Stay informed

Stay informed with what’s going on. Browse posts that might be helpful to you or check out an event happening in your area. Come back regularly as this page is kept up-to-date with a lot of relevant information.

You’ve worked hard to build your business, but without clear next steps, transitions could put it at risk.

A clear succession strategy can help protect your business, support your team, and create a smoother path forward. Book a quick chat to discuss your next steps. https://advisor.sunlife.ca/scott.buckley

A clear succession strategy can help protect your business, support your team, and create a smoother path forward. Book a quick chat to discuss your next steps. https://advisor.sunlife.ca/scott.buckley

You’ve worked hard to build your business, but without clear next steps, transitions could put it at risk.

A clear succession strategy can help protect your business, support your team, and create a smoother path forward. Book a quick chat to discuss your next steps. https://advisor.sunlife.ca/scott.buckley

A clear succession strategy can help protect your business, support your team, and create a smoother path forward. Book a quick chat to discuss your next steps. https://advisor.sunlife.ca/scott.buckley

Health events can happen without warning — and the costs aren’t always medical. Critical illness insurance can provide financial support during a serious diagnosis, helping with time off work, travel for care, or everyday expenses so you can focus on recovery. Want to explore if it fits your plan? https://advisor.sunlife.ca/scott.buckley

Health events can happen without warning — and the costs aren’t always medical. Critical illness insurance can provide financial support during a serious diagnosis, helping with time off work, travel for care, or everyday expenses so you can focus on recovery. Want to explore if it fits your plan? https://advisor.sunlife.ca/scott.buckley

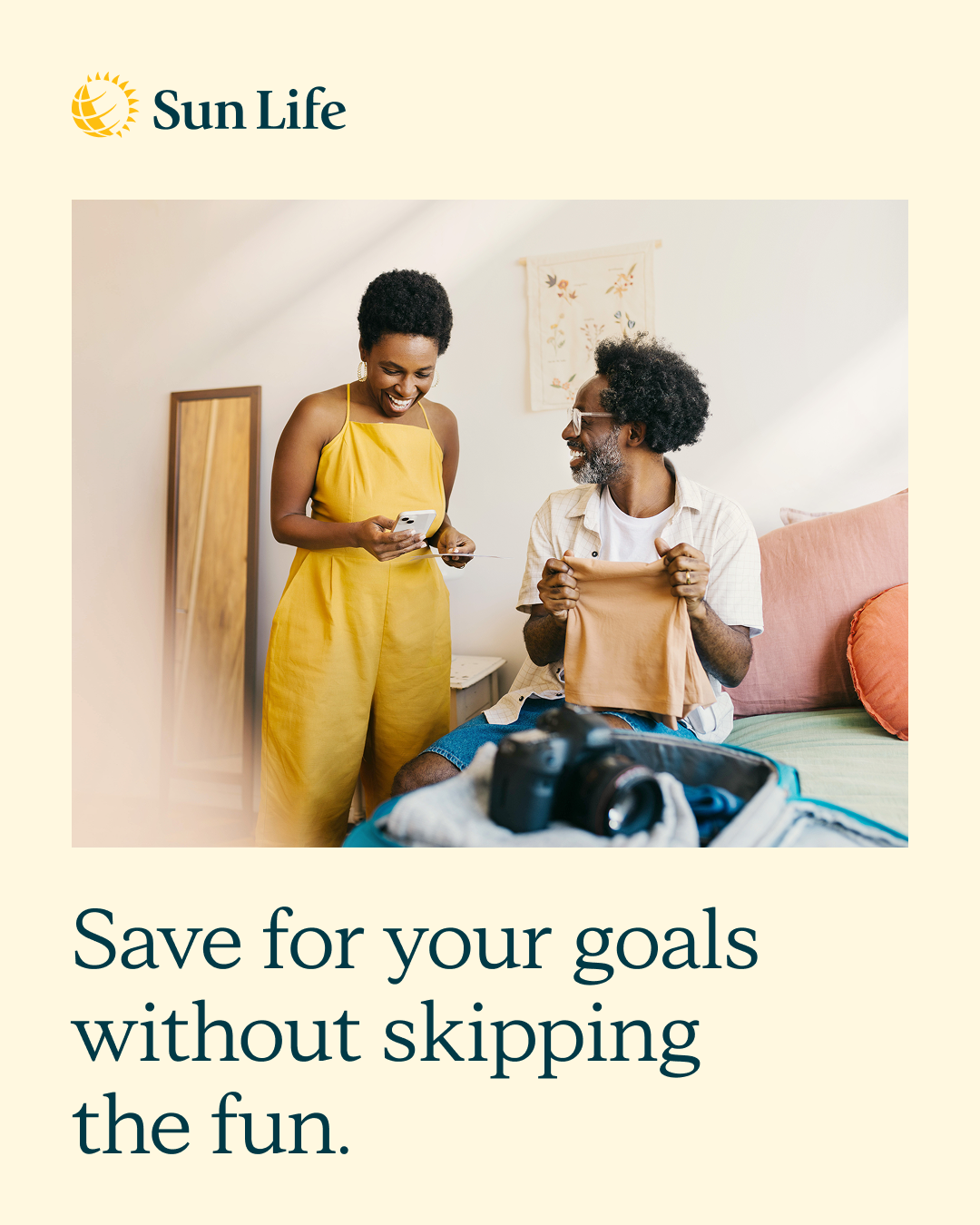

Saving for your goals shouldn’t mean skipping the fun. Whether you’re planning travel, a wedding, a big experience or your next “chapter,” the right strategy can help you set aside cash intentionally while still staying on track. Let's transform your priorities into a financial roadmap you can commit to. https://advisor.sunlife.ca/scott.buckley

Saving for your goals shouldn’t mean skipping the fun. Whether you’re planning travel, a wedding, a big experience or your next “chapter,” the right strategy can help you set aside cash intentionally while still staying on track. Let's transform your priorities into a financial roadmap you can commit to. https://advisor.sunlife.ca/scott.buckley

Greater wealth can bring greater complexity. From tax-aware approaches to estate considerations, having a thoughtful plan in place can help you protect and preserve what matters most — today and for the future. Let’s help simplify your next steps with a personalized roadmap. https://advisor.sunlife.ca/scott.buckley

Greater wealth can bring greater complexity. From tax-aware approaches to estate considerations, having a thoughtful plan in place can help you protect and preserve what matters most — today and for the future. Let’s help simplify your next steps with a personalized roadmap. https://advisor.sunlife.ca/scott.buckley

When your money is spread across different accounts, having one clear plan can help it work better for you over time. If you’re managing milestone goals like a home, family, retirement, or what you want to leave behind, it helps when everything connects. Let’s put a strategy together that helps support what you want next. https://advisor.sunlife.ca/scott.buckley

When your money is spread across different accounts, having one clear plan can help it work better for you over time. If you’re managing milestone goals like a home, family, retirement, or what you want to leave behind, it helps when everything connects. Let’s put a strategy together that helps support what you want next. https://advisor.sunlife.ca/scott.buckley

Ease into retirement with Sun Life One Plan

Your retirement plan should feel unique and tailored to you. Sun Life One Plan can help bring your goals, investments and income strategy together so you can see what’s possible. Get in touch to start planning your dream retirement. https://advisor.sunlife.ca/scott.buckley

#SunLifeOnePlan #RetirementPlanning

#SunLifeOnePlan #RetirementPlanning

Watch video

Unexpected events don’t send calendar invites. A back-up plan can help your business stay steady if a key person becomes suddenly unavailable, or revenue unexpectedly dips. Let’s pressure-test “what ifs” for your business and build a strategy that helps protect both your company and your personal finances. https://advisor.sunlife.ca/scott.buckley

Unexpected events don’t send calendar invites. A back-up plan can help your business stay steady if a key person becomes suddenly unavailable, or revenue unexpectedly dips. Let’s pressure-test “what ifs” for your business and build a strategy that helps protect both your company and your personal finances. https://advisor.sunlife.ca/scott.buckley

Disability can impact more than just your income — it can affect your financial priorities all at once. The right coverage can help create breathing room if you’re unable to work due to illness or injury. If your paycheque fuels your plans, they may be worth protecting. Get in touch to talk about your options. https://advisor.sunlife.ca/scott.buckley

Disability can impact more than just your income — it can affect your financial priorities all at once. The right coverage can help create breathing room if you’re unable to work due to illness or injury. If your paycheque fuels your plans, they may be worth protecting. Get in touch to talk about your options. https://advisor.sunlife.ca/scott.buckley

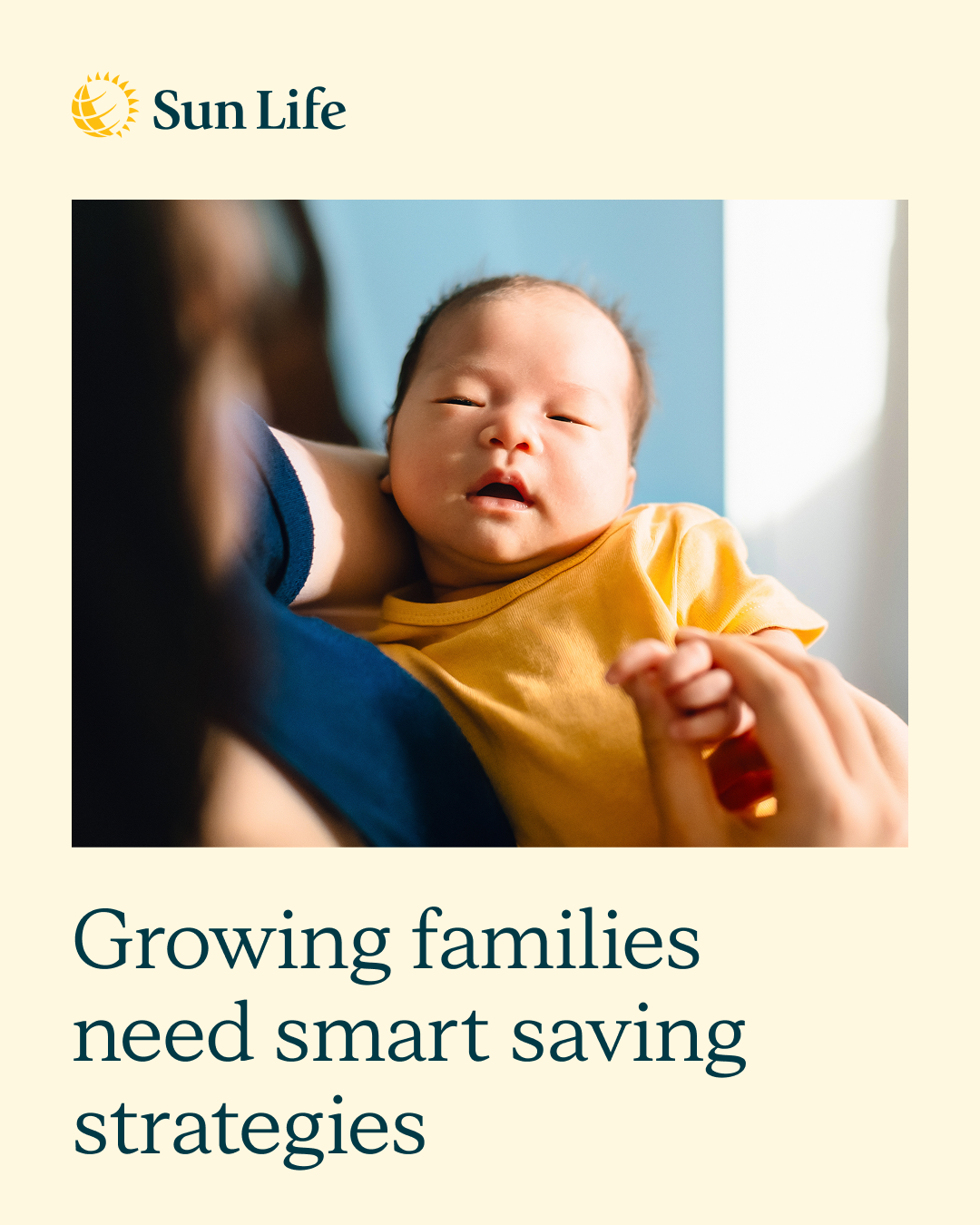

A growing family is exciting — and it changes everything from monthly cash flow to longer-term goals. Childcare, activities, housing, education… it adds up fast. A realistic plan can help you balance today’s costs while still making progress on what matters most.

A growing family is exciting — and it changes everything from monthly cash flow to longer-term goals. Childcare, activities, housing, education… it adds up fast. A realistic plan can help you balance today’s costs while still making progress on what matters most.

As wealth grows, so does complexity. Smart financial strategies look beyond traditional investing to financial roadmaps that help protect, grow, and transfer wealth more efficiently. From insurance, as part of an estate strategy, to broader diversification, we help bring the pieces together. Book a quick review.

As wealth grows, so does complexity. Smart financial strategies look beyond traditional investing to financial roadmaps that help protect, grow, and transfer wealth more efficiently. From insurance, as part of an estate strategy, to broader diversification, we help bring the pieces together. Book a quick review.

A tax refund can feel like “extra” money — but it can also be a powerful planning moment. Putting it toward the right goal (RRSP, TFSA, debt strategy, or a targeted savings plan) can help you build momentum. The best move depends on your priorities — and your timeline. Let’s chat about your goals.

A tax refund can feel like “extra” money — but it can also be a powerful planning moment. Putting it toward the right goal (RRSP, TFSA, debt strategy, or a targeted savings plan) can help you build momentum. The best move depends on your priorities — and your timeline. Let’s chat about your goals.

Your retirement plan should feel personal — not generic. Sun Life One Plan can help bring your goals, investments and income strategy together into one clear financial roadmap, so you can see what’s possible and adjust as life changes. What would you like your retirement to look like? https://advisor.sunlife.ca/scott.buckley

#SunLifeOnePlan #RetirementPlanning

#SunLifeOnePlan #RetirementPlanning

Your retirement plan should feel personal — not generic. Sun Life One Plan can help bring your goals, investments and income strategy together into one clear financial roadmap, so you can see what’s possible and adjust as life changes. What would you like your retirement to look like? https://advisor.sunlife.ca/scott.buckley

#SunLifeOnePlan #RetirementPlanning

#SunLifeOnePlan #RetirementPlanning

A business built for the long term needs more than cash flow. Clear routines, healthy boundaries and the right support helps teams stay engaged and productive. Let’s chat about how we can work together to support your staff and business goals.

A business built for the long term needs more than cash flow. Clear routines, healthy boundaries and the right support helps teams stay engaged and productive. Let’s chat about how we can work together to support your staff and business goals.

Your mortgage is likely one of your biggest financial commitments. What happens to it if something unexpected occurs? Mortgage protection insurance helps ensure your family can keep your home secure, no matter what life brings. Let's review your coverage and give you peace of mind. Reach out to discuss your options today.

https://advisor.sunlife.ca/scott.buckley

https://advisor.sunlife.ca/scott.buckley

Your mortgage is likely one of your biggest financial commitments. What happens to it if something unexpected occurs? Mortgage protection insurance helps ensure your family can keep your home secure, no matter what life brings. Let's review your coverage and give you peace of mind. Reach out to discuss your options today.

https://advisor.sunlife.ca/scott.buckley

https://advisor.sunlife.ca/scott.buckley

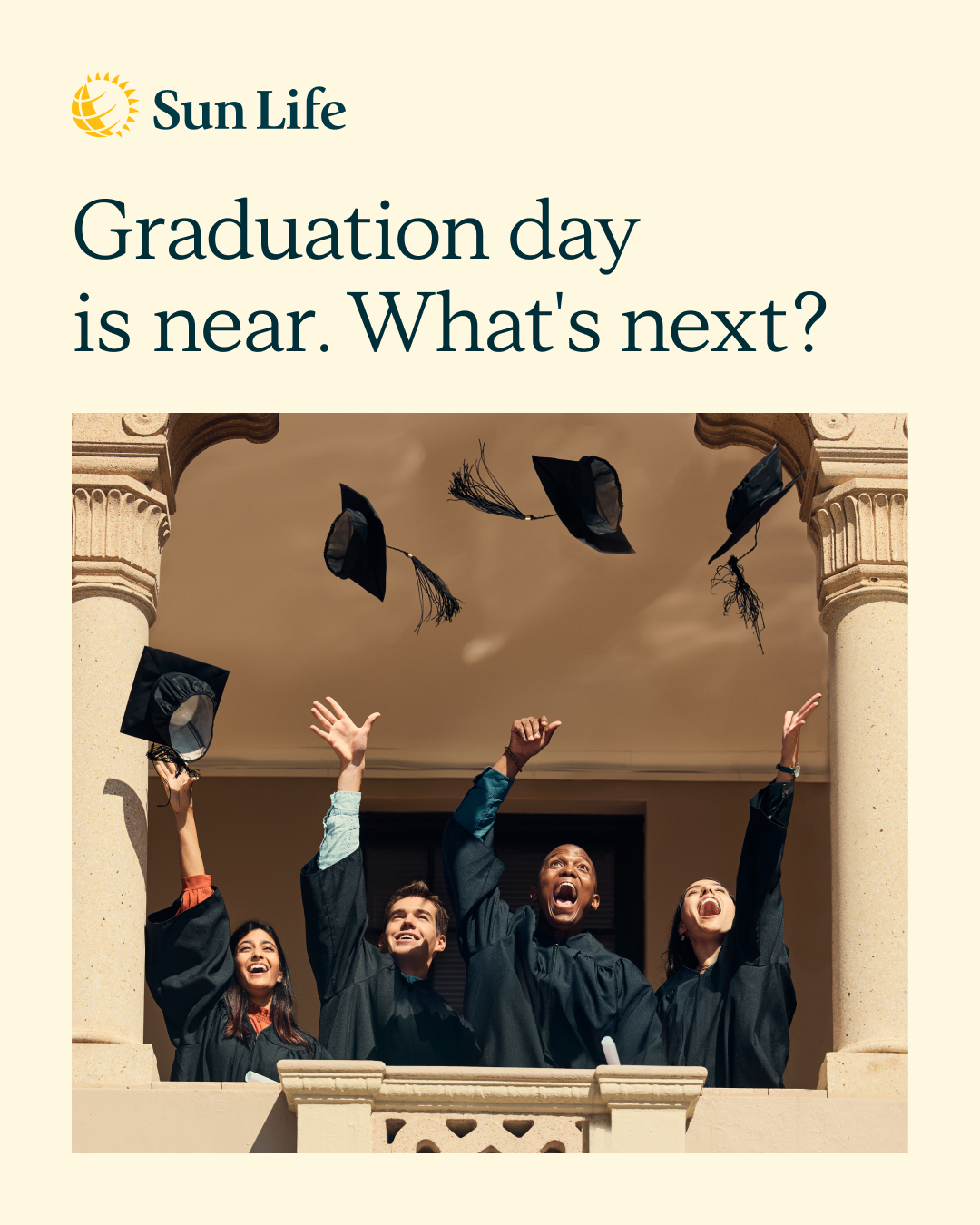

Congratulations on graduating! Now comes the next chapter, managing student debt while building your future. From repayment strategies to integrating loans into your financial roadmap, let's make sure you're set up for success. Whether it's buying a first home or saving for further education, we can help you navigate it all. Let's talk!

Congratulations on graduating! Now comes the next chapter, managing student debt while building your future. From repayment strategies to integrating loans into your financial roadmap, let's make sure you're set up for success. Whether it's buying a first home or saving for further education, we can help you navigate it all. Let's talk!

When your finances are complex, an intentional strategy can be helpful. Coordinating taxes, investments and protection can help you preserve what you’ve built — and make it easier to pass on. Transferring wealth can be about more than assets; it’s about values, fairness, and protecting the people you care about. With the right planning, you can help reduce friction, manage tax impacts and keep your legacy aligned with your wishes. Let’s talk about a strategy that works best for your family and future. https://advisor.sunlife.ca/scott.buckley

When your finances are complex, an intentional strategy can be helpful. Coordinating taxes, investments and protection can help you preserve what you’ve built — and make it easier to pass on. Transferring wealth can be about more than assets; it’s about values, fairness, and protecting the people you care about. With the right planning, you can help reduce friction, manage tax impacts and keep your legacy aligned with your wishes. Let’s talk about a strategy that works best for your family and future. https://advisor.sunlife.ca/scott.buckley

Taxes complete? Now is the perfect time to think bigger. Your tax refund is an opportunity to strengthen your financial foundation. Whether it's boosting RRSP contributions, maximizing investment strategies or planning for next year, let's help ensure every dollar works harder for you. Questions about how to best utilize your tax return? Let's chat!

https://advisor.sunlife.ca/scott.buckley

https://advisor.sunlife.ca/scott.buckley

Taxes complete? Now is the perfect time to think bigger. Your tax refund is an opportunity to strengthen your financial foundation. Whether it's boosting RRSP contributions, maximizing investment strategies or planning for next year, let's help ensure every dollar works harder for you. Questions about how to best utilize your tax return? Let's chat!

https://advisor.sunlife.ca/scott.buckley

https://advisor.sunlife.ca/scott.buckley

Thinking about retirement? Move from “a number” to a real plan. Income, timing, taxes and how you’ll use your savings all work better when they’re aligned. The sooner you explore your options, the more choices you may have later.

Thinking about retirement? Move from “a number” to a real plan. Income, timing, taxes and how you’ll use your savings all work better when they’re aligned. The sooner you explore your options, the more choices you may have later.

Every business needs a backup plan. Contingency planning means identifying risks— from cash flow disruptions to key person loss. Having strategies in place to weather the storm isn't about being pessimistic; it's about being prepared. What keeps you up at night? Let's build more resilience into your financial strategy so you can sleep peacefully. Reach out to set up a time to chat. https://advisor.sunlife.ca/scott.buckley

Every business needs a backup plan. Contingency planning means identifying risks— from cash flow disruptions to key person loss. Having strategies in place to weather the storm isn't about being pessimistic; it's about being prepared. What keeps you up at night? Let's build more resilience into your financial strategy so you can sleep peacefully. Reach out to set up a time to chat. https://advisor.sunlife.ca/scott.buckley

Why choose between protection and savings when you can have both? Bundle term and permanent life insurance to save 10% for life on your permanent policy, AND get money back on critical illness coverage.

Build complete protection for multiple life scenarios while maximizing your savings. Let's talk about your protection needs!

Build complete protection for multiple life scenarios while maximizing your savings. Let's talk about your protection needs!

Why choose between protection and savings when you can have both? Bundle term and permanent life insurance to save 10% for life on your permanent policy, AND get money back on critical illness coverage.

Build complete protection for multiple life scenarios while maximizing your savings. Let's talk about your protection needs!

Build complete protection for multiple life scenarios while maximizing your savings. Let's talk about your protection needs!

Have questions?

Here to help answer your questions, provide clarity about products and get you started on the road to achieving your goals.