Stay Informed

Brock is active on social media - follow him on Facebook, Instagram and LinkedIn.

Did you get a tax refund? This is your chance to boost your retirement readiness. Strategic RRSP contributions or tax-efficient withdrawals can help maximize your refund's impact on your retirement roadmap. Let's make every dollar count. https://advisor.sunlife.ca/brock.vale/

Did you get a tax refund? This is your chance to boost your retirement readiness. Strategic RRSP contributions or tax-efficient withdrawals can help maximize your refund's impact on your retirement roadmap. Let's make every dollar count. https://advisor.sunlife.ca/brock.vale/

Financial stress doesn’t go away by ignoring it—it goes away by planning for it. 🛑

I’ve seen a lot of people lately who are hesitant to reach out because they're embarrassed about debt. Don't be. My office is a judgment-free zone where we focus on the solution, not the past.

If you're ready to trade that stress for a strategy, let's get to work. 🤝

I’ve seen a lot of people lately who are hesitant to reach out because they're embarrassed about debt. Don't be. My office is a judgment-free zone where we focus on the solution, not the past.

If you're ready to trade that stress for a strategy, let's get to work. 🤝

Do you know anyone saving up to buy their first home?!

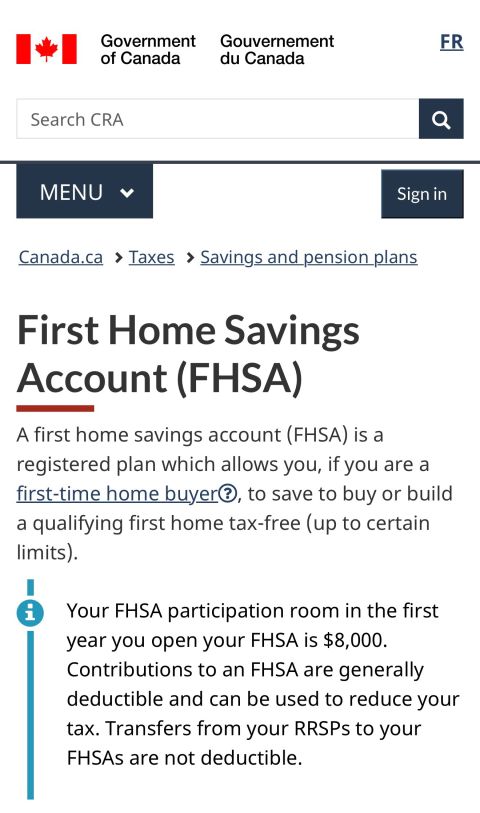

The First Home Savings Account (FHSA) may the best registered account ever created for young Canadians!

1. Contributions are tax-deductible (similar to an RRSP), reducing your taxable income in the year contributed.

2. Investment growth is tax-free.

3. Qualifying withdrawals (for a first home) are tax-free (similar to a TFSA), including both contributions and earnings.

4. You can transfer funds from an RRSP to an FHSA (up to contribution room limits).

5. If you don't use your FHSA to buy a home you can roll the entire balance over to your RRSP (or RRIF) giving you a larger RRSP (or RRIF).

Annual contribution limit: $8,000 per year

Lifetime contribution limit: $40,000

Unused room carries forward (up to $8,000 max carry-forward per year)

Is tax-free if used to buy or build a home. No repayment required (unlike the RRSP Home Buyers' Plan).

Note:

a. You and your partner must never have owned a home in the current year or past 4 calendar years

b. The FHSA reaches the end of its participation period after 15 years or by age 71, whichever comes first

If you are a young Canadian adult who doesn’t own a primary residence the FHSA might be the best registered account out there!

The First Home Savings Account (FHSA) may the best registered account ever created for young Canadians!

1. Contributions are tax-deductible (similar to an RRSP), reducing your taxable income in the year contributed.

2. Investment growth is tax-free.

3. Qualifying withdrawals (for a first home) are tax-free (similar to a TFSA), including both contributions and earnings.

4. You can transfer funds from an RRSP to an FHSA (up to contribution room limits).

5. If you don't use your FHSA to buy a home you can roll the entire balance over to your RRSP (or RRIF) giving you a larger RRSP (or RRIF).

Annual contribution limit: $8,000 per year

Lifetime contribution limit: $40,000

Unused room carries forward (up to $8,000 max carry-forward per year)

Is tax-free if used to buy or build a home. No repayment required (unlike the RRSP Home Buyers' Plan).

Note:

a. You and your partner must never have owned a home in the current year or past 4 calendar years

b. The FHSA reaches the end of its participation period after 15 years or by age 71, whichever comes first

If you are a young Canadian adult who doesn’t own a primary residence the FHSA might be the best registered account out there!

Do you know anyone saving up to buy their first home?!

The First Home Savings Account (FHSA) may the best registered account ever created for young Canadians!

1. Contributions are tax-deductible (similar to an RRSP), reducing your taxable income in the year contributed.

2. Investment growth is tax-free.

3. Qualifying withdrawals (for a first home) are tax-free (similar to a TFSA), including both contributions and earnings.

4. You can transfer funds from an RRSP to an FHSA (up to contribution room limits).

5. If you don't use your FHSA to buy a home you can roll the entire balance over to your RRSP (or RRIF) giving you a larger RRSP (or RRIF).

Annual contribution limit: $8,000 per year

Lifetime contribution limit: $40,000

Unused room carries forward (up to $8,000 max carry-forward per year)

Is tax-free if used to buy or build a home. No repayment required (unlike the RRSP Home Buyers' Plan).

Note:

a. You and your partner must never have owned a home in the current year or past 4 calendar years

b. The FHSA reaches the end of its participation period after 15 years or by age 71, whichever comes first

If you are a young Canadian adult who doesn’t own a primary residence the FHSA might be the best registered account out there!

The First Home Savings Account (FHSA) may the best registered account ever created for young Canadians!

1. Contributions are tax-deductible (similar to an RRSP), reducing your taxable income in the year contributed.

2. Investment growth is tax-free.

3. Qualifying withdrawals (for a first home) are tax-free (similar to a TFSA), including both contributions and earnings.

4. You can transfer funds from an RRSP to an FHSA (up to contribution room limits).

5. If you don't use your FHSA to buy a home you can roll the entire balance over to your RRSP (or RRIF) giving you a larger RRSP (or RRIF).

Annual contribution limit: $8,000 per year

Lifetime contribution limit: $40,000

Unused room carries forward (up to $8,000 max carry-forward per year)

Is tax-free if used to buy or build a home. No repayment required (unlike the RRSP Home Buyers' Plan).

Note:

a. You and your partner must never have owned a home in the current year or past 4 calendar years

b. The FHSA reaches the end of its participation period after 15 years or by age 71, whichever comes first

If you are a young Canadian adult who doesn’t own a primary residence the FHSA might be the best registered account out there!

Prediction time… January of 2027, most Canadians will see a much bigger number on their investment statements.

This isn’t a stock market prediction.

It’s fee disclosure. So why is this number going to be bigger?

Regulators are rolling out mandatory total fee disclosure in real dollars, total percentages and as an aggregated total cost.

The prior iteration of this only required disclosure of dealer and advisor compensation.

Now, clients will see the compensation paid to your advisor, the investment fees, trading fees and administrative fees.

For those in A series mutual funds don’t be surprised if you are paying close to double what your current statements show.

In an A series portfolio of $500k, that charges 2.2%, this year you may only see the advisor / dealer compensation which could be anywhere from $4-5k.

In 2027, that number will balloon to nearly $11k!

Be vigilant, ask questions, and if advisors tell you that you don’t pay fees on your portfolios, ask someone else to review it.

I am spending 2026 making sure that clients are aware of their fees and costs. You should know what you pay, where it goes, and what you are getting.

Advisors that hide these fees are selling their clients short. You and I, both want your account values to go up. Not all fees are "fees", some of it is a cost of professional advice, market research by advisors and fund managers, and some of it is a cost of the product.

However, not knowing what you pay or what you get is disappointing.

If you would like my help looking over your current investment portfolio's fees, I am here to help.

Brock Vale

Sun Life, Advisor

613-243-0015

This isn’t a stock market prediction.

It’s fee disclosure. So why is this number going to be bigger?

Regulators are rolling out mandatory total fee disclosure in real dollars, total percentages and as an aggregated total cost.

The prior iteration of this only required disclosure of dealer and advisor compensation.

Now, clients will see the compensation paid to your advisor, the investment fees, trading fees and administrative fees.

For those in A series mutual funds don’t be surprised if you are paying close to double what your current statements show.

In an A series portfolio of $500k, that charges 2.2%, this year you may only see the advisor / dealer compensation which could be anywhere from $4-5k.

In 2027, that number will balloon to nearly $11k!

Be vigilant, ask questions, and if advisors tell you that you don’t pay fees on your portfolios, ask someone else to review it.

I am spending 2026 making sure that clients are aware of their fees and costs. You should know what you pay, where it goes, and what you are getting.

Advisors that hide these fees are selling their clients short. You and I, both want your account values to go up. Not all fees are "fees", some of it is a cost of professional advice, market research by advisors and fund managers, and some of it is a cost of the product.

However, not knowing what you pay or what you get is disappointing.

If you would like my help looking over your current investment portfolio's fees, I am here to help.

Brock Vale

Sun Life, Advisor

613-243-0015

Watching the markets drop 500+ points in a single session (like we saw Friday) is a massive gut check. It’s easy to be a long-term investor when everything is green, but the red days are where the real work happens.

Whether this volatility lasts three weeks or three years, your plan shouldn't change—but your structure might need to.

If you're staring at your accounts wondering if you’re actually diversified enough to handle this, let’s talk. A properly structured portfolio isn't built to avoid the storm; it’s built to weather it without sinking your long-term goals.

Don't wait for the bottom to find out if your plan works. Send me a message and let's do a quick "stress test" on your current setup. 🛠️

Whether this volatility lasts three weeks or three years, your plan shouldn't change—but your structure might need to.

If you're staring at your accounts wondering if you’re actually diversified enough to handle this, let’s talk. A properly structured portfolio isn't built to avoid the storm; it’s built to weather it without sinking your long-term goals.

Don't wait for the bottom to find out if your plan works. Send me a message and let's do a quick "stress test" on your current setup. 🛠️

Is Your Tax Refund a "Bonus" or a "Breakthrough"? The $100k Difference.

Millions of tax refunds are landing in bank accounts these days. While the average Canadian refund is approximately $2,300, how you treat that money in 2026 will determine your financial trajectory for the next decade.

The Data: Two Paths for the Average $2,300 Refund

Path A: The "One-Time Win"

You spend the $2,300 on a vacation or retail.

Result: Great memories, but a $0 balance in your investment account by next year.

Path B: The "Legacy Builder" (Reinvested)

You put that $2,300 into a diversified investment portfolio (especially into an RRSP or TFSA account) and repeat this for just 15 years.

The Growth: At an average 7% annual return, that single annual habit could grow to over $60,000.

The 30-Year Impact: If you start this habit in your 30s, by retirement, those "refunds" alone could be worth over $220,000 tax-free.

Why 2026 is the Year to Start:

With the recent changes to capital gains and the increasing cost of living in Ontario, "passive saving" isn't enough anymore. You need your money to work as hard as you do.

3 Strategic Ways to Use Your 2026 Refund:

The TFSA "Power-Up": Maximize your tax-free growth to shield your gains from the 2026 tax environment.

The RRSP Loop: Reinvest your refund back into your RRSP to create a second tax deduction for 2027. This is how the wealthy build momentum.

The FHSA Route: If you’re saving for your first home, your refund is tax-free going in and tax-free coming out. It’s a double win. Plus, you'll work towards a tax deduction for 2027.

The Bottom Line:

An average refund invested today isn't just $2,300—it’s the foundation of a six-figure legacy.

Ready to see what your specific refund could look like in 10 years? Let’s run the numbers together.

📍 Brock Vale | Sun Life

📞 613-243-0015

Millions of tax refunds are landing in bank accounts these days. While the average Canadian refund is approximately $2,300, how you treat that money in 2026 will determine your financial trajectory for the next decade.

The Data: Two Paths for the Average $2,300 Refund

Path A: The "One-Time Win"

You spend the $2,300 on a vacation or retail.

Result: Great memories, but a $0 balance in your investment account by next year.

Path B: The "Legacy Builder" (Reinvested)

You put that $2,300 into a diversified investment portfolio (especially into an RRSP or TFSA account) and repeat this for just 15 years.

The Growth: At an average 7% annual return, that single annual habit could grow to over $60,000.

The 30-Year Impact: If you start this habit in your 30s, by retirement, those "refunds" alone could be worth over $220,000 tax-free.

Why 2026 is the Year to Start:

With the recent changes to capital gains and the increasing cost of living in Ontario, "passive saving" isn't enough anymore. You need your money to work as hard as you do.

3 Strategic Ways to Use Your 2026 Refund:

The TFSA "Power-Up": Maximize your tax-free growth to shield your gains from the 2026 tax environment.

The RRSP Loop: Reinvest your refund back into your RRSP to create a second tax deduction for 2027. This is how the wealthy build momentum.

The FHSA Route: If you’re saving for your first home, your refund is tax-free going in and tax-free coming out. It’s a double win. Plus, you'll work towards a tax deduction for 2027.

The Bottom Line:

An average refund invested today isn't just $2,300—it’s the foundation of a six-figure legacy.

Ready to see what your specific refund could look like in 10 years? Let’s run the numbers together.

📍 Brock Vale | Sun Life

📞 613-243-0015

Is Your Tax Refund a "Bonus" or a "Breakthrough"? The $100k Difference.

Millions of tax refunds are landing in bank accounts these days. While the average Canadian refund is approximately $2,300, how you treat that money in 2026 will determine your financial trajectory for the next decade.

The Data: Two Paths for the Average $2,300 Refund

Path A: The "One-Time Win"

You spend the $2,300 on a vacation or retail.

Result: Great memories, but a $0 balance in your investment account by next year.

Path B: The "Legacy Builder" (Reinvested)

You put that $2,300 into a diversified investment portfolio (especially into an RRSP or TFSA account) and repeat this for just 15 years.

The Growth: At an average 7% annual return, that single annual habit could grow to over $60,000.

The 30-Year Impact: If you start this habit in your 30s, by retirement, those "refunds" alone could be worth over $220,000 tax-free.

Why 2026 is the Year to Start:

With the recent changes to capital gains and the increasing cost of living in Ontario, "passive saving" isn't enough anymore. You need your money to work as hard as you do.

3 Strategic Ways to Use Your 2026 Refund:

The TFSA "Power-Up": Maximize your tax-free growth to shield your gains from the 2026 tax environment.

The RRSP Loop: Reinvest your refund back into your RRSP to create a second tax deduction for 2027. This is how the wealthy build momentum.

The FHSA Route: If you’re saving for your first home, your refund is tax-free going in and tax-free coming out. It’s a double win. Plus, you'll work towards a tax deduction for 2027.

The Bottom Line:

An average refund invested today isn't just $2,300—it’s the foundation of a six-figure legacy.

Ready to see what your specific refund could look like in 10 years? Let’s run the numbers together.

📍 Brock Vale | Sun Life

📞 613-243-0015

Millions of tax refunds are landing in bank accounts these days. While the average Canadian refund is approximately $2,300, how you treat that money in 2026 will determine your financial trajectory for the next decade.

The Data: Two Paths for the Average $2,300 Refund

Path A: The "One-Time Win"

You spend the $2,300 on a vacation or retail.

Result: Great memories, but a $0 balance in your investment account by next year.

Path B: The "Legacy Builder" (Reinvested)

You put that $2,300 into a diversified investment portfolio (especially into an RRSP or TFSA account) and repeat this for just 15 years.

The Growth: At an average 7% annual return, that single annual habit could grow to over $60,000.

The 30-Year Impact: If you start this habit in your 30s, by retirement, those "refunds" alone could be worth over $220,000 tax-free.

Why 2026 is the Year to Start:

With the recent changes to capital gains and the increasing cost of living in Ontario, "passive saving" isn't enough anymore. You need your money to work as hard as you do.

3 Strategic Ways to Use Your 2026 Refund:

The TFSA "Power-Up": Maximize your tax-free growth to shield your gains from the 2026 tax environment.

The RRSP Loop: Reinvest your refund back into your RRSP to create a second tax deduction for 2027. This is how the wealthy build momentum.

The FHSA Route: If you’re saving for your first home, your refund is tax-free going in and tax-free coming out. It’s a double win. Plus, you'll work towards a tax deduction for 2027.

The Bottom Line:

An average refund invested today isn't just $2,300—it’s the foundation of a six-figure legacy.

Ready to see what your specific refund could look like in 10 years? Let’s run the numbers together.

📍 Brock Vale | Sun Life

📞 613-243-0015

Most people spend more time researching their March Madness bracket than their workplace retirement investments!

When those HR forms arrive, guessing based on cool names or last year's winners is a common mistake.

In a tournament, a bad pick ruins a pool—in your RRSP, it impacts your future.

If you’re looking for a second set of eyes on your available options, let's connect.

When those HR forms arrive, guessing based on cool names or last year's winners is a common mistake.

In a tournament, a bad pick ruins a pool—in your RRSP, it impacts your future.

If you’re looking for a second set of eyes on your available options, let's connect.

Most people spend more time researching their March Madness bracket than their workplace retirement investments!

When those HR forms arrive, guessing based on cool names or last year's winners is a common mistake.

In a tournament, a bad pick ruins a pool—in your RRSP, it impacts your future.

If you’re looking for a second set of eyes on your available options, let's connect.

When those HR forms arrive, guessing based on cool names or last year's winners is a common mistake.

In a tournament, a bad pick ruins a pool—in your RRSP, it impacts your future.

If you’re looking for a second set of eyes on your available options, let's connect.

Don't just spend your refund—multiply it.

Most people treat their tax refund as "found money".

That tax refund could be the foundation of your family's financial plan.

By choosing to invest instead of spend, you are changing your mindset for good!

Most people treat their tax refund as "found money".

That tax refund could be the foundation of your family's financial plan.

By choosing to invest instead of spend, you are changing your mindset for good!

Don't just spend your refund—multiply it.

Most people treat their tax refund as "found money".

That tax refund could be the foundation of your family's financial plan.

By choosing to invest instead of spend, you are changing your mindset for good!

Most people treat their tax refund as "found money".

That tax refund could be the foundation of your family's financial plan.

By choosing to invest instead of spend, you are changing your mindset for good!

Retirement isn’t a number — it’s a roadmap. We’ll outline how your savings can become a reliable source of income. Together, let's build your withdrawal strategy.

#RetirementStrategy #Retirement #SunLife

#RetirementStrategy #Retirement #SunLife

Retirement isn’t a number — it’s a roadmap. We’ll outline how your savings can become a reliable source of income. Together, let's build your withdrawal strategy.

#RetirementStrategy #Retirement #SunLife

#RetirementStrategy #Retirement #SunLife

Do you find that your money sometimes seems to disappear after pay day?

If so, you need a plan for your money.

Here are the top, actionable ways to use your tax return:

Pay Down High-Interest Debt: Prioritize credit cards, personal loans, or lines of credit to save on interest payments.

Build an Emergency Fund: If you do not have one, use this cash to start a savings account covering 3-6 months of living expenses.

Invest for the Future (RRSP/TFSA): Contribute to a TFSA for tax-free growth or an RRSP to reduce future taxable income.

Make an Extra Mortgage Payment: If permitted, applying the refund to your principal can save significant interest over time.

Contribute to an RESP: Invest in a Registered Education Savings Plan to take advantage of government grants for your children’s education.

Invest in Yourself: Use the money to take courses, learn new skills, or upgrade your qualifications for career advancement.

Repair or Improve Your Home: Address necessary home repairs or maintenance to avoid costlier issues later.

Do you have your tax return planned?

If not, there is a high chance it disappears to extra expenses.

If so, you need a plan for your money.

Here are the top, actionable ways to use your tax return:

Pay Down High-Interest Debt: Prioritize credit cards, personal loans, or lines of credit to save on interest payments.

Build an Emergency Fund: If you do not have one, use this cash to start a savings account covering 3-6 months of living expenses.

Invest for the Future (RRSP/TFSA): Contribute to a TFSA for tax-free growth or an RRSP to reduce future taxable income.

Make an Extra Mortgage Payment: If permitted, applying the refund to your principal can save significant interest over time.

Contribute to an RESP: Invest in a Registered Education Savings Plan to take advantage of government grants for your children’s education.

Invest in Yourself: Use the money to take courses, learn new skills, or upgrade your qualifications for career advancement.

Repair or Improve Your Home: Address necessary home repairs or maintenance to avoid costlier issues later.

Do you have your tax return planned?

If not, there is a high chance it disappears to extra expenses.

Working from home is great, and I am more productive than being in the office and making the commute.

However, every time I see my kitty laying on his back for belly rubs, I will be away from my desk.

However, every time I see my kitty laying on his back for belly rubs, I will be away from my desk.

Working from home is great, and I am more productive than being in the office and making the commute.

However, every time I see my kitty laying on his back for belly rubs, I will be away from my desk.

However, every time I see my kitty laying on his back for belly rubs, I will be away from my desk.

The Smartest Insurance Policy for Estate Planning (That You’ve Probably Never Heard Of)

When we talk about estate planning in 2026, one of the biggest hurdles isn't the inheritance itself—it’s the tax bill that comes with it.

If you own a home, a cottage, or a significant RRIF, your heirs could be looking at a major tax hit from the CRA.

The Solution? Joint Last-to-Die (JLT) Life Insurance.

What is it?

Unlike traditional life insurance that pays out when one person passes away, a JLT policy covers two people (usually spouses) and pays out only after the second person passes.

Why is this the "Gold Standard" for Estate Planning?

Cost-Efficient: Because the payout is deferred until the second death, the premiums are typically significantly lower than two individual policies.

Perfect Timing: In Canada, most taxes on an estate are deferred until the second spouse passes. A JLT policy triggers a tax-free payout at the exact moment the CRA bill arrives.

Liquidity: It provides the cash needed to pay probate fees and capital gains, so your kids don't have to sell the family home or the cottage just to pay the taxes.

The Bottom Line:

It’s not about the payout for you; it’s about the legacy for them. It ensures that 100% of what you built stays with your family.

Looking to see how the math works for your specific situation ? Let’s run the numbers.

📍 Brock Vale | Sun Life

📞 613-243-0015

When we talk about estate planning in 2026, one of the biggest hurdles isn't the inheritance itself—it’s the tax bill that comes with it.

If you own a home, a cottage, or a significant RRIF, your heirs could be looking at a major tax hit from the CRA.

The Solution? Joint Last-to-Die (JLT) Life Insurance.

What is it?

Unlike traditional life insurance that pays out when one person passes away, a JLT policy covers two people (usually spouses) and pays out only after the second person passes.

Why is this the "Gold Standard" for Estate Planning?

Cost-Efficient: Because the payout is deferred until the second death, the premiums are typically significantly lower than two individual policies.

Perfect Timing: In Canada, most taxes on an estate are deferred until the second spouse passes. A JLT policy triggers a tax-free payout at the exact moment the CRA bill arrives.

Liquidity: It provides the cash needed to pay probate fees and capital gains, so your kids don't have to sell the family home or the cottage just to pay the taxes.

The Bottom Line:

It’s not about the payout for you; it’s about the legacy for them. It ensures that 100% of what you built stays with your family.

Looking to see how the math works for your specific situation ? Let’s run the numbers.

📍 Brock Vale | Sun Life

📞 613-243-0015

The Smartest Insurance Policy for Estate Planning (That You’ve Probably Never Heard Of)

When we talk about estate planning in 2026, one of the biggest hurdles isn't the inheritance itself—it’s the tax bill that comes with it.

If you own a home, a cottage, or a significant RRIF, your heirs could be looking at a major tax hit from the CRA.

The Solution? Joint Last-to-Die (JLT) Life Insurance.

What is it?

Unlike traditional life insurance that pays out when one person passes away, a JLT policy covers two people (usually spouses) and pays out only after the second person passes.

Why is this the "Gold Standard" for Estate Planning?

Cost-Efficient: Because the payout is deferred until the second death, the premiums are typically significantly lower than two individual policies.

Perfect Timing: In Canada, most taxes on an estate are deferred until the second spouse passes. A JLT policy triggers a tax-free payout at the exact moment the CRA bill arrives.

Liquidity: It provides the cash needed to pay probate fees and capital gains, so your kids don't have to sell the family home or the cottage just to pay the taxes.

The Bottom Line:

It’s not about the payout for you; it’s about the legacy for them. It ensures that 100% of what you built stays with your family.

Looking to see how the math works for your specific situation ? Let’s run the numbers.

📍 Brock Vale | Sun Life

📞 613-243-0015

When we talk about estate planning in 2026, one of the biggest hurdles isn't the inheritance itself—it’s the tax bill that comes with it.

If you own a home, a cottage, or a significant RRIF, your heirs could be looking at a major tax hit from the CRA.

The Solution? Joint Last-to-Die (JLT) Life Insurance.

What is it?

Unlike traditional life insurance that pays out when one person passes away, a JLT policy covers two people (usually spouses) and pays out only after the second person passes.

Why is this the "Gold Standard" for Estate Planning?

Cost-Efficient: Because the payout is deferred until the second death, the premiums are typically significantly lower than two individual policies.

Perfect Timing: In Canada, most taxes on an estate are deferred until the second spouse passes. A JLT policy triggers a tax-free payout at the exact moment the CRA bill arrives.

Liquidity: It provides the cash needed to pay probate fees and capital gains, so your kids don't have to sell the family home or the cottage just to pay the taxes.

The Bottom Line:

It’s not about the payout for you; it’s about the legacy for them. It ensures that 100% of what you built stays with your family.

Looking to see how the math works for your specific situation ? Let’s run the numbers.

📍 Brock Vale | Sun Life

📞 613-243-0015

From health spending accounts to enhanced benefits, there are ways to cover what provincial plans don't — and sometimes save on taxes too. Let's explore what fits your needs and budget.

From health spending accounts to enhanced benefits, there are ways to cover what provincial plans don't — and sometimes save on taxes too. Let's explore what fits your needs and budget.

A withdrawal strategy can help create dependable income while helping you manage risk. Let’s chat about income planning basics that fit your needs. https://advisor.sunlife.ca/brock.vale/

A withdrawal strategy can help create dependable income while helping you manage risk. Let’s chat about income planning basics that fit your needs. https://advisor.sunlife.ca/brock.vale/

Tax season isn't just about filing — it's about planning ahead. From RRSP contributions to income splitting strategies, there are things you can do now to better position your finances for next year and beyond.

Get in touch to find out what strategies work best for you. https://advisor.sunlife.ca/brock.vale/

Get in touch to find out what strategies work best for you. https://advisor.sunlife.ca/brock.vale/

Tax season isn't just about filing — it's about planning ahead. From RRSP contributions to income splitting strategies, there are things you can do now to better position your finances for next year and beyond.

Get in touch to find out what strategies work best for you. https://advisor.sunlife.ca/brock.vale/

Get in touch to find out what strategies work best for you. https://advisor.sunlife.ca/brock.vale/

Wealth isn’t about complexity. It’s about clarity. 🧠

Being a young Wealth Advisor gives me a unique perspective. I’m looking at the finish line every day through the lives of my clients.

Here is what the "winners" at the end of the race are actually looking for:

- Less debt.

- Fewer moving parts.

- Simple, effective investments.

- Peace of mind.

No one regrets missing the "hot stock" of 2024. They regret the stress of not being in control.

If you want to build true wealth, stop looking for the most complicated path. Look for the clearest one. 🚀

Being a young Wealth Advisor gives me a unique perspective. I’m looking at the finish line every day through the lives of my clients.

Here is what the "winners" at the end of the race are actually looking for:

- Less debt.

- Fewer moving parts.

- Simple, effective investments.

- Peace of mind.

No one regrets missing the "hot stock" of 2024. They regret the stress of not being in control.

If you want to build true wealth, stop looking for the most complicated path. Look for the clearest one. 🚀

Navigating life insurance options can be overwhelming. Whether finishing school, buying a first home or starting a family, finding the right plan that fits life's unique journey is essential.

I can help secure your future. Let me know how we can help.

I can help secure your future. Let me know how we can help.

Navigating life insurance options can be overwhelming. Whether finishing school, buying a first home or starting a family, finding the right plan that fits life's unique journey is essential.

I can help secure your future. Let me know how we can help.

I can help secure your future. Let me know how we can help.

The Biggest Retirement Myth: "I need to be 100% safe." 🛑

Common wisdom says that as you approach retirement, you should move everything into "safe" investments like GICs or bonds.

But here’s the truth: Retirement isn't a single event; it’s a 30-year journey. If you stop your growth too early, you risk:

Inflation Erosion: Your purchasing power drops while costs rise.

Outliving Your Money: A stagnant portfolio may not keep up with your lifestyle.

Working Longer: You might be delaying your retirement unnecessarily because your "safe" strategy isn't doing the heavy lifting anymore.

You don’t need all your money on Day 1. We plan for the short-term cash you need AND the long-term growth you still require.

Brock Vale - 613-243-0015

brock.vale@sunlife.com

Common wisdom says that as you approach retirement, you should move everything into "safe" investments like GICs or bonds.

But here’s the truth: Retirement isn't a single event; it’s a 30-year journey. If you stop your growth too early, you risk:

Inflation Erosion: Your purchasing power drops while costs rise.

Outliving Your Money: A stagnant portfolio may not keep up with your lifestyle.

Working Longer: You might be delaying your retirement unnecessarily because your "safe" strategy isn't doing the heavy lifting anymore.

You don’t need all your money on Day 1. We plan for the short-term cash you need AND the long-term growth you still require.

Brock Vale - 613-243-0015

brock.vale@sunlife.com

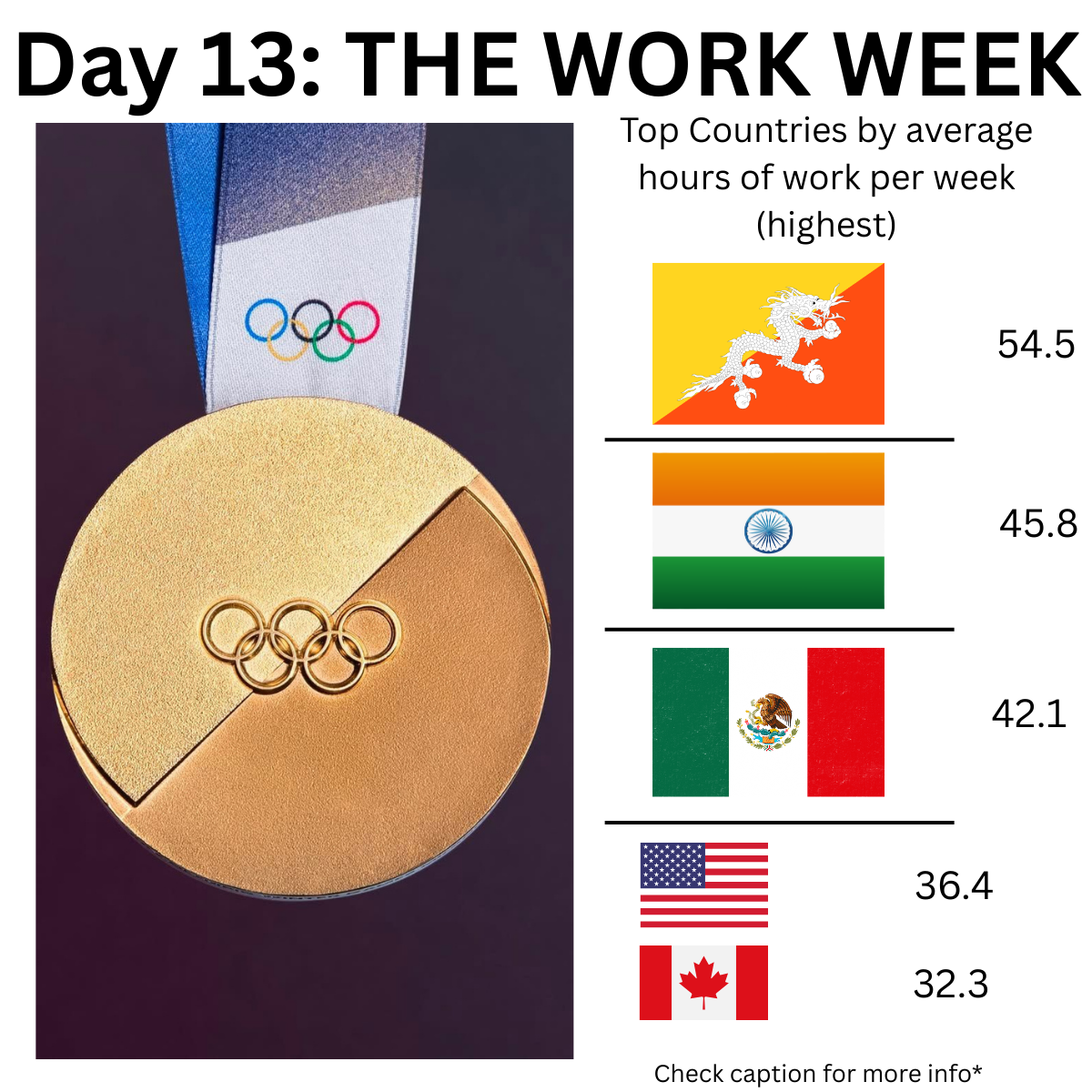

Is Your Financial Plan Built for Overtime?

It’s Quarter-Final day for Team Canada Men’s Hockey! 🇨🇦 In the Olympics, coaches have to manage "Time on Ice" perfectly. If a player stays out too long, they burn out. If they don’t play enough, they don’t get results.

In the "Economic Olympics," we track this by looking at the average hours worked per week. Check out the global leaderboard for 2026:

🏆 The Weekly Endurance Leaderboard (Avg. Hours Worked)

1️⃣ Bhutan: 54.5 hrs

2️⃣ India: 45.8 hrs

3️⃣ Mexico: 42.1 hrs

4️⃣ USA: 36.4 hrs

5️⃣ Canada: 32.3 hrs

6️⃣ Germany: 25.5 hrs

Wait—only 32.3 hours for Canada? 🤨

That’s the national average, which includes part-time workers, seasonal shifts, and our generous vacation time.

The goal of a great financial plan isn’t to make you work more hours—it’s to ensure that the hours you DO work are building enough momentum so that eventually, your money starts doing the heavy lifting for you.

Source: https://data.oecd.org/emp/hours-worked.htm

Whether you’re clocking 30 hours or 60, let’s make sure your retirement strategy is ready for the podium.

Give me a shout to review your "scouting report."

📞 613-243-0015

It’s Quarter-Final day for Team Canada Men’s Hockey! 🇨🇦 In the Olympics, coaches have to manage "Time on Ice" perfectly. If a player stays out too long, they burn out. If they don’t play enough, they don’t get results.

In the "Economic Olympics," we track this by looking at the average hours worked per week. Check out the global leaderboard for 2026:

🏆 The Weekly Endurance Leaderboard (Avg. Hours Worked)

1️⃣ Bhutan: 54.5 hrs

2️⃣ India: 45.8 hrs

3️⃣ Mexico: 42.1 hrs

4️⃣ USA: 36.4 hrs

5️⃣ Canada: 32.3 hrs

6️⃣ Germany: 25.5 hrs

Wait—only 32.3 hours for Canada? 🤨

That’s the national average, which includes part-time workers, seasonal shifts, and our generous vacation time.

The goal of a great financial plan isn’t to make you work more hours—it’s to ensure that the hours you DO work are building enough momentum so that eventually, your money starts doing the heavy lifting for you.

Source: https://data.oecd.org/emp/hours-worked.htm

Whether you’re clocking 30 hours or 60, let’s make sure your retirement strategy is ready for the podium.

Give me a shout to review your "scouting report."

📞 613-243-0015

Is Your Financial Plan Built for Overtime?

It’s Quarter-Final day for Team Canada Men’s Hockey! 🇨🇦 In the Olympics, coaches have to manage "Time on Ice" perfectly. If a player stays out too long, they burn out. If they don’t play enough, they don’t get results.

In the "Economic Olympics," we track this by looking at the average hours worked per week. Check out the global leaderboard for 2026:

🏆 The Weekly Endurance Leaderboard (Avg. Hours Worked)

1️⃣ Bhutan: 54.5 hrs

2️⃣ India: 45.8 hrs

3️⃣ Mexico: 42.1 hrs

4️⃣ USA: 36.4 hrs

5️⃣ Canada: 32.3 hrs

6️⃣ Germany: 25.5 hrs

Wait—only 32.3 hours for Canada? 🤨

That’s the national average, which includes part-time workers, seasonal shifts, and our generous vacation time.

The goal of a great financial plan isn’t to make you work more hours—it’s to ensure that the hours you DO work are building enough momentum so that eventually, your money starts doing the heavy lifting for you.

Source: https://data.oecd.org/emp/hours-worked.htm

Whether you’re clocking 30 hours or 60, let’s make sure your retirement strategy is ready for the podium.

Give me a shout to review your "scouting report."

📞 613-243-0015

It’s Quarter-Final day for Team Canada Men’s Hockey! 🇨🇦 In the Olympics, coaches have to manage "Time on Ice" perfectly. If a player stays out too long, they burn out. If they don’t play enough, they don’t get results.

In the "Economic Olympics," we track this by looking at the average hours worked per week. Check out the global leaderboard for 2026:

🏆 The Weekly Endurance Leaderboard (Avg. Hours Worked)

1️⃣ Bhutan: 54.5 hrs

2️⃣ India: 45.8 hrs

3️⃣ Mexico: 42.1 hrs

4️⃣ USA: 36.4 hrs

5️⃣ Canada: 32.3 hrs

6️⃣ Germany: 25.5 hrs

Wait—only 32.3 hours for Canada? 🤨

That’s the national average, which includes part-time workers, seasonal shifts, and our generous vacation time.

The goal of a great financial plan isn’t to make you work more hours—it’s to ensure that the hours you DO work are building enough momentum so that eventually, your money starts doing the heavy lifting for you.

Source: https://data.oecd.org/emp/hours-worked.htm

Whether you’re clocking 30 hours or 60, let’s make sure your retirement strategy is ready for the podium.

Give me a shout to review your "scouting report."

📞 613-243-0015

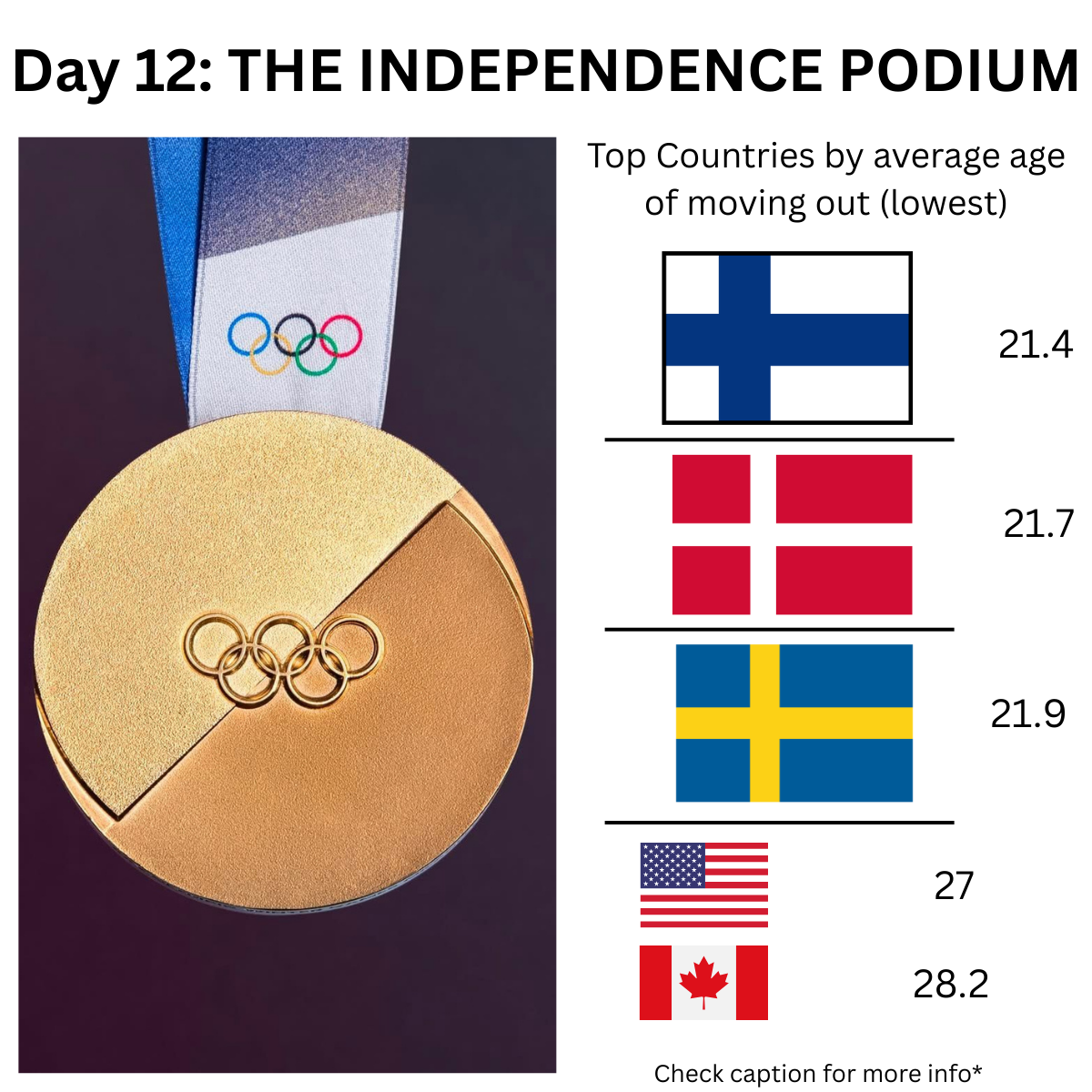

🏠 Day 12: Is the Nest Getting Crowded?

We’ve all seen the headlines about the "Boomerang Generation," but how does Canada actually compare to the rest of the world when it comes to kids moving out in 2026?

The 2026 Global Standings: Average Age of Moving Out (2026)

🥇 GOLD: Finland (21.4 years) The world leader in launching early. A mix of government student support and a culture that prizes independence keeps them in first place.

🥈 SILVER: Denmark (21.7 years) Denmark takes the Silver. Like their neighbors, Danish young adults benefit from a system that makes moving out for school or work financially feasible much earlier than in North America.

🥉 BRONZE: Sweden (21.9 years) Rounding out the Nordic sweep, Sweden takes the Bronze. Independence usually happens right around the end of high school or the start of university.

🇺🇸 The USA Shift: For the first time, the average age in the US has climbed to 27. Rental affordability is keeping the next generation home longer than ever before.

🇨🇦 Where is Canada?

We land even higher. In Canada, the average age of independence is now 28.2. Many young professionals are staying home well into their late 20s to build a down payment.

The Plot Twist: Think 28 is old? In Croatia, the average person doesn't move out until they are 31.3!

If your adult children are still at home, the "Parental Bank" needs a strategy. In 2026, the FHSA (First Home Savings Account) and the $7,000 TFSA limit are the best tools to help them move from your basement to their own front door.

Is your nest feeling a little full? Let’s chat about how we can build a plan to get the next generation launched without delaying your own retirement. 🚀

Brock Vale

Financial Advisor, Sun Life

📍 Kingston, Ontario

📞 613-243-0015

Source: https://ec.europa.eu/eurostat/web/products-eurostat-news/w/ddn-20250923-1?hl=en-CA

We’ve all seen the headlines about the "Boomerang Generation," but how does Canada actually compare to the rest of the world when it comes to kids moving out in 2026?

The 2026 Global Standings: Average Age of Moving Out (2026)

🥇 GOLD: Finland (21.4 years) The world leader in launching early. A mix of government student support and a culture that prizes independence keeps them in first place.

🥈 SILVER: Denmark (21.7 years) Denmark takes the Silver. Like their neighbors, Danish young adults benefit from a system that makes moving out for school or work financially feasible much earlier than in North America.

🥉 BRONZE: Sweden (21.9 years) Rounding out the Nordic sweep, Sweden takes the Bronze. Independence usually happens right around the end of high school or the start of university.

🇺🇸 The USA Shift: For the first time, the average age in the US has climbed to 27. Rental affordability is keeping the next generation home longer than ever before.

🇨🇦 Where is Canada?

We land even higher. In Canada, the average age of independence is now 28.2. Many young professionals are staying home well into their late 20s to build a down payment.

The Plot Twist: Think 28 is old? In Croatia, the average person doesn't move out until they are 31.3!

If your adult children are still at home, the "Parental Bank" needs a strategy. In 2026, the FHSA (First Home Savings Account) and the $7,000 TFSA limit are the best tools to help them move from your basement to their own front door.

Is your nest feeling a little full? Let’s chat about how we can build a plan to get the next generation launched without delaying your own retirement. 🚀

Brock Vale

Financial Advisor, Sun Life

📍 Kingston, Ontario

📞 613-243-0015

Source: https://ec.europa.eu/eurostat/web/products-eurostat-news/w/ddn-20250923-1?hl=en-CA

🏠 Day 12: Is the Nest Getting Crowded?

We’ve all seen the headlines about the "Boomerang Generation," but how does Canada actually compare to the rest of the world when it comes to kids moving out in 2026?

The 2026 Global Standings: Average Age of Moving Out (2026)

🥇 GOLD: Finland (21.4 years) The world leader in launching early. A mix of government student support and a culture that prizes independence keeps them in first place.

🥈 SILVER: Denmark (21.7 years) Denmark takes the Silver. Like their neighbors, Danish young adults benefit from a system that makes moving out for school or work financially feasible much earlier than in North America.

🥉 BRONZE: Sweden (21.9 years) Rounding out the Nordic sweep, Sweden takes the Bronze. Independence usually happens right around the end of high school or the start of university.

🇺🇸 The USA Shift: For the first time, the average age in the US has climbed to 27. Rental affordability is keeping the next generation home longer than ever before.

🇨🇦 Where is Canada?

We land even higher. In Canada, the average age of independence is now 28.2. Many young professionals are staying home well into their late 20s to build a down payment.

The Plot Twist: Think 28 is old? In Croatia, the average person doesn't move out until they are 31.3!

If your adult children are still at home, the "Parental Bank" needs a strategy. In 2026, the FHSA (First Home Savings Account) and the $7,000 TFSA limit are the best tools to help them move from your basement to their own front door.

Is your nest feeling a little full? Let’s chat about how we can build a plan to get the next generation launched without delaying your own retirement. 🚀

Brock Vale

Financial Advisor, Sun Life

📍 Kingston, Ontario

📞 613-243-0015

Source: https://ec.europa.eu/eurostat/web/products-eurostat-news/w/ddn-20250923-1?hl=en-CA

We’ve all seen the headlines about the "Boomerang Generation," but how does Canada actually compare to the rest of the world when it comes to kids moving out in 2026?

The 2026 Global Standings: Average Age of Moving Out (2026)

🥇 GOLD: Finland (21.4 years) The world leader in launching early. A mix of government student support and a culture that prizes independence keeps them in first place.

🥈 SILVER: Denmark (21.7 years) Denmark takes the Silver. Like their neighbors, Danish young adults benefit from a system that makes moving out for school or work financially feasible much earlier than in North America.

🥉 BRONZE: Sweden (21.9 years) Rounding out the Nordic sweep, Sweden takes the Bronze. Independence usually happens right around the end of high school or the start of university.

🇺🇸 The USA Shift: For the first time, the average age in the US has climbed to 27. Rental affordability is keeping the next generation home longer than ever before.

🇨🇦 Where is Canada?

We land even higher. In Canada, the average age of independence is now 28.2. Many young professionals are staying home well into their late 20s to build a down payment.

The Plot Twist: Think 28 is old? In Croatia, the average person doesn't move out until they are 31.3!

If your adult children are still at home, the "Parental Bank" needs a strategy. In 2026, the FHSA (First Home Savings Account) and the $7,000 TFSA limit are the best tools to help them move from your basement to their own front door.

Is your nest feeling a little full? Let’s chat about how we can build a plan to get the next generation launched without delaying your own retirement. 🚀

Brock Vale

Financial Advisor, Sun Life

📍 Kingston, Ontario

📞 613-243-0015

Source: https://ec.europa.eu/eurostat/web/products-eurostat-news/w/ddn-20250923-1?hl=en-CA

Have questions?

Here to help answer your questions, provide clarity about products and get you started on the road to achieving your goals.