Stay informed

Stay informed with what’s going on. Browse posts that might be helpful to you or check out an event happening in your area. Come back regularly as this page is kept up-to-date with a lot of relevant information.

Running a business today often means managing rising costs, tighter margins and constant pressure on cash flow. A clear financial approach can help you stay in control, manage expenses, protect against risk and keep your business moving forward.

Let’s review your strategy to find ways to strengthen your margins.https://advisor.sunlife.ca/vitalis.financial.services/

Let’s review your strategy to find ways to strengthen your margins.https://advisor.sunlife.ca/vitalis.financial.services/

Running a business today often means managing rising costs, tighter margins and constant pressure on cash flow. A clear financial approach can help you stay in control, manage expenses, protect against risk and keep your business moving forward.

Let’s review your strategy to find ways to strengthen your margins.https://advisor.sunlife.ca/vitalis.financial.services/

Let’s review your strategy to find ways to strengthen your margins.https://advisor.sunlife.ca/vitalis.financial.services/

Buying a home, growing your family, building your career — there’s a lot to balance. Creating a personalized financial roadmap early can help you stay on track while still living for today. Small steps today can make a meaningful difference over time. Get in touch to discuss options that will work best for you. https://advisor.sunlife.ca/vitalis.financial.services/

Buying a home, growing your family, building your career — there’s a lot to balance. Creating a personalized financial roadmap early can help you stay on track while still living for today. Small steps today can make a meaningful difference over time. Get in touch to discuss options that will work best for you. https://advisor.sunlife.ca/vitalis.financial.services/

You’ve built significant wealth. Now it’s about making it last. With the right approach, you can help reduce tax impacts, protect your estate and create a legacy that supports the people and causes you care about. Let’s build a strategy that helps you move into retirement with clarity and confidence. Book a conversation to start shaping your legacy. https://advisor.sunlife.ca/vitalis.financial.services/

You’ve built significant wealth. Now it’s about making it last. With the right approach, you can help reduce tax impacts, protect your estate and create a legacy that supports the people and causes you care about. Let’s build a strategy that helps you move into retirement with clarity and confidence. Book a conversation to start shaping your legacy. https://advisor.sunlife.ca/vitalis.financial.services/

This week marks 6 years since Christina has been part of the Vitalis Family. Thank you for being an amazing part of the company and for your hard work and dedication! 🎉🎉🎉

This week marks 6 years since Christina has been part of the Vitalis Family. Thank you for being an amazing part of the company and for your hard work and dedication! 🎉🎉🎉

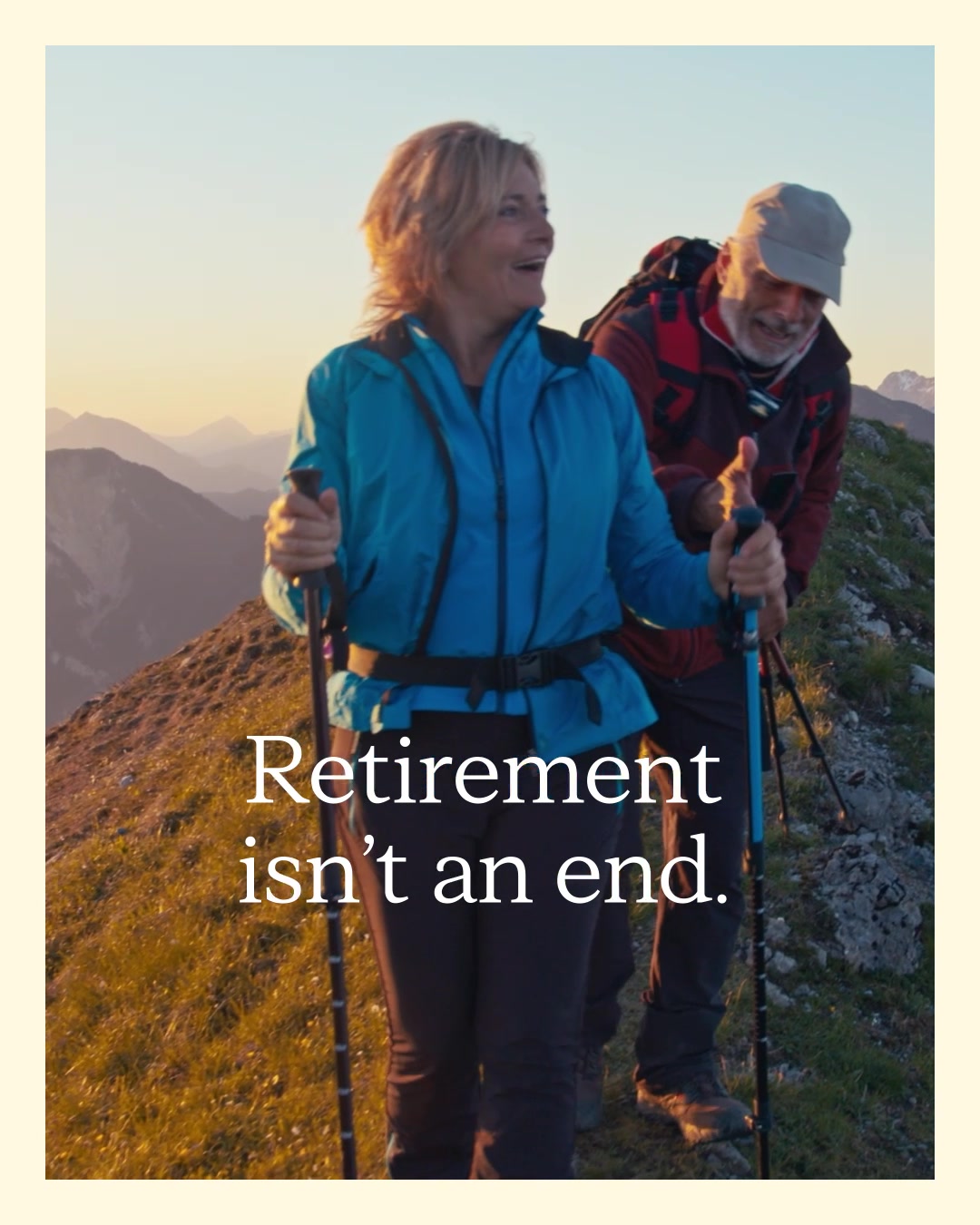

Retirement isn’t an end. It’s your next chapter.

Retirement looks different for everyone. Whether you’re planning to slow down, travel, or explore new passions, having a thoughtful strategy can help you get there with confidence. Explore ways to transition your savings into income that supports the lifestyle you envision. Let’s build a strategy that helps you move into retirement with clarity and confidence.

Watch video

Health events can happen without warning — and the costs aren’t always medical. Critical illness insurance can provide financial support during a serious diagnosis, helping with time off work, travel for care, or everyday expenses so you can focus on recovery. Want to explore if it fits your plan? https://advisor.sunlife.ca/vitalis.financial.services/

Health events can happen without warning — and the costs aren’t always medical. Critical illness insurance can provide financial support during a serious diagnosis, helping with time off work, travel for care, or everyday expenses so you can focus on recovery. Want to explore if it fits your plan? https://advisor.sunlife.ca/vitalis.financial.services/

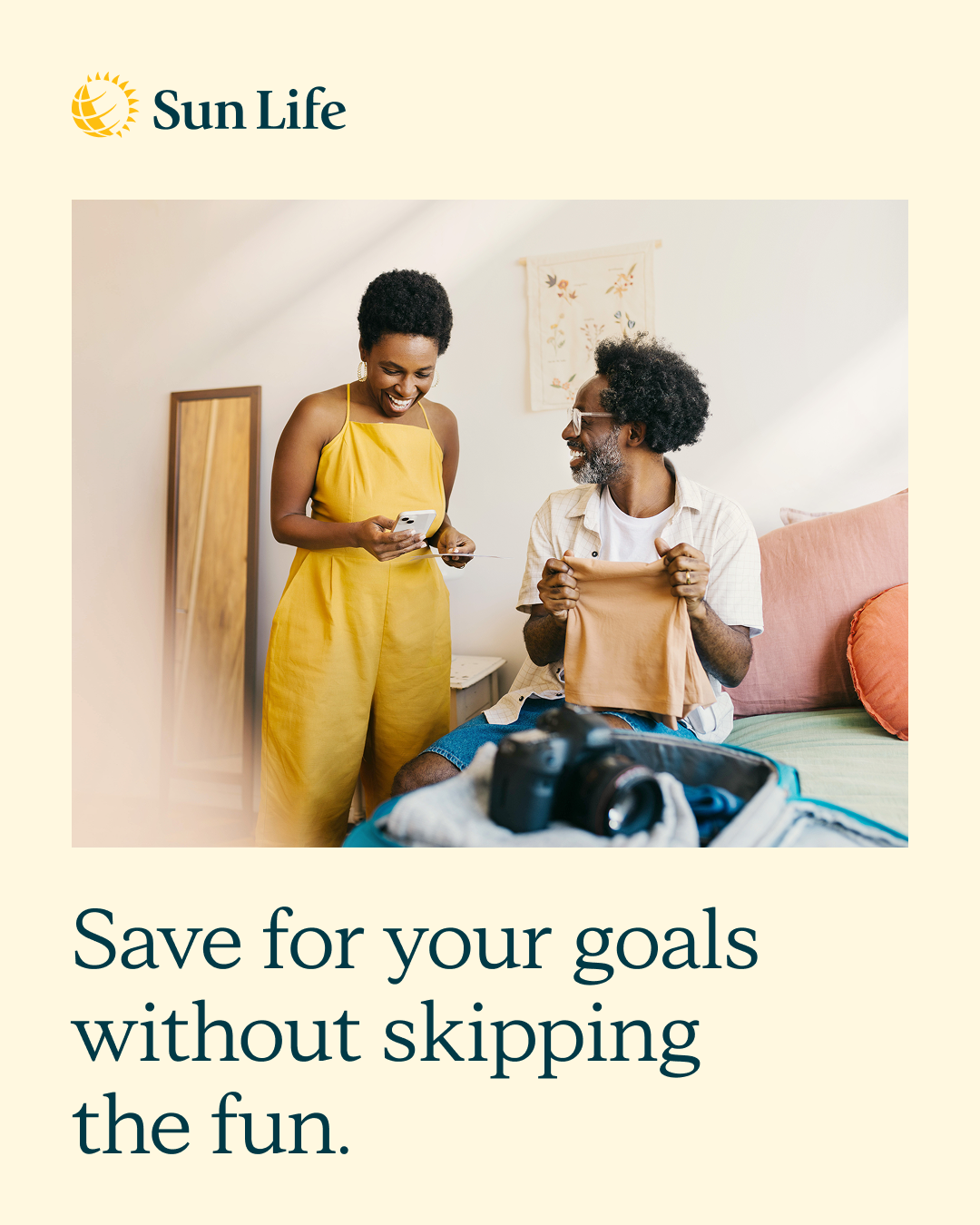

Saving for your goals shouldn’t mean skipping the fun. Whether you’re planning travel, a wedding, a big experience or your next “chapter,” the right strategy can help you set aside cash intentionally while still staying on track. Let's transform your priorities into a financial roadmap you can commit to. https://advisor.sunlife.ca/vitalis.financial.services/

Saving for your goals shouldn’t mean skipping the fun. Whether you’re planning travel, a wedding, a big experience or your next “chapter,” the right strategy can help you set aside cash intentionally while still staying on track. Let's transform your priorities into a financial roadmap you can commit to. https://advisor.sunlife.ca/vitalis.financial.services/

When your money is spread across different accounts, having one clear plan can help it work better for you over time. If you’re managing milestone goals like a home, family, retirement, or what you want to leave behind, it helps when everything connects. Let’s put a strategy together that helps support what you want next. https://advisor.sunlife.ca/vitalis.financial.services/

When your money is spread across different accounts, having one clear plan can help it work better for you over time. If you’re managing milestone goals like a home, family, retirement, or what you want to leave behind, it helps when everything connects. Let’s put a strategy together that helps support what you want next. https://advisor.sunlife.ca/vitalis.financial.services/

Ease into retirement with Sun Life One Plan

Your retirement plan should feel unique and tailored to you. Sun Life One Plan can help bring your goals, investments and income strategy together so you can see what’s possible. Get in touch to start planning your dream retirement. https://advisor.sunlife.ca/vitalis.financial.services/

#SunLifeOnePlan #RetirementPlanning

#SunLifeOnePlan #RetirementPlanning

Watch video

Unexpected events don’t send calendar invites. A back-up plan can help your business stay steady if a key person becomes suddenly unavailable, or revenue unexpectedly dips. Let’s pressure-test “what ifs” for your business and build a strategy that helps protect both your company and your personal finances. https://advisor.sunlife.ca/vitalis.financial.services/

Unexpected events don’t send calendar invites. A back-up plan can help your business stay steady if a key person becomes suddenly unavailable, or revenue unexpectedly dips. Let’s pressure-test “what ifs” for your business and build a strategy that helps protect both your company and your personal finances. https://advisor.sunlife.ca/vitalis.financial.services/

As wealth grows, so does complexity. Smart financial strategies look beyond traditional investing to financial roadmaps that help protect, grow, and transfer wealth more efficiently. From insurance, as part of an estate strategy, to broader diversification, we help bring the pieces together. Book a quick review.

As wealth grows, so does complexity. Smart financial strategies look beyond traditional investing to financial roadmaps that help protect, grow, and transfer wealth more efficiently. From insurance, as part of an estate strategy, to broader diversification, we help bring the pieces together. Book a quick review.

A tax refund can feel like “extra” money — but it can also be a powerful planning moment. Putting it toward the right goal (RRSP, TFSA, debt strategy, or a targeted savings plan) can help you build momentum. The best move depends on your priorities and your timeline.

A tax refund can feel like “extra” money — but it can also be a powerful planning moment. Putting it toward the right goal (RRSP, TFSA, debt strategy, or a targeted savings plan) can help you build momentum. The best move depends on your priorities and your timeline.

Your retirement plan should feel personal and unique to you and your goals. Sun Life One Plan can help bring your goals, investments and income strategy together into one clear financial roadmap, so you can see what’s possible and adjust as life changes. What would you like your retirement to look like? https://advisor.sunlife.ca/vitalis.financial.services/

#SunLifeOnePlan #RetirementPlanning

#SunLifeOnePlan #RetirementPlanning

Your retirement plan should feel personal and unique to you and your goals. Sun Life One Plan can help bring your goals, investments and income strategy together into one clear financial roadmap, so you can see what’s possible and adjust as life changes. What would you like your retirement to look like? https://advisor.sunlife.ca/vitalis.financial.services/

#SunLifeOnePlan #RetirementPlanning

#SunLifeOnePlan #RetirementPlanning

Your mortgage is likely one of your biggest financial commitments. What happens to it if something unexpected occurs? Mortgage protection insurance helps ensure your family can keep your home secure, no matter what life brings. Let's review your coverage and give you peace of mind. Reach out to discuss your options today.

https://advisor.sunlife.ca/vitalis.financial.services/

https://advisor.sunlife.ca/vitalis.financial.services/

Your mortgage is likely one of your biggest financial commitments. What happens to it if something unexpected occurs? Mortgage protection insurance helps ensure your family can keep your home secure, no matter what life brings. Let's review your coverage and give you peace of mind. Reach out to discuss your options today.

https://advisor.sunlife.ca/vitalis.financial.services/

https://advisor.sunlife.ca/vitalis.financial.services/

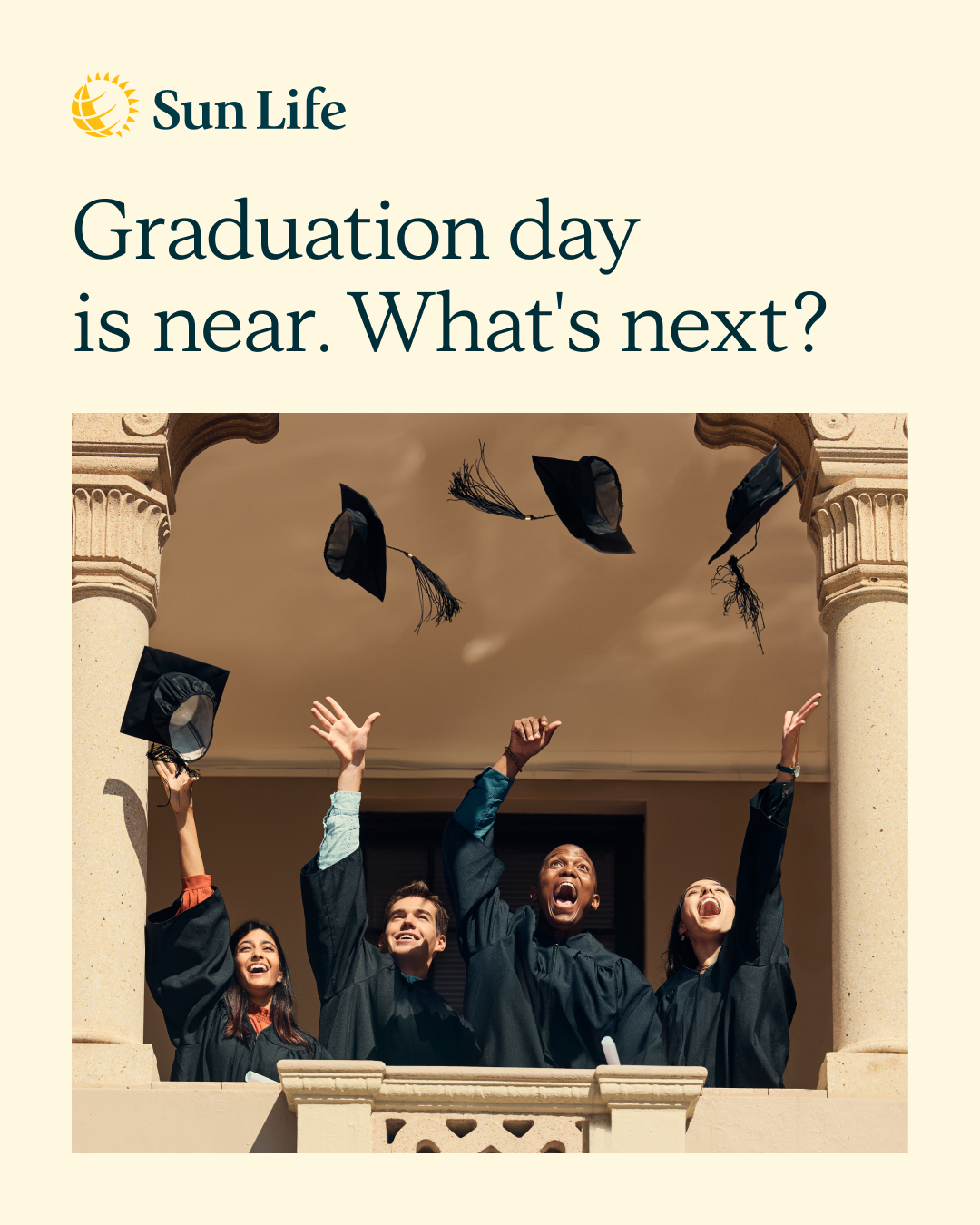

Congratulations on graduating! Now comes the next chapter, managing student debt while building your future. From repayment strategies to integrating loans into your financial roadmap, let's make sure you're set up for success. Whether it's buying a first home or saving for further education, we can help you navigate it all. Let's talk!

Congratulations on graduating! Now comes the next chapter, managing student debt while building your future. From repayment strategies to integrating loans into your financial roadmap, let's make sure you're set up for success. Whether it's buying a first home or saving for further education, we can help you navigate it all. Let's talk!

Taxes complete? Now is the perfect time to think bigger. Your tax refund is an opportunity to strengthen your financial foundation. Whether it's boosting RRSP contributions, maximizing investment strategies or planning for next year, let's help ensure every dollar works harder for you. Questions about how to best utilize your tax return? Let's chat!

https://advisor.sunlife.ca/vitalis.financial.services/

https://advisor.sunlife.ca/vitalis.financial.services/

Taxes complete? Now is the perfect time to think bigger. Your tax refund is an opportunity to strengthen your financial foundation. Whether it's boosting RRSP contributions, maximizing investment strategies or planning for next year, let's help ensure every dollar works harder for you. Questions about how to best utilize your tax return? Let's chat!

https://advisor.sunlife.ca/vitalis.financial.services/

https://advisor.sunlife.ca/vitalis.financial.services/

Thinking about retirement? Move from “a number” to a real plan. Income, timing, taxes and how you’ll use your savings all work better when they’re aligned. The sooner you explore your options, the more choices you may have later.

Thinking about retirement? Move from “a number” to a real plan. Income, timing, taxes and how you’ll use your savings all work better when they’re aligned. The sooner you explore your options, the more choices you may have later.

📈 Myth: Market ups and downs can derail even the best retirement plans.

Sun GIF Solutions Income Series offers a guaranteed income for life no matter what markets do. Keep in mind, extra withdrawals taken above the guaranteed income amount will decrease future income amounts.

Let’s talk about whether Sun Life GIFs are the right choice for your retirement.

Sun GIF Solutions Income Series offers a guaranteed income for life no matter what markets do. Keep in mind, extra withdrawals taken above the guaranteed income amount will decrease future income amounts.

Let’s talk about whether Sun Life GIFs are the right choice for your retirement.

📈 Myth: Market ups and downs can derail even the best retirement plans.

Sun GIF Solutions Income Series offers a guaranteed income for life no matter what markets do. Keep in mind, extra withdrawals taken above the guaranteed income amount will decrease future income amounts.

Let’s talk about whether Sun Life GIFs are the right choice for your retirement.

Sun GIF Solutions Income Series offers a guaranteed income for life no matter what markets do. Keep in mind, extra withdrawals taken above the guaranteed income amount will decrease future income amounts.

Let’s talk about whether Sun Life GIFs are the right choice for your retirement.

🔒 Myth: Money in a segregated fund is locked in.

Your money can be accessed at any time; however, withdrawals will impact the guarantees (maturity and death benefit) associated with the specific contract. Often guarantees are 75% or 100% of your initial investments or market value, whichever is higher.

Get in touch to discuss whether a segregated fund is the right choice for your investments!

Your money can be accessed at any time; however, withdrawals will impact the guarantees (maturity and death benefit) associated with the specific contract. Often guarantees are 75% or 100% of your initial investments or market value, whichever is higher.

Get in touch to discuss whether a segregated fund is the right choice for your investments!

🔒 Myth: Money in a segregated fund is locked in.

Your money can be accessed at any time; however, withdrawals will impact the guarantees (maturity and death benefit) associated with the specific contract. Often guarantees are 75% or 100% of your initial investments or market value, whichever is higher.

Get in touch to discuss whether a segregated fund is the right choice for your investments!

Your money can be accessed at any time; however, withdrawals will impact the guarantees (maturity and death benefit) associated with the specific contract. Often guarantees are 75% or 100% of your initial investments or market value, whichever is higher.

Get in touch to discuss whether a segregated fund is the right choice for your investments!

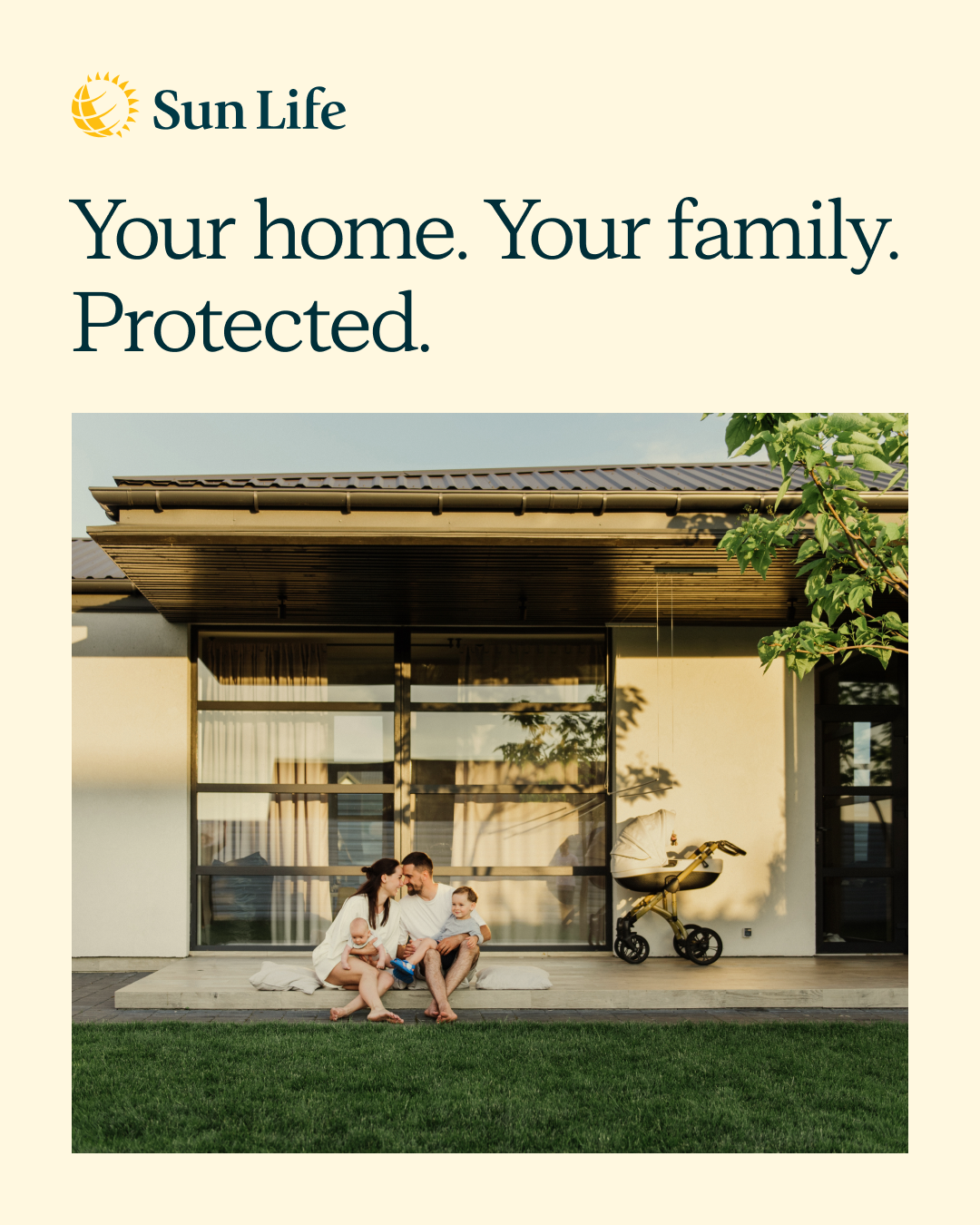

You're building your future – let's help make sure it's protected.

Whether you're planning for your growing family or thinking about what you'll leave behind, our current offers make comprehensive coverage more affordable. Get 10% off permanent insurance when bundled with term insurance, and cash back on critical illness protection. Real savings for real life. Let’s chat! Offer ends July 31.

Whether you're planning for your growing family or thinking about what you'll leave behind, our current offers make comprehensive coverage more affordable. Get 10% off permanent insurance when bundled with term insurance, and cash back on critical illness protection. Real savings for real life. Let’s chat! Offer ends July 31.

You're building your future – let's help make sure it's protected.

Whether you're planning for your growing family or thinking about what you'll leave behind, our current offers make comprehensive coverage more affordable. Get 10% off permanent insurance when bundled with term insurance, and cash back on critical illness protection. Real savings for real life. Let’s chat! Offer ends July 31.

Whether you're planning for your growing family or thinking about what you'll leave behind, our current offers make comprehensive coverage more affordable. Get 10% off permanent insurance when bundled with term insurance, and cash back on critical illness protection. Real savings for real life. Let’s chat! Offer ends July 31.

Have questions?

Here to help answer your questions, provide clarity about products and get you started on the road to achieving your goals.

We are contracted with Sun Life Financial Distributors (Canada) Inc., a member of the Sun Life group of companies. Mutual funds distributed by Sun Life Financial Investment Services (Canada) Inc.