Stay informed

Stay informed with what’s going on. Browse posts that might be helpful to you or check out an event happening in your area. Come back regularly as this page is kept up-to-date with a lot of relevant information.

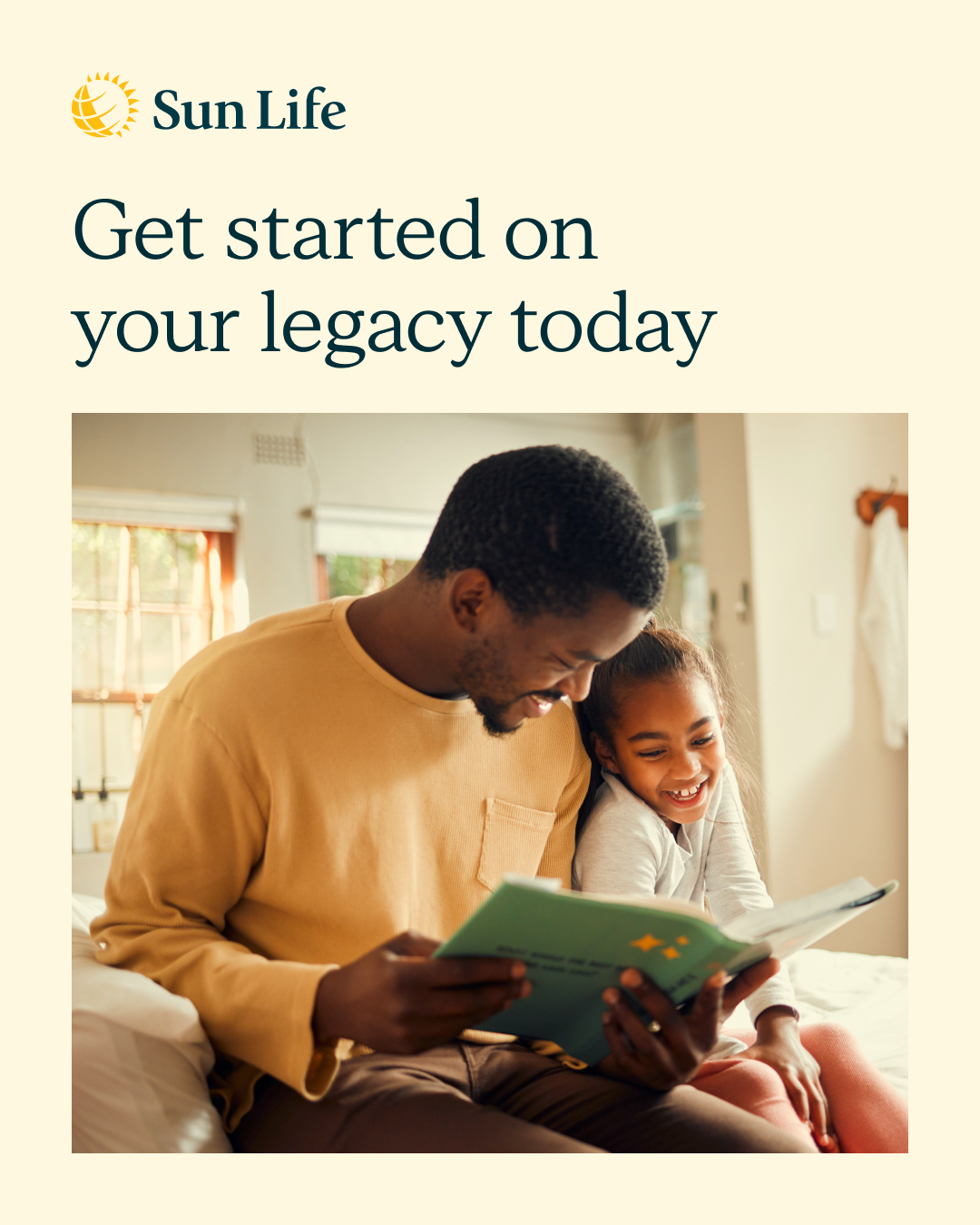

Thinking about what you'll leave behind? Intergenerational planning is more than just numbers — it's about passing on your values, your dreams and your wealth to those you love. Whether you're thinking about your children, grandchildren or other VIPs in your life, let's create a strategy that helps ensure your legacy reflects your vision. Ready to get started on leaving your legacy? Let’s chat!

https://advisor.sunlife.ca/steven.zhang

https://advisor.sunlife.ca/steven.zhang

Thinking about what you'll leave behind? Intergenerational planning is more than just numbers — it's about passing on your values, your dreams and your wealth to those you love. Whether you're thinking about your children, grandchildren or other VIPs in your life, let's create a strategy that helps ensure your legacy reflects your vision. Ready to get started on leaving your legacy? Let’s chat!

https://advisor.sunlife.ca/steven.zhang

https://advisor.sunlife.ca/steven.zhang

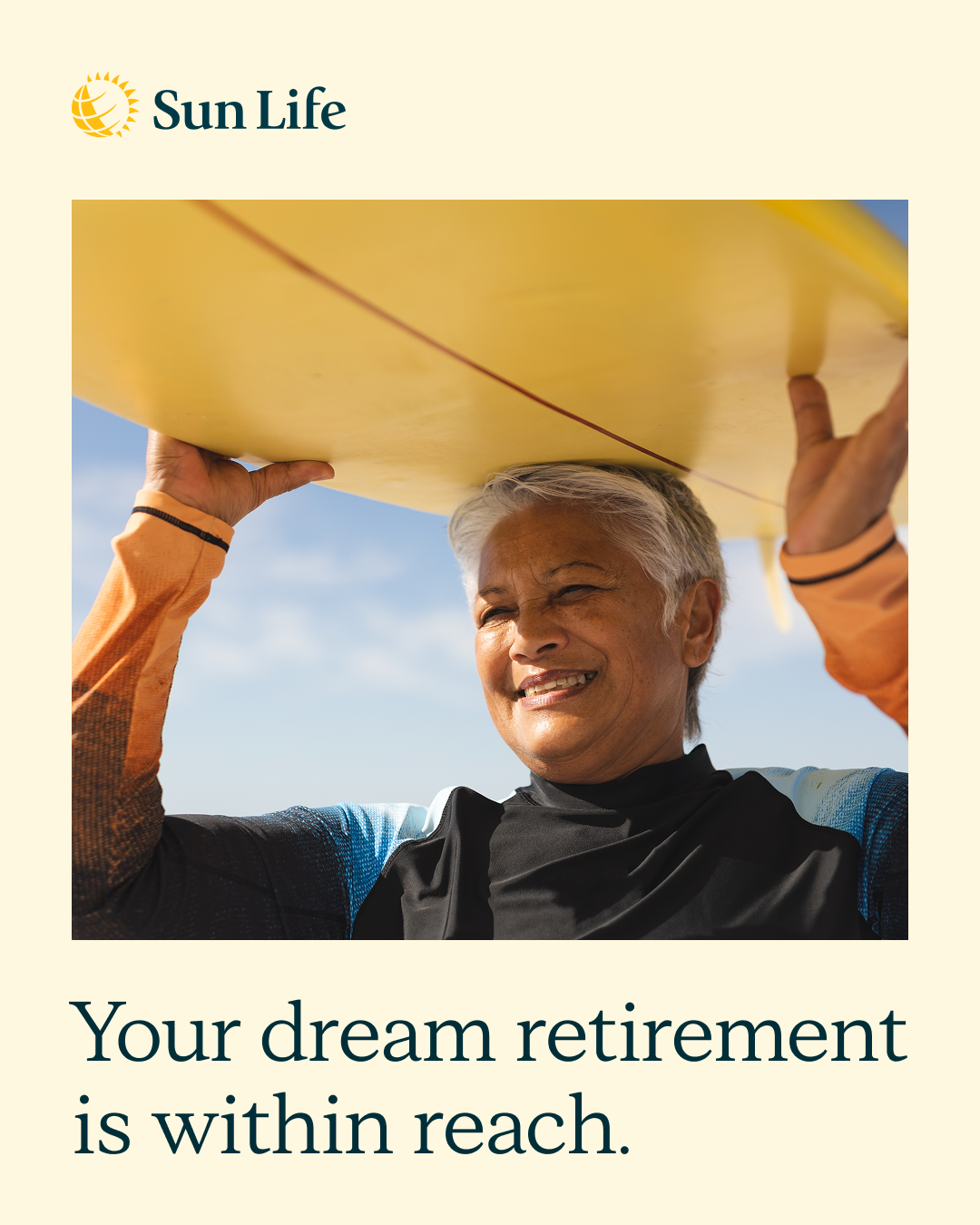

Retirement isn't just a number, it's a lifestyle. Whether you're dreaming of early retirement, a career shift or phased transition, we can help turn those dreams into reality. From income planning to investment strategy, let's create a one-of-a-kind roadmap using Sun Life One Plan. Your retirement story starts here. What does your ideal retirement look like? https://advisor.sunlife.ca/steven.zhang

#SunLifeOnePlan #RetirementPlanning

#SunLifeOnePlan #RetirementPlanning

Retirement isn't just a number, it's a lifestyle. Whether you're dreaming of early retirement, a career shift or phased transition, we can help turn those dreams into reality. From income planning to investment strategy, let's create a one-of-a-kind roadmap using Sun Life One Plan. Your retirement story starts here. What does your ideal retirement look like? https://advisor.sunlife.ca/steven.zhang

#SunLifeOnePlan #RetirementPlanning

#SunLifeOnePlan #RetirementPlanning

Your employees are your greatest asset. A healthy workplace culture built on trust, flexibility, and support can improve retention, productivity and long-term growth. From prioritizing mental well-being to encouraging healthy habits, small changes can make a big impact. Ready to strengthen your workplace? Let’s start the conversation. https://advisor.sunlife.ca/steven.zhang

Your employees are your greatest asset. A healthy workplace culture built on trust, flexibility, and support can improve retention, productivity and long-term growth. From prioritizing mental well-being to encouraging healthy habits, small changes can make a big impact. Ready to strengthen your workplace? Let’s start the conversation. https://advisor.sunlife.ca/steven.zhang

Your leisure goals matter just as much as your long-term plans. Whether it's a dream vacation or a weekend getaway, let's build a savings strategy that lets you enjoy life now while securing your future. Small contributions can add up fast. Let’s chat about options that work for you. https://advisor.sunlife.ca/steven.zhang

Your leisure goals matter just as much as your long-term plans. Whether it's a dream vacation or a weekend getaway, let's build a savings strategy that lets you enjoy life now while securing your future. Small contributions can add up fast. Let’s chat about options that work for you. https://advisor.sunlife.ca/steven.zhang

Multiple accounts, properties and investments? Sun Life One Plan can help bring it all together, allowing you to see more of the complete picture. Let's work together to align your goals, timelines and risk comfort. #SunLifeOnePlan

Multiple accounts, properties and investments? Sun Life One Plan can help bring it all together, allowing you to see more of the complete picture. Let's work together to align your goals, timelines and risk comfort. #SunLifeOnePlan

Small steps can lead to big wins when it comes to your financial future. Start building a solid foundation with smart strategies for debt management, investing and automated savings. Your future self will thank you.

Let’s connect to discuss how we can work together to create a personalized financial roadmap that’s tailored to your life goals.

#FinancialRoadmap #SunLifeOnePlan #PersonalWealth

Let’s connect to discuss how we can work together to create a personalized financial roadmap that’s tailored to your life goals.

#FinancialRoadmap #SunLifeOnePlan #PersonalWealth

Small steps can lead to big wins when it comes to your financial future. Start building a solid foundation with smart strategies for debt management, investing and automated savings. Your future self will thank you.

Let’s connect to discuss how we can work together to create a personalized financial roadmap that’s tailored to your life goals.

#FinancialRoadmap #SunLifeOnePlan #PersonalWealth

Let’s connect to discuss how we can work together to create a personalized financial roadmap that’s tailored to your life goals.

#FinancialRoadmap #SunLifeOnePlan #PersonalWealth

Think comprehensive insurance protection is out of reach? Think again. Our spring offers make it easier and more affordable to cover all your bases. Save 10% on permanent life insurance, plus you can get cash back on critical illness insurance premiums.

Let's find the right solution for your needs!

Let's find the right solution for your needs!

Think comprehensive insurance protection is out of reach? Think again. Our spring offers make it easier and more affordable to cover all your bases. Save 10% on permanent life insurance, plus you can get cash back on critical illness insurance premiums.

Let's find the right solution for your needs!

Let's find the right solution for your needs!

Canada 2026 Q2 Outlook: Resilience amid geopolitical crosscurrents | Vanguard Canada

Access helpful resources on financial knowledge developed by professionals in the industry.

https://www.vanguard.ca/en/insights/canada-outlook

The opinions expressed in this article are of the fund company that owns this content and do not constitute professional advice or recommendation. Please seek advice from a qualified professional, including a thorough examination of your specific legal, accounting and tax situation

https://www.vanguard.ca/en/insights/canada-outlook

The opinions expressed in this article are of the fund company that owns this content and do not constitute professional advice or recommendation. Please seek advice from a qualified professional, including a thorough examination of your specific legal, accounting and tax situation

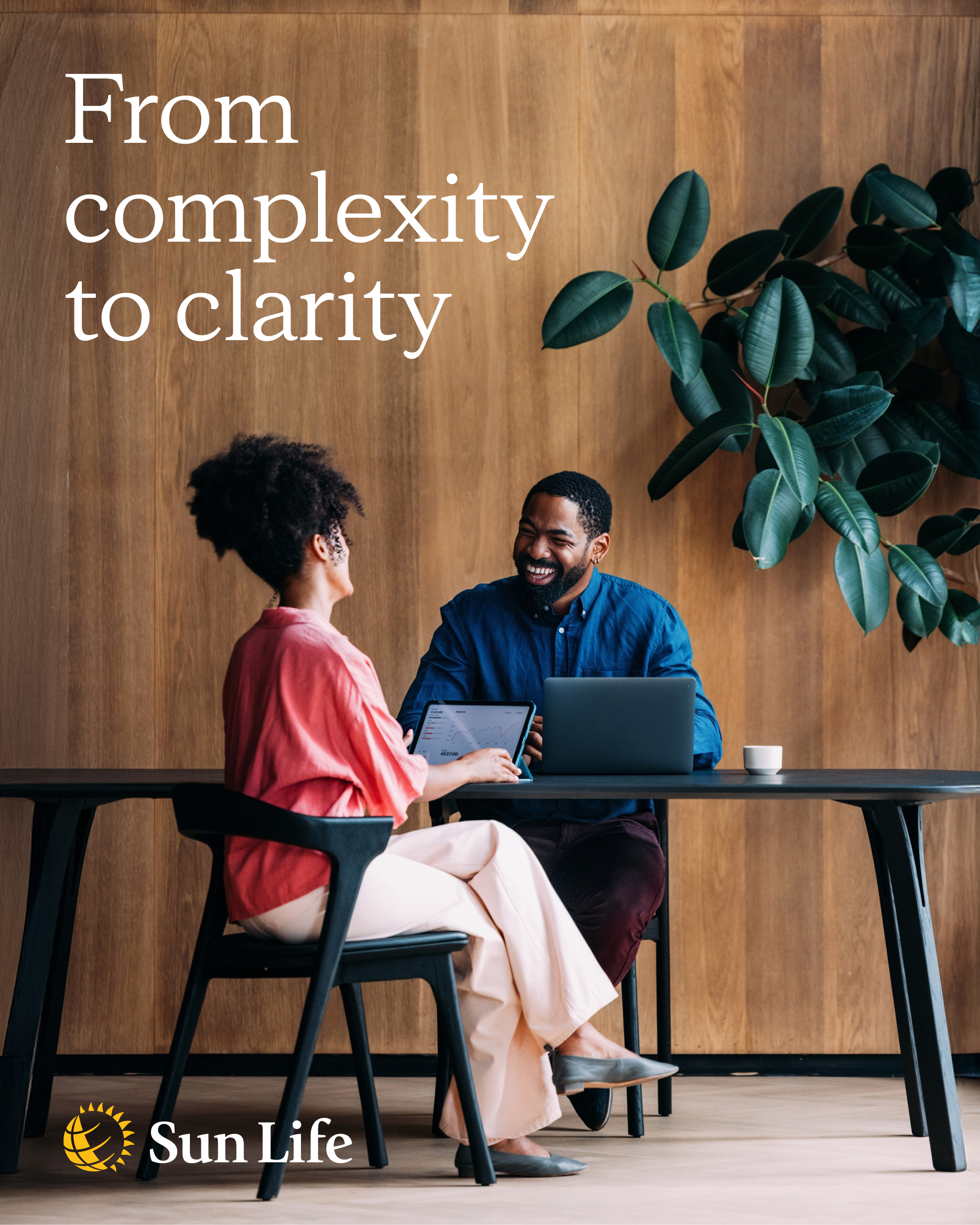

Your financial future deserves a tailored approach. With Sun Life One Plan, you can simplify decisions for your personal finances. From tax strategies to succession planning, a comprehensive roadmap helps you protect what you've built while planning for what's ahead. Learn more: https://sunlife.hubs.vidyard.com/watch/ksLWJjT43furjobhkXkgiQ.

Let's book time to develop your personalized Sun Life One Plan. Reach out today.

#SunLifeOnePlan #FinancialSecurity

Let's book time to develop your personalized Sun Life One Plan. Reach out today.

#SunLifeOnePlan #FinancialSecurity

Your financial future deserves a tailored approach. With Sun Life One Plan, you can simplify decisions for your personal finances. From tax strategies to succession planning, a comprehensive roadmap helps you protect what you've built while planning for what's ahead. Learn more: https://sunlife.hubs.vidyard.com/watch/ksLWJjT43furjobhkXkgiQ.

Let's book time to develop your personalized Sun Life One Plan. Reach out today.

#SunLifeOnePlan #FinancialSecurity

Let's book time to develop your personalized Sun Life One Plan. Reach out today.

#SunLifeOnePlan #FinancialSecurity

Your tax refund is an opportunity to invest in the future. Instead of letting it sit, let's explore smart ways to put it to work. From RRSP contributions to investment strategies, there are options to help grow your wealth. Let's explore what works best for your goals. https://advisor.sunlife.ca/steven.zhang

Your tax refund is an opportunity to invest in the future. Instead of letting it sit, let's explore smart ways to put it to work. From RRSP contributions to investment strategies, there are options to help grow your wealth. Let's explore what works best for your goals. https://advisor.sunlife.ca/steven.zhang

Thinking about retirement? You're not alone — and the good news is you don't have to navigate it solo. Let's create a personalized retirement roadmap. Together we can explore income strategies, investment options and timelines that fit your vision. Get in touch today!

Thinking about retirement? You're not alone — and the good news is you don't have to navigate it solo. Let's create a personalized retirement roadmap. Together we can explore income strategies, investment options and timelines that fit your vision. Get in touch today!

Growing your business means managing more than just revenue. Smart cash-flow planning helps you balance reinvestment with personal financial security.

Let's explore strategies to optimize how money flows through your business and into your personal wealth roadmap. Book a Sun Life One Plan conversation today.

#SunLifeOnePlan

Let's explore strategies to optimize how money flows through your business and into your personal wealth roadmap. Book a Sun Life One Plan conversation today.

#SunLifeOnePlan

Growing your business means managing more than just revenue. Smart cash-flow planning helps you balance reinvestment with personal financial security.

Let's explore strategies to optimize how money flows through your business and into your personal wealth roadmap. Book a Sun Life One Plan conversation today.

#SunLifeOnePlan

Let's explore strategies to optimize how money flows through your business and into your personal wealth roadmap. Book a Sun Life One Plan conversation today.

#SunLifeOnePlan

Heart Disease: Young Adults With Hypertension Have 27% Higher Risk

Young Adults With High Blood Pressure Face Higher Risk of Heart, Kidney Disease.https://advisor.sunlife.ca/steven.zhang

Heart Disease: Young Adults With Hypertension Have 27% Higher Risk

Young Adults With High Blood Pressure Face Higher Risk of Heart, Kidney Disease.https://advisor.sunlife.ca/steven.zhang

Positive Beliefs About Aging Can Influence Wellness

No matter your age, is it time to update beliefs about what aging is and is not?https://advisor.sunlife.ca/steven.zhang

Parents, help secure your kids' future today. Lock in lower premiums and guaranteed coverage with Sun CII for children. Bonus: For a limited time, get 50% off their first year of premiums! Offer ends July 31. #ChildInsurance #PlanningAhead

Parents, help secure your kids' future today. Lock in lower premiums and guaranteed coverage with Sun CII for children. Bonus: For a limited time, get 50% off their first year of premiums! Offer ends July 31. #ChildInsurance #PlanningAhead

Tax write-offs that Canadians often get wrong

Tax season brings plenty of confusion—and costly mistakes. Here are some commonly misunderstood expenses Canadians often try (but fail) to claim on their tax returns.

https://advisor.sunlife.ca/steven.zhang

https://advisor.sunlife.ca/steven.zhang

The New 65: Why the Healthiest Retirees Are Planning for 30 More Years

Planning to live to 95? Why your retirement strategy needs a 'healthspan' reset.https://advisor.sunlife.ca/steven.zhang

Limited time offer! Help protect your family with Sun Critical Illness Insurance and save on your first year. Prepare for the unexpected and get peace of mind for less. Offer ends July 31. #InsuranceSavings #FamilyProtection

Limited time offer! Help protect your family with Sun Critical Illness Insurance and save on your first year. Prepare for the unexpected and get peace of mind for less. Offer ends July 31. #InsuranceSavings #FamilyProtection

Lock in lower rates ✓ Guarantee coverage ✓ Secure their future ✓

Help secure your little one's future today. Sun CII for kids locks in lower premiums and guarantees coverage as they grow. Plus, get 50% of their first year's premiums back! Offer ends July 31. #ParentingWin #ChildInsurance

Watch video

Have questions?

Here to help answer your questions, provide clarity about products and get you started on the road to achieving your goals.

We are contracted with Sun Life Financial Distributors (Canada) Inc., a member of the Sun Life group of companies. Mutual funds distributed by Sun Life Financial Investment Services (Canada) Inc.