Stay informed

Stay informed with what’s going on. Browse posts that might be helpful to you or check out an event happening in your area. Come back regularly as this page is kept up-to-date with a lot of relevant information.

Health events can happen without warning — and the costs aren’t always medical. Critical illness insurance can provide financial support during a serious diagnosis, helping with time off work, travel for care, or everyday expenses so you can focus on recovery. Want to explore if it fits your plan? https://advisor.sunlife.ca/wild.illsley

Health events can happen without warning — and the costs aren’t always medical. Critical illness insurance can provide financial support during a serious diagnosis, helping with time off work, travel for care, or everyday expenses so you can focus on recovery. Want to explore if it fits your plan? https://advisor.sunlife.ca/wild.illsley

Transferring wealth isn’t just about assets — it involves values, intentions and clarity.

A well-structured roadmap can help ensure your wealth supports the people and causes that matter most to you, across generations.

Together, let’s help shape a legacy that reflects your vision using Sun Life One Plan. Get in touch to get started. https://advisor.sunlife.ca/wild.illsley

#SunLifeOnePlan #SunLife

A well-structured roadmap can help ensure your wealth supports the people and causes that matter most to you, across generations.

Together, let’s help shape a legacy that reflects your vision using Sun Life One Plan. Get in touch to get started. https://advisor.sunlife.ca/wild.illsley

#SunLifeOnePlan #SunLife

Transferring wealth isn’t just about assets — it involves values, intentions and clarity.

A well-structured roadmap can help ensure your wealth supports the people and causes that matter most to you, across generations.

Together, let’s help shape a legacy that reflects your vision using Sun Life One Plan. Get in touch to get started. https://advisor.sunlife.ca/wild.illsley

#SunLifeOnePlan #SunLife

A well-structured roadmap can help ensure your wealth supports the people and causes that matter most to you, across generations.

Together, let’s help shape a legacy that reflects your vision using Sun Life One Plan. Get in touch to get started. https://advisor.sunlife.ca/wild.illsley

#SunLifeOnePlan #SunLife

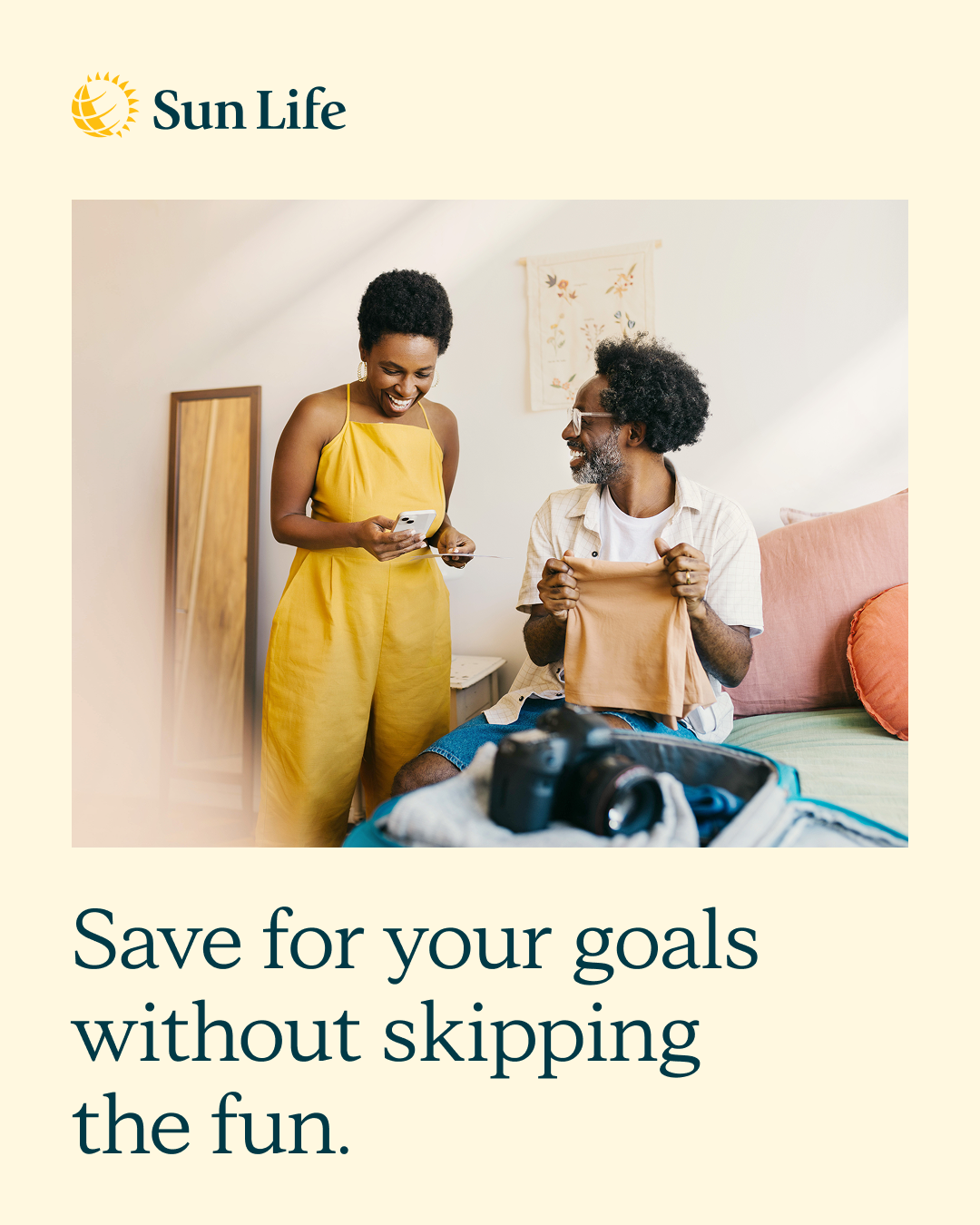

Saving for your goals shouldn’t mean skipping the fun. Whether you’re planning travel, a wedding, a big experience or your next “chapter,” the right strategy can help you set aside cash intentionally while still staying on track. Let's transform your priorities into a financial roadmap you can commit to. https://advisor.sunlife.ca/wild.illsley

Saving for your goals shouldn’t mean skipping the fun. Whether you’re planning travel, a wedding, a big experience or your next “chapter,” the right strategy can help you set aside cash intentionally while still staying on track. Let's transform your priorities into a financial roadmap you can commit to. https://advisor.sunlife.ca/wild.illsley

Greater wealth can bring greater complexity. From tax-aware approaches to estate considerations, having a thoughtful plan in place can help you protect and preserve what matters most — today and for the future. Let’s help simplify your next steps with a personalized roadmap. https://advisor.sunlife.ca/wild.illsley

Greater wealth can bring greater complexity. From tax-aware approaches to estate considerations, having a thoughtful plan in place can help you protect and preserve what matters most — today and for the future. Let’s help simplify your next steps with a personalized roadmap. https://advisor.sunlife.ca/wild.illsley

When your money is spread across different accounts, having one clear plan can help it work better for you over time. If you’re managing milestone goals like a home, family, retirement, or what you want to leave behind, it helps when everything connects. Let’s put a strategy together that helps support what you want next. https://advisor.sunlife.ca/wild.illsley

When your money is spread across different accounts, having one clear plan can help it work better for you over time. If you’re managing milestone goals like a home, family, retirement, or what you want to leave behind, it helps when everything connects. Let’s put a strategy together that helps support what you want next. https://advisor.sunlife.ca/wild.illsley

Ease into retirement with Sun Life One Plan

Your retirement plan should feel unique and tailored to you. Sun Life One Plan can help bring your goals, investments and income strategy together so you can see what’s possible. Get in touch to start planning your dream retirement. https://advisor.sunlife.ca/wild.illsley

#SunLifeOnePlan #RetirementPlanning

#SunLifeOnePlan #RetirementPlanning

Watch video

From coast to coast, today is about connection, community and celebration. 🍁

Here’s to enjoying the moment and continuing to build a strong financial future. #HappyCanadaDay #CanadaDay

Here’s to enjoying the moment and continuing to build a strong financial future. #HappyCanadaDay #CanadaDay

From coast to coast, today is about connection, community and celebration. 🍁

Here’s to enjoying the moment and continuing to build a strong financial future. #HappyCanadaDay #CanadaDay

Here’s to enjoying the moment and continuing to build a strong financial future. #HappyCanadaDay #CanadaDay

Unexpected events don’t send calendar invites. A back-up plan can help your business stay steady if a key person becomes suddenly unavailable, or revenue unexpectedly dips. Let’s pressure-test “what ifs” for your business and build a strategy that helps protect both your company and your personal finances. https://advisor.sunlife.ca/wild.illsley

Unexpected events don’t send calendar invites. A back-up plan can help your business stay steady if a key person becomes suddenly unavailable, or revenue unexpectedly dips. Let’s pressure-test “what ifs” for your business and build a strategy that helps protect both your company and your personal finances. https://advisor.sunlife.ca/wild.illsley

From gifts to travel, wedding season can add up quickly. A little foresight can help you celebrate the big moments without putting your financial goals on hold. If you’re looking to balance it all this summer, let’s talk — so you can enjoy every celebration with confidence. https://advisor.sunlife.ca/wild.illsley

From gifts to travel, wedding season can add up quickly. A little foresight can help you celebrate the big moments without putting your financial goals on hold. If you’re looking to balance it all this summer, let’s talk — so you can enjoy every celebration with confidence. https://advisor.sunlife.ca/wild.illsley

Whether it’s your first place or a fresh move, new beginnings come with new opportunities.

As things change, it can help to make sure your financial priorities still reflect where you are today. If you’d like to talk it through, I’m here to help.

As things change, it can help to make sure your financial priorities still reflect where you are today. If you’d like to talk it through, I’m here to help.

Whether it’s your first place or a fresh move, new beginnings come with new opportunities.

As things change, it can help to make sure your financial priorities still reflect where you are today. If you’d like to talk it through, I’m here to help.

As things change, it can help to make sure your financial priorities still reflect where you are today. If you’d like to talk it through, I’m here to help.

Disability can impact more than just your income — it can affect your financial priorities all at once. The right coverage can help create breathing room if you’re unable to work due to illness or injury. If your paycheque fuels your plans, they may be worth protecting. Get in touch to talk about your options. https://advisor.sunlife.ca/wild.illsley

Disability can impact more than just your income — it can affect your financial priorities all at once. The right coverage can help create breathing room if you’re unable to work due to illness or injury. If your paycheque fuels your plans, they may be worth protecting. Get in touch to talk about your options. https://advisor.sunlife.ca/wild.illsley

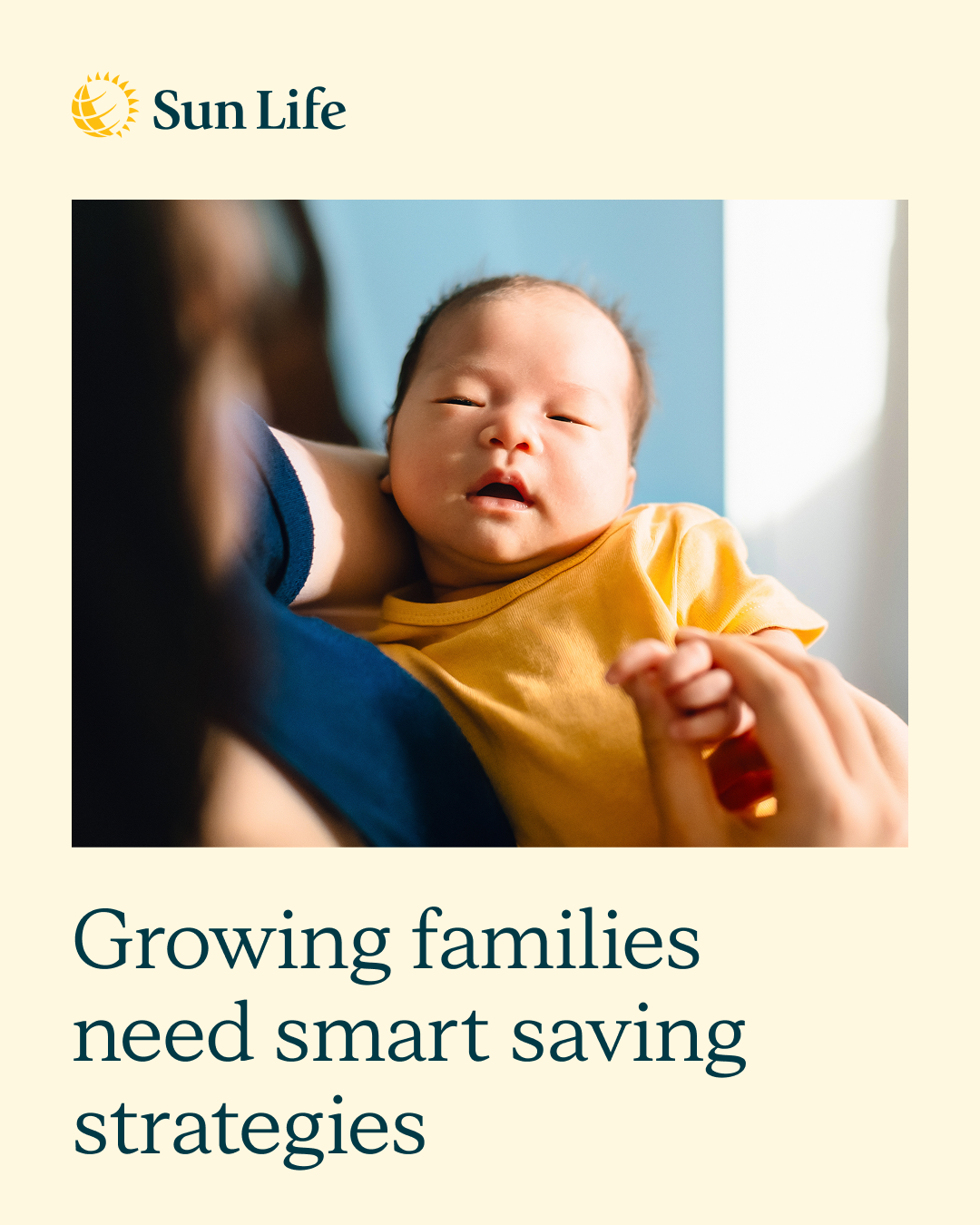

A growing family is exciting — and it changes everything from monthly cash flow to longer-term goals. Childcare, activities, housing, education… it adds up fast. A realistic plan can help you balance today’s costs while still making progress on what matters most.

A growing family is exciting — and it changes everything from monthly cash flow to longer-term goals. Childcare, activities, housing, education… it adds up fast. A realistic plan can help you balance today’s costs while still making progress on what matters most.

Prediabetes: 3 lifestyle changes lower chronic disease risk by 21%

A new study has found that, in a group of adults with prediabetes, lifestyle modifications were more effective at preventing multiple chronic conditions, including type 2 diabetes, than metformin or placebo.

https://advisor.sunlife.ca/wild.illsley

https://advisor.sunlife.ca/wild.illsley

As wealth grows, so does complexity. Smart financial strategies look beyond traditional investing to financial roadmaps that help protect, grow, and transfer wealth more efficiently. From insurance, as part of an estate strategy, to broader diversification, we help bring the pieces together. Book a quick review.

As wealth grows, so does complexity. Smart financial strategies look beyond traditional investing to financial roadmaps that help protect, grow, and transfer wealth more efficiently. From insurance, as part of an estate strategy, to broader diversification, we help bring the pieces together. Book a quick review.

Weekly Exercise Goals Should Be Higher to Prevent Heart Attack, Stroke

Researchers say current aerobic exercise recommendations may not be sufficient to reduce cardiovascular risk.https://advisor.sunlife.ca/wild.illsley

A tax refund can feel like “extra” money — but it can also be a powerful planning moment. Putting it toward the right goal (RRSP, TFSA, debt strategy, or a targeted savings plan) can help you build momentum. The best move depends on your priorities — and your timeline. Let’s chat about your goals.

A tax refund can feel like “extra” money — but it can also be a powerful planning moment. Putting it toward the right goal (RRSP, TFSA, debt strategy, or a targeted savings plan) can help you build momentum. The best move depends on your priorities — and your timeline. Let’s chat about your goals.

Happy Father's Day to all the dads and father figures who guide, support and inspire us! 👨👦💙

Whether you're a father, stepfather, grandfather, mentor or positive role model — today we celebrate YOU and the impact you make. Thank you!

Whether you're a father, stepfather, grandfather, mentor or positive role model — today we celebrate YOU and the impact you make. Thank you!

Happy Father's Day to all the dads and father figures who guide, support and inspire us! 👨👦💙

Whether you're a father, stepfather, grandfather, mentor or positive role model — today we celebrate YOU and the impact you make. Thank you!

Whether you're a father, stepfather, grandfather, mentor or positive role model — today we celebrate YOU and the impact you make. Thank you!

Your mortgage is likely one of your biggest financial commitments. What happens to it if something unexpected occurs? Mortgage protection solutions can help support your family’s ability to keep your home secure, no matter what life brings. Let's review your coverage for peace of mind. Reach out to discuss your options today. https://advisor.sunlife.ca/wild.illsley

Watch video

Your retirement plan should feel personal — not generic. Sun Life One Plan can help bring your goals, investments and income strategy together into one clear financial roadmap, so you can see what’s possible and adjust as life changes. What would you like your retirement to look like? https://advisor.sunlife.ca/wild.illsley

#SunLifeOnePlan #RetirementPlanning

#SunLifeOnePlan #RetirementPlanning

Your retirement plan should feel personal — not generic. Sun Life One Plan can help bring your goals, investments and income strategy together into one clear financial roadmap, so you can see what’s possible and adjust as life changes. What would you like your retirement to look like? https://advisor.sunlife.ca/wild.illsley

#SunLifeOnePlan #RetirementPlanning

#SunLifeOnePlan #RetirementPlanning

A business built for the long term needs more than cash flow. Clear routines, healthy boundaries and the right support helps teams stay engaged and productive. Let’s chat about how we can work together to support your staff and business goals.

A business built for the long term needs more than cash flow. Clear routines, healthy boundaries and the right support helps teams stay engaged and productive. Let’s chat about how we can work together to support your staff and business goals.

Have questions?

Here to help answer your questions, provide clarity about products and get you started on the road to achieving your goals.