Stay informed

Stay informed with what’s going on. Browse posts that might be helpful to you or check out an event happening in your area. Come back regularly as this page is kept up-to-date with a lot of relevant information.

RRSPs: Know your limits

Boost your knowledge with this helpful article.

https://www.sunlifeglobalinvestments.com/en/insights/investor-education/getting-started/rrsps-know-your-limits/?slgi_r=investor

The opinions expressed in this article are of the fund company that owns this content and do not constitute professional advice or recommendation. Please seek advice from a qualified professional, including a thorough examination of your specific legal, accounting and tax situation.

https://www.sunlifeglobalinvestments.com/en/insights/investor-education/getting-started/rrsps-know-your-limits/?slgi_r=investor

The opinions expressed in this article are of the fund company that owns this content and do not constitute professional advice or recommendation. Please seek advice from a qualified professional, including a thorough examination of your specific legal, accounting and tax situation.

Life insurance helps ensure your family can maintain their lifestyle, pay off debts and fund future goals even after you die. Simple, affordable coverage can make all the difference. Message me for a personalized coverage estimate. https://advisor.sunlife.ca/sandeep.bawa

Life insurance helps ensure your family can maintain their lifestyle, pay off debts and fund future goals even after you die. Simple, affordable coverage can make all the difference. Message me for a personalized coverage estimate. https://advisor.sunlife.ca/sandeep.bawa

Objectifs à court, moyen et long terme organisés en un seul endroit pour agir avec confiance. Commençons avec votre #UnPlanSimplementSunLife. Contactez-moi pour plus d'information. https://conseiller.sunlife.ca/f/sandeep.bawa

Objectifs à court, moyen et long terme organisés en un seul endroit pour agir avec confiance. Commençons avec votre #UnPlanSimplementSunLife. Contactez-moi pour plus d'information. https://conseiller.sunlife.ca/f/sandeep.bawa

A holistic financial roadmap balances protection, investment and access to cash for life’s moments. Together we can tailor an approach that fits your financial needs. Ask me about Sun Life One Plan. https://advisor.sunlife.ca/sandeep.bawa

#SunLifeOnePlan

#SunLifeOnePlan

A holistic financial roadmap balances protection, investment and access to cash for life’s moments. Together we can tailor an approach that fits your financial needs. Ask me about Sun Life One Plan. https://advisor.sunlife.ca/sandeep.bawa

#SunLifeOnePlan

#SunLifeOnePlan

Un parcours simple permet d’équilibrer les coûts actuels avec les objectifs futurs. Établissons ensemble un budget familial qui fonctionne pour vous.

https://conseiller.sunlife.ca/f/sandeep.bawa

https://conseiller.sunlife.ca/f/sandeep.bawa

Un parcours simple permet d’équilibrer les coûts actuels avec les objectifs futurs. Établissons ensemble un budget familial qui fonctionne pour vous.

https://conseiller.sunlife.ca/f/sandeep.bawa

https://conseiller.sunlife.ca/f/sandeep.bawa

Thinking about your family's future? Be prepared for life’s certainties and surprises with permanent life insurance. It helps offer protection today and a financial legacy for loved ones later. Find out how, get in touch. https://advisor.sunlife.ca/sandeep.bawa

Thinking about your family's future? Be prepared for life’s certainties and surprises with permanent life insurance. It helps offer protection today and a financial legacy for loved ones later. Find out how, get in touch. https://advisor.sunlife.ca/sandeep.bawa

When it comes to your savings, don’t let common TFSA mistakes tip you overboard. Read this article on the 4 mistakes to avoid and then let’s connect to discuss how I can help you.

When it comes to your savings, don’t let common TFSA mistakes tip you overboard. Read this article on the 4 mistakes to avoid and then let’s connect to discuss how I can help you.

Tax time is also estate-planning time. Reviewing your return helps ensure beneficiary designations, ownership structures and transfer plans align with your wishes, while reducing potential taxes on asset transfers.

Tax time is also estate-planning time. Reviewing your return helps ensure beneficiary designations, ownership structures and transfer plans align with your wishes, while reducing potential taxes on asset transfers.

L’automne est arrivé et le paysage change. Peut-être est-ce le moment de changer votre stratégie fiscale?

Voici une série de mesures à envisager :

-Cristalliser les pertes fiscales pour compenser les gains 📉

-Maximiser les cotisations à votre CELI 💰

-Revoir votre stratégie de dons de bienfaisance 🎁

-Explorer des possibilités de fractionnement du revenu 👥

-Penser aux prêts à taux prescrit pour les membres de votre famille 💸

Ne laissez rien hasard quand il s’agit de votre argent durement gagné. Parlons de vous créer une stratégie personnalisée d’optimisation fiscale de fin d’année qui concorde avec vos objectifs actuels. Les petits gestes peuvent avoir une grande incidence sur votre avenir financier. Communiquez avec moi dès aujourd’hui.

Voici une série de mesures à envisager :

-Cristalliser les pertes fiscales pour compenser les gains 📉

-Maximiser les cotisations à votre CELI 💰

-Revoir votre stratégie de dons de bienfaisance 🎁

-Explorer des possibilités de fractionnement du revenu 👥

-Penser aux prêts à taux prescrit pour les membres de votre famille 💸

Ne laissez rien hasard quand il s’agit de votre argent durement gagné. Parlons de vous créer une stratégie personnalisée d’optimisation fiscale de fin d’année qui concorde avec vos objectifs actuels. Les petits gestes peuvent avoir une grande incidence sur votre avenir financier. Communiquez avec moi dès aujourd’hui.

L’automne est arrivé et le paysage change. Peut-être est-ce le moment de changer votre stratégie fiscale?

Voici une série de mesures à envisager :

-Cristalliser les pertes fiscales pour compenser les gains 📉

-Maximiser les cotisations à votre CELI 💰

-Revoir votre stratégie de dons de bienfaisance 🎁

-Explorer des possibilités de fractionnement du revenu 👥

-Penser aux prêts à taux prescrit pour les membres de votre famille 💸

Ne laissez rien hasard quand il s’agit de votre argent durement gagné. Parlons de vous créer une stratégie personnalisée d’optimisation fiscale de fin d’année qui concorde avec vos objectifs actuels. Les petits gestes peuvent avoir une grande incidence sur votre avenir financier. Communiquez avec moi dès aujourd’hui.

Voici une série de mesures à envisager :

-Cristalliser les pertes fiscales pour compenser les gains 📉

-Maximiser les cotisations à votre CELI 💰

-Revoir votre stratégie de dons de bienfaisance 🎁

-Explorer des possibilités de fractionnement du revenu 👥

-Penser aux prêts à taux prescrit pour les membres de votre famille 💸

Ne laissez rien hasard quand il s’agit de votre argent durement gagné. Parlons de vous créer une stratégie personnalisée d’optimisation fiscale de fin d’année qui concorde avec vos objectifs actuels. Les petits gestes peuvent avoir une grande incidence sur votre avenir financier. Communiquez avec moi dès aujourd’hui.

Tax season isn't just about filing — it's about planning ahead. From RRSP contributions to income splitting strategies, there are things you can do now to better position your finances for next year and beyond.

Get in touch to find out what strategies work best for you. https://advisor.sunlife.ca/sandeep.bawa

Get in touch to find out what strategies work best for you. https://advisor.sunlife.ca/sandeep.bawa

Tax season isn't just about filing — it's about planning ahead. From RRSP contributions to income splitting strategies, there are things you can do now to better position your finances for next year and beyond.

Get in touch to find out what strategies work best for you. https://advisor.sunlife.ca/sandeep.bawa

Get in touch to find out what strategies work best for you. https://advisor.sunlife.ca/sandeep.bawa

As proud partners and lifelong fans of the Toronto Raptors, we know every great play starts with a solid game plan – on and off the court.

Let’s go Raptors!

Let’s go Raptors!

As proud partners and lifelong fans of the Toronto Raptors, we know every great play starts with a solid game plan – on and off the court.

Let’s go Raptors!

Let’s go Raptors!

Greater clarity on the main risks to the market

Dive into expert insights on building and preserving wealth in today’s economic landscape.

https://www.invesco.com/ca/en/insights/greater-clarity-risks-market.html

The opinions expressed in this article are of the fund company that owns this content and do not constitute professional advice or recommendation. Please seek advice from a qualified professional, including a thorough examination of your specific legal, accounting and tax situation.

https://www.invesco.com/ca/en/insights/greater-clarity-risks-market.html

The opinions expressed in this article are of the fund company that owns this content and do not constitute professional advice or recommendation. Please seek advice from a qualified professional, including a thorough examination of your specific legal, accounting and tax situation.

5 Expert-Backed Ways To Improve Your Grip Strength for Healthy Aging

Hand strength is linked with longevity and is important for maintaining independence as you age. https://advisor.sunlife.ca/sandeep.bawa

For the people cheering you on every day, protect their future with the ultimate defence: life insurance.

This is a good time to check in and review your life insurance coverage.

🏀See how much coverage you need to protect what matters most: https://www.sunlife.ca/en/tools-and-resources/tools-and-calculators/life-insurance-calculator/

This is a good time to check in and review your life insurance coverage.

🏀See how much coverage you need to protect what matters most: https://www.sunlife.ca/en/tools-and-resources/tools-and-calculators/life-insurance-calculator/

For the people cheering you on every day, protect their future with the ultimate defence: life insurance.

This is a good time to check in and review your life insurance coverage.

🏀See how much coverage you need to protect what matters most: https://www.sunlife.ca/en/tools-and-resources/tools-and-calculators/life-insurance-calculator/

This is a good time to check in and review your life insurance coverage.

🏀See how much coverage you need to protect what matters most: https://www.sunlife.ca/en/tools-and-resources/tools-and-calculators/life-insurance-calculator/

On International Women's Day, we honour women's achievements and our commitment to advancing their financial security and wellness

Every person's journey to wealth, health and well-being is unique. Many factors, including gender, race and age can impact and shape the trajectory of our lives.

When women are empowered, more opportunities arise across our communities. Learn what steps you can take to help you get closer to your financial independence: https://www.sunlife.ca/en/empowering-women-wealth-health-financial-security/

#EmpowerHer #IWD2026 #InternationalWomensDay

Every person's journey to wealth, health and well-being is unique. Many factors, including gender, race and age can impact and shape the trajectory of our lives.

When women are empowered, more opportunities arise across our communities. Learn what steps you can take to help you get closer to your financial independence: https://www.sunlife.ca/en/empowering-women-wealth-health-financial-security/

#EmpowerHer #IWD2026 #InternationalWomensDay

On International Women's Day, we honour women's achievements and our commitment to advancing their financial security and wellness

Every person's journey to wealth, health and well-being is unique. Many factors, including gender, race and age can impact and shape the trajectory of our lives.

When women are empowered, more opportunities arise across our communities. Learn what steps you can take to help you get closer to your financial independence: https://www.sunlife.ca/en/empowering-women-wealth-health-financial-security/

#EmpowerHer #IWD2026 #InternationalWomensDay

Every person's journey to wealth, health and well-being is unique. Many factors, including gender, race and age can impact and shape the trajectory of our lives.

When women are empowered, more opportunities arise across our communities. Learn what steps you can take to help you get closer to your financial independence: https://www.sunlife.ca/en/empowering-women-wealth-health-financial-security/

#EmpowerHer #IWD2026 #InternationalWomensDay

On International Women's Day, we honour women's achievements and our commitment to advancing their financial security and wellness.

Every person's journey to wealth, health and well-being is unique. Many factors, including gender, race and age can impact and shape the trajectory of our lives.

When women are empowered, more opportunities arise across our communities. Learn what steps you can take to help you get closer to your financial independence: https://www.sunlife.ca/en/empowering-women-wealth-health-financial-security/

#EmpowerHer #IWD2026 #InternationalWomensDay

Every person's journey to wealth, health and well-being is unique. Many factors, including gender, race and age can impact and shape the trajectory of our lives.

When women are empowered, more opportunities arise across our communities. Learn what steps you can take to help you get closer to your financial independence: https://www.sunlife.ca/en/empowering-women-wealth-health-financial-security/

#EmpowerHer #IWD2026 #InternationalWomensDay

On International Women's Day, we honour women's achievements and our commitment to advancing their financial security and wellness.

Every person's journey to wealth, health and well-being is unique. Many factors, including gender, race and age can impact and shape the trajectory of our lives.

When women are empowered, more opportunities arise across our communities. Learn what steps you can take to help you get closer to your financial independence: https://www.sunlife.ca/en/empowering-women-wealth-health-financial-security/

#EmpowerHer #IWD2026 #InternationalWomensDay

Every person's journey to wealth, health and well-being is unique. Many factors, including gender, race and age can impact and shape the trajectory of our lives.

When women are empowered, more opportunities arise across our communities. Learn what steps you can take to help you get closer to your financial independence: https://www.sunlife.ca/en/empowering-women-wealth-health-financial-security/

#EmpowerHer #IWD2026 #InternationalWomensDay

From health spending accounts to enhanced benefits, there are ways to cover what provincial plans don't — and sometimes save on taxes too. Let's explore what fits your needs and budget.

From health spending accounts to enhanced benefits, there are ways to cover what provincial plans don't — and sometimes save on taxes too. Let's explore what fits your needs and budget.

Canada 2026 Outlook: Competitive Advantages Underpin a Brighter Outlook | Vanguard Canada

Access helpful resources on financial knowledge developed by professionals in the industry.

https://www.vanguard.ca/en/insights/canada-outlook

The opinions expressed in this article are of the fund company that owns this content and do not constitute professional advice or recommendation. Please seek advice from a qualified professional, including a thorough examination of your specific legal, accounting and tax situation.

https://www.vanguard.ca/en/insights/canada-outlook

The opinions expressed in this article are of the fund company that owns this content and do not constitute professional advice or recommendation. Please seek advice from a qualified professional, including a thorough examination of your specific legal, accounting and tax situation.

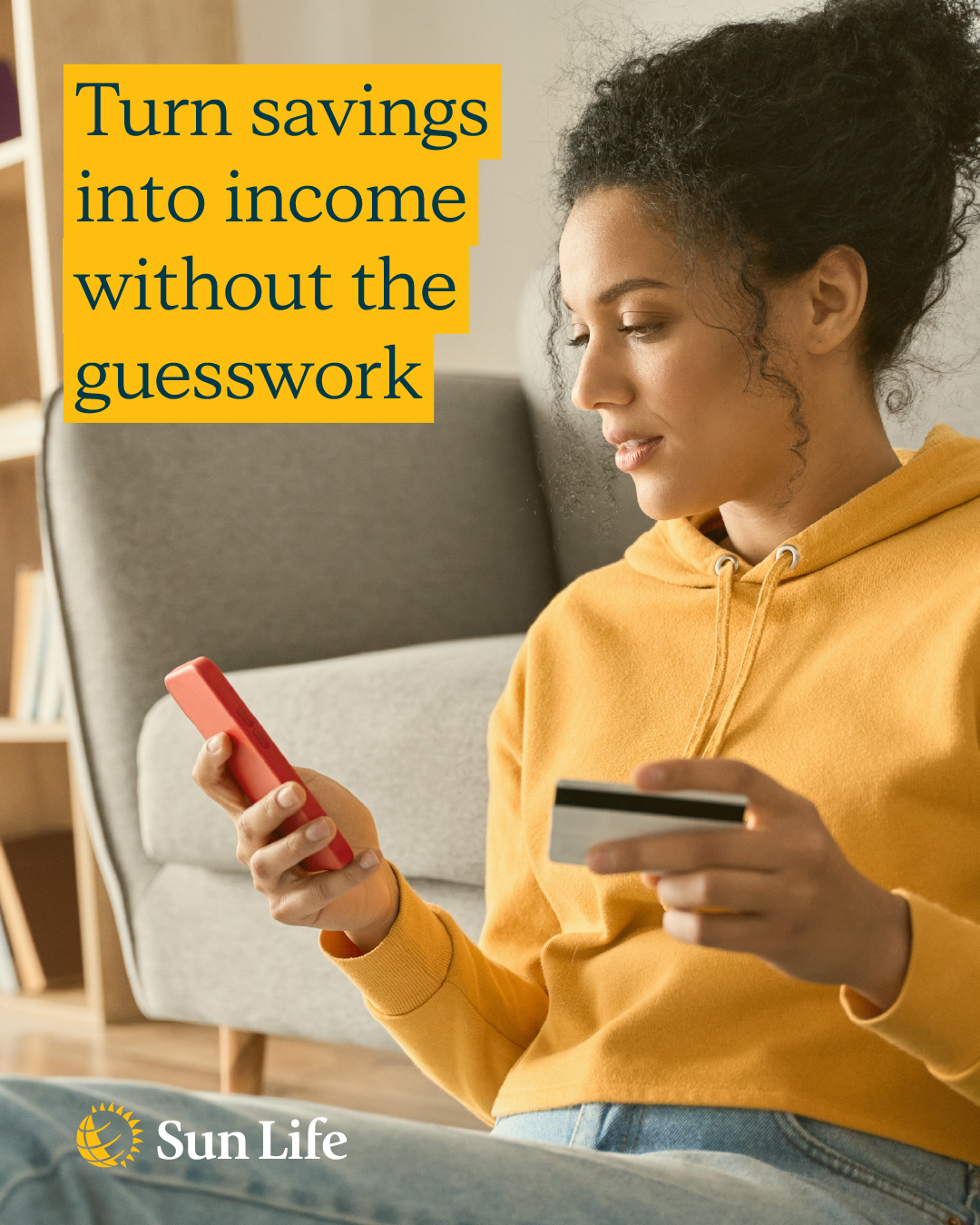

A withdrawal strategy can help create dependable income while helping you manage risk. Let’s chat about income planning basics that fit your needs. https://advisor.sunlife.ca/sandeep.bawa

A withdrawal strategy can help create dependable income while helping you manage risk. Let’s chat about income planning basics that fit your needs. https://advisor.sunlife.ca/sandeep.bawa

La période des impôts ne consiste pas seulement à produire une déclaration de revenus, mais aussi à se préparer. Des cotisations aux REER aux stratégies de fractionnement du revenu, il existe des mesures que vous pouvez prendre pour mieux positionner vos finances pour l’année prochaine et les suivantes.

Communiquez avec moi pour découvrir les stratégies qui vous conviennent le mieux. https://conseiller.sunlife.ca/f/sandeep.bawa

Communiquez avec moi pour découvrir les stratégies qui vous conviennent le mieux. https://conseiller.sunlife.ca/f/sandeep.bawa

La période des impôts ne consiste pas seulement à produire une déclaration de revenus, mais aussi à se préparer. Des cotisations aux REER aux stratégies de fractionnement du revenu, il existe des mesures que vous pouvez prendre pour mieux positionner vos finances pour l’année prochaine et les suivantes.

Communiquez avec moi pour découvrir les stratégies qui vous conviennent le mieux. https://conseiller.sunlife.ca/f/sandeep.bawa

Communiquez avec moi pour découvrir les stratégies qui vous conviennent le mieux. https://conseiller.sunlife.ca/f/sandeep.bawa

Have questions?

Here to help answer your questions, provide clarity about products and get you started on the road to achieving your goals.