies, there are things you can do now to better position your finances for next year and beyond.

Get in touch to find out what strategies work best for you. https://advisor.sunlife.ca/mark.noble

Get in touch to find out what strategies work best for you. https://advisor.sunlife.ca/mark.noble

A withdrawal strategy can help create dependable income while helping you manage risk. Let’s chat about income planning basics that fit your needs. https://advisor.sunlife.ca/mark.noble

A withdrawal strategy can help create dependable income while helping you manage risk. Let’s chat about income planning basics that fit your needs. https://advisor.sunlife.ca/mark.noble

Have questions?

Here to help answer your questions, provide clarity about products and get you started on the road to achieving your goals.