Stay Informed

Brock is active on social media - follow him on Facebook, Instagram and LinkedIn.

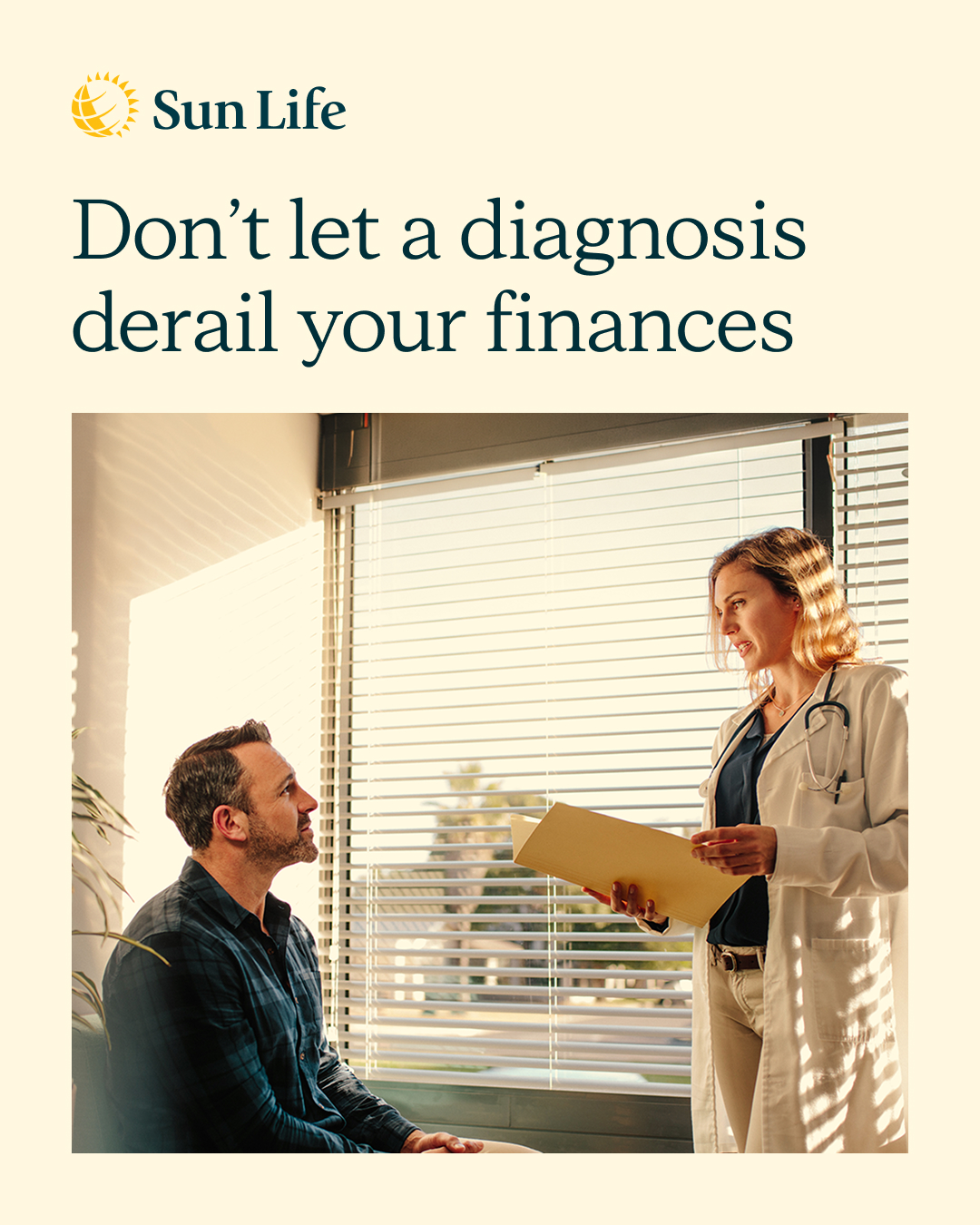

A serious illness can impact more than your health, it can disrupt your income, savings and long-term goals. Critical illness insurance pays a lump sum benefit upon diagnosis of covered conditions like cancer, heart attack or stroke, so you have financial support when it matters most. Let’s talk about how critical illness coverage can protect your financial plan before you need it. https://advisor.sunlife.ca/brock.vale/

A serious illness can impact more than your health, it can disrupt your income, savings and long-term goals. Critical illness insurance pays a lump sum benefit upon diagnosis of covered conditions like cancer, heart attack or stroke, so you have financial support when it matters most. Let’s talk about how critical illness coverage can protect your financial plan before you need it. https://advisor.sunlife.ca/brock.vale/

It's never too early to start. When kids learn about money young, they make smarter choices later. 💡

Here's how to get started:

• Give them an allowance and let them decide how to spend it

• Talk openly about budgeting and saving

• Show them how saving reaches big goals 🎯

• Make learning fun and age-appropriate

Small money conversations today build confident adults tomorrow.

Ready to help your kids build money confidence? Reach out and let's talk about it. https://advisor.sunlife.ca/brock.vale/

Here's how to get started:

• Give them an allowance and let them decide how to spend it

• Talk openly about budgeting and saving

• Show them how saving reaches big goals 🎯

• Make learning fun and age-appropriate

Small money conversations today build confident adults tomorrow.

Ready to help your kids build money confidence? Reach out and let's talk about it. https://advisor.sunlife.ca/brock.vale/

It's never too early to start. When kids learn about money young, they make smarter choices later. 💡

Here's how to get started:

• Give them an allowance and let them decide how to spend it

• Talk openly about budgeting and saving

• Show them how saving reaches big goals 🎯

• Make learning fun and age-appropriate

Small money conversations today build confident adults tomorrow.

Ready to help your kids build money confidence? Reach out and let's talk about it. https://advisor.sunlife.ca/brock.vale/

Here's how to get started:

• Give them an allowance and let them decide how to spend it

• Talk openly about budgeting and saving

• Show them how saving reaches big goals 🎯

• Make learning fun and age-appropriate

Small money conversations today build confident adults tomorrow.

Ready to help your kids build money confidence? Reach out and let's talk about it. https://advisor.sunlife.ca/brock.vale/

Your investments should do more than grow — they should support where you’re headed. A well-balanced strategy can help align your money with your goals as they evolve. Let’s build an investment approach designed around you. https://advisor.sunlife.ca/brock.vale/

Your investments should do more than grow — they should support where you’re headed. A well-balanced strategy can help align your money with your goals as they evolve. Let’s build an investment approach designed around you. https://advisor.sunlife.ca/brock.vale/

Are you a parent or grandparent?

Are you looking to lock in a head start to a strong financial foundation for your child?

Purchasing a Participating Life Insurance Policy on your child is a great way to:

- Lock in the lowest cost

- Guarantee insurability for when they are older

- Leave a legacy gift in a tax efficient way that offers growth!

If this is something that you would like to look into, reach out!

Brock Vale

brock.vale@sunlife.com

613-243-0015

Are you looking to lock in a head start to a strong financial foundation for your child?

Purchasing a Participating Life Insurance Policy on your child is a great way to:

- Lock in the lowest cost

- Guarantee insurability for when they are older

- Leave a legacy gift in a tax efficient way that offers growth!

If this is something that you would like to look into, reach out!

Brock Vale

brock.vale@sunlife.com

613-243-0015

Are you a parent or grandparent?

Are you looking to lock in a head start to a strong financial foundation for your child?

Purchasing a Participating Life Insurance Policy on your child is a great way to:

- Lock in the lowest cost

- Guarantee insurability for when they are older

- Leave a legacy gift in a tax efficient way that offers growth!

If this is something that you would like to look into, reach out!

Brock Vale

brock.vale@sunlife.com

613-243-0015

Are you looking to lock in a head start to a strong financial foundation for your child?

Purchasing a Participating Life Insurance Policy on your child is a great way to:

- Lock in the lowest cost

- Guarantee insurability for when they are older

- Leave a legacy gift in a tax efficient way that offers growth!

If this is something that you would like to look into, reach out!

Brock Vale

brock.vale@sunlife.com

613-243-0015

Buying a home, growing your family, building your career — there’s a lot to balance. Creating a personalized financial roadmap early can help you stay on track while still living for today. Small steps today can make a meaningful difference over time. Get in touch to discuss options that will work best for you. https://advisor.sunlife.ca/brock.vale/

Buying a home, growing your family, building your career — there’s a lot to balance. Creating a personalized financial roadmap early can help you stay on track while still living for today. Small steps today can make a meaningful difference over time. Get in touch to discuss options that will work best for you. https://advisor.sunlife.ca/brock.vale/

Life can be unpredictable. The right protection can help you stay financially secure when it matters most. Insurance can play a key role in supporting your overall financial approach. Let’s review your coverage and make sure it fits your needs. https://advisor.sunlife.ca/brock.vale/

Life can be unpredictable. The right protection can help you stay financially secure when it matters most. Insurance can play a key role in supporting your overall financial approach. Let’s review your coverage and make sure it fits your needs. https://advisor.sunlife.ca/brock.vale/

6:00 AM on a Friday should be an absolute crime. 🥱

My morning started with a rude awakening today because Brittany decided she's shifting her entire Friday schedule. Her master plan? Punching the clock at 7:00 AM so she can be completely done with work by 3:00 PM.

Don’t get me wrong, a 3:00 PM weekend kickoff sounds amazing on paper. But I told her if you are willingly getting up at 6:00 in the morning to head straight into work, you should probably be wearing a hard hat and working a heavy labor or construction job. 👷♂️🏗️

Either that, or I just desperately need to find some caffeine to survive the rest of this morning. ☕🚀

It got me thinking about the ultimate pre-weekend schedule debate:

👇 If you could choose your exact start time on a Friday to wrap up your week, what hour are you choosing? Are you grinding it out early like Brittany, or sleeping in?

Let me know in the comments!

My morning started with a rude awakening today because Brittany decided she's shifting her entire Friday schedule. Her master plan? Punching the clock at 7:00 AM so she can be completely done with work by 3:00 PM.

Don’t get me wrong, a 3:00 PM weekend kickoff sounds amazing on paper. But I told her if you are willingly getting up at 6:00 in the morning to head straight into work, you should probably be wearing a hard hat and working a heavy labor or construction job. 👷♂️🏗️

Either that, or I just desperately need to find some caffeine to survive the rest of this morning. ☕🚀

It got me thinking about the ultimate pre-weekend schedule debate:

👇 If you could choose your exact start time on a Friday to wrap up your week, what hour are you choosing? Are you grinding it out early like Brittany, or sleeping in?

Let me know in the comments!

6:00 AM on a Friday should be an absolute crime. 🥱

My morning started with a rude awakening today because Brittany decided she's shifting her entire Friday schedule. Her master plan? Punching the clock at 7:00 AM so she can be completely done with work by 3:00 PM.

Don’t get me wrong, a 3:00 PM weekend kickoff sounds amazing on paper. But I told her if you are willingly getting up at 6:00 in the morning to head straight into work, you should probably be wearing a hard hat and working a heavy labor or construction job. 👷♂️🏗️

Either that, or I just desperately need to find some caffeine to survive the rest of this morning. ☕🚀

It got me thinking about the ultimate pre-weekend schedule debate:

👇 If you could choose your exact start time on a Friday to wrap up your week, what hour are you choosing? Are you grinding it out early like Brittany, or sleeping in?

Let me know in the comments!

My morning started with a rude awakening today because Brittany decided she's shifting her entire Friday schedule. Her master plan? Punching the clock at 7:00 AM so she can be completely done with work by 3:00 PM.

Don’t get me wrong, a 3:00 PM weekend kickoff sounds amazing on paper. But I told her if you are willingly getting up at 6:00 in the morning to head straight into work, you should probably be wearing a hard hat and working a heavy labor or construction job. 👷♂️🏗️

Either that, or I just desperately need to find some caffeine to survive the rest of this morning. ☕🚀

It got me thinking about the ultimate pre-weekend schedule debate:

👇 If you could choose your exact start time on a Friday to wrap up your week, what hour are you choosing? Are you grinding it out early like Brittany, or sleeping in?

Let me know in the comments!

Ease into retirement with Sun Life One Plan

Your retirement plan should feel unique and tailored to you. Sun Life One Plan can help bring your goals, investments and income strategy together so you can see what’s possible. Get in touch to start planning your dream retirement. https://advisor.sunlife.ca/brock.vale/

#SunLifeOnePlan #RetirementPlanning

#SunLifeOnePlan #RetirementPlanning

Watch video

A tax refund can feel like “extra” money — but it can also be a powerful planning moment. Putting it toward the right goal (RRSP, TFSA, debt strategy, or a targeted savings plan) can help you build momentum. The best move depends on your priorities — and your timeline. Let’s chat about your goals.

A tax refund can feel like “extra” money — but it can also be a powerful planning moment. Putting it toward the right goal (RRSP, TFSA, debt strategy, or a targeted savings plan) can help you build momentum. The best move depends on your priorities — and your timeline. Let’s chat about your goals.

Your retirement plan should feel personal — not generic. Sun Life One Plan can help bring your goals, investments and income strategy together into one clear financial roadmap, so you can see what’s possible and adjust as life changes. What would you like your retirement to look like? https://advisor.sunlife.ca/brock.vale/

#SunLifeOnePlan #RetirementPlanning

#SunLifeOnePlan #RetirementPlanning

Your retirement plan should feel personal — not generic. Sun Life One Plan can help bring your goals, investments and income strategy together into one clear financial roadmap, so you can see what’s possible and adjust as life changes. What would you like your retirement to look like? https://advisor.sunlife.ca/brock.vale/

#SunLifeOnePlan #RetirementPlanning

#SunLifeOnePlan #RetirementPlanning

Congratulations on graduating! Now comes the next chapter, managing student debt while building your future. From repayment strategies to integrating loans into your financial roadmap, let's make sure you're set up for success. Whether it's buying a first home or saving for further education, we can help you navigate it all. Let's talk!

Congratulations on graduating! Now comes the next chapter, managing student debt while building your future. From repayment strategies to integrating loans into your financial roadmap, let's make sure you're set up for success. Whether it's buying a first home or saving for further education, we can help you navigate it all. Let's talk!

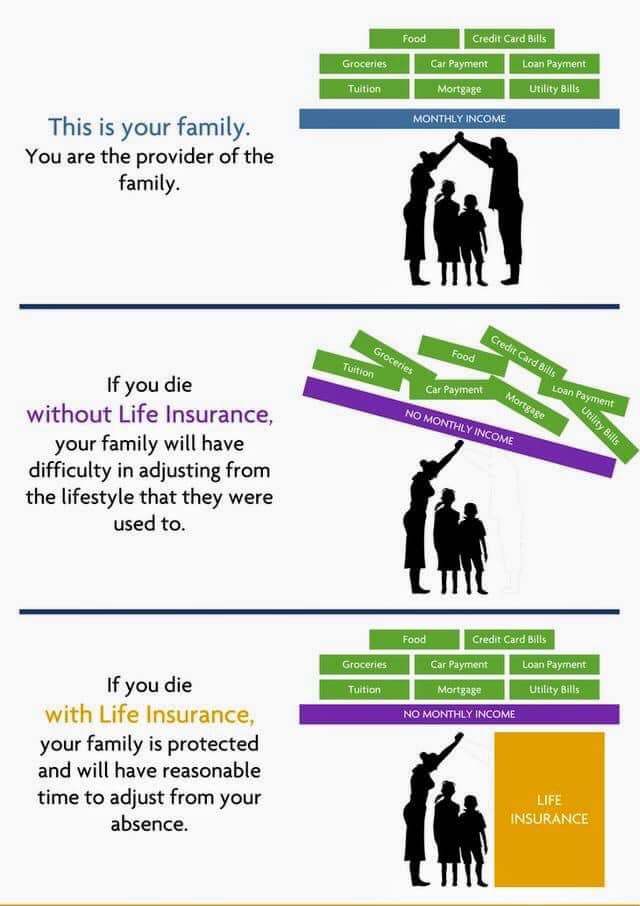

If your family depends on you now, what would happen if you weren't there?

Life Insurance can provide for your family in case something were to happen to you.

Life Insurance can provide for your family in case something were to happen to you.

If your family depends on you now, what would happen if you weren't there?

Life Insurance can provide for your family in case something were to happen to you.

Life Insurance can provide for your family in case something were to happen to you.

An inheritance is more than just a balance in a bank account.

It’s a bridge between the hard work of the past and the dreams of your future.

Whether it’s funding a grandchild’s education, finally taking that family trip, or ensuring your own retirement is secure, every dollar has a story. My role isn't just to "manage money", it’s to help you align these new resources with your personal values.

If you’ve inherited wealth recently, you don't have to figure it out alone. Let’s sit down and create a plan that honours where the money came from while focusing on where you want to go.

📞 613-243-0015

It’s a bridge between the hard work of the past and the dreams of your future.

Whether it’s funding a grandchild’s education, finally taking that family trip, or ensuring your own retirement is secure, every dollar has a story. My role isn't just to "manage money", it’s to help you align these new resources with your personal values.

If you’ve inherited wealth recently, you don't have to figure it out alone. Let’s sit down and create a plan that honours where the money came from while focusing on where you want to go.

📞 613-243-0015

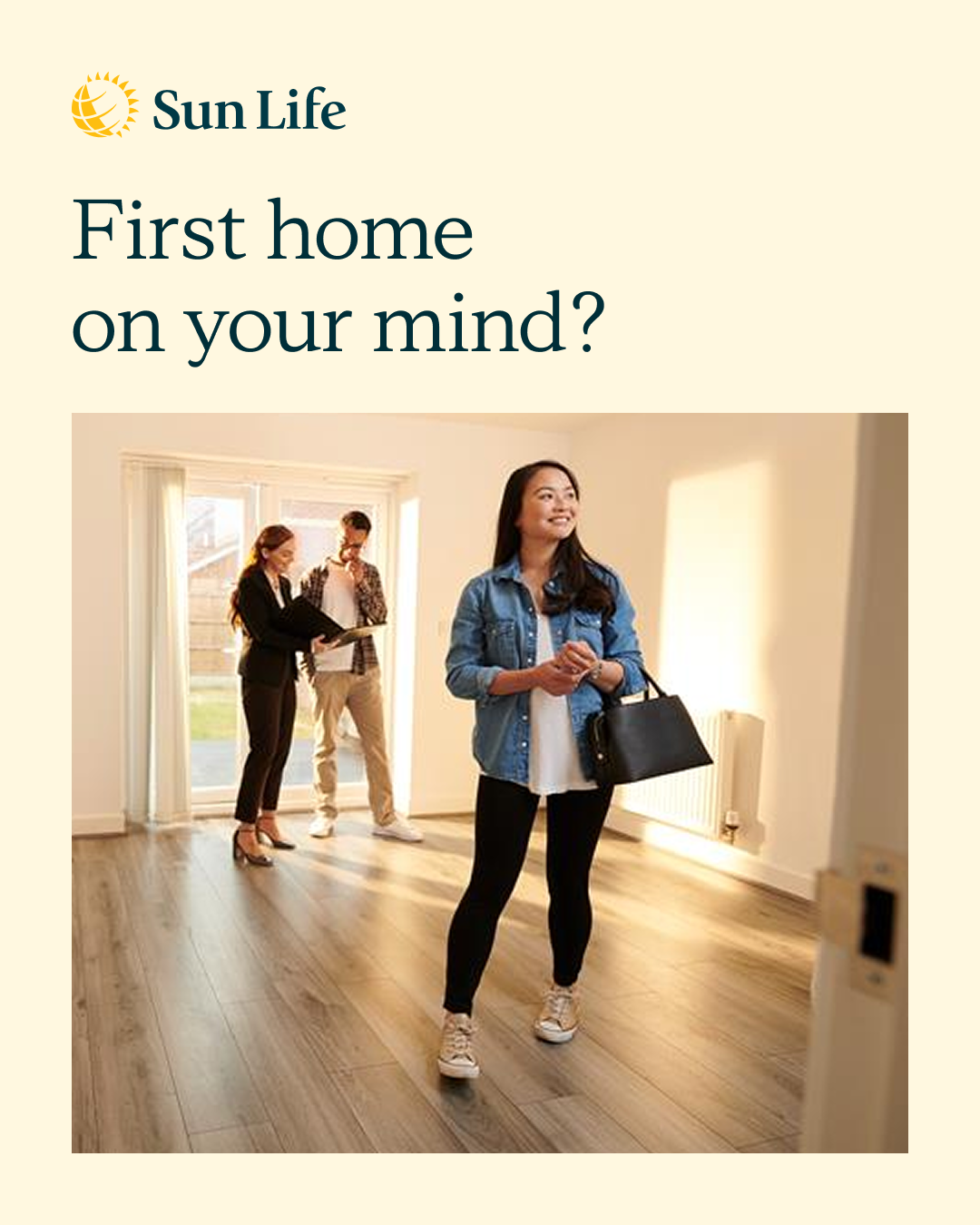

Dreaming of owning your first home? You might not know all the tools available to help you get there.

From RRSP Home Buyer's Plan withdrawals to the new First Home Savings Account (FHSA), there are smart strategies to help accelerate your down payment savings. Let's explore which options work best for your situation. Reach out today!

From RRSP Home Buyer's Plan withdrawals to the new First Home Savings Account (FHSA), there are smart strategies to help accelerate your down payment savings. Let's explore which options work best for your situation. Reach out today!

Dreaming of owning your first home? You might not know all the tools available to help you get there.

From RRSP Home Buyer's Plan withdrawals to the new First Home Savings Account (FHSA), there are smart strategies to help accelerate your down payment savings. Let's explore which options work best for your situation. Reach out today!

From RRSP Home Buyer's Plan withdrawals to the new First Home Savings Account (FHSA), there are smart strategies to help accelerate your down payment savings. Let's explore which options work best for your situation. Reach out today!

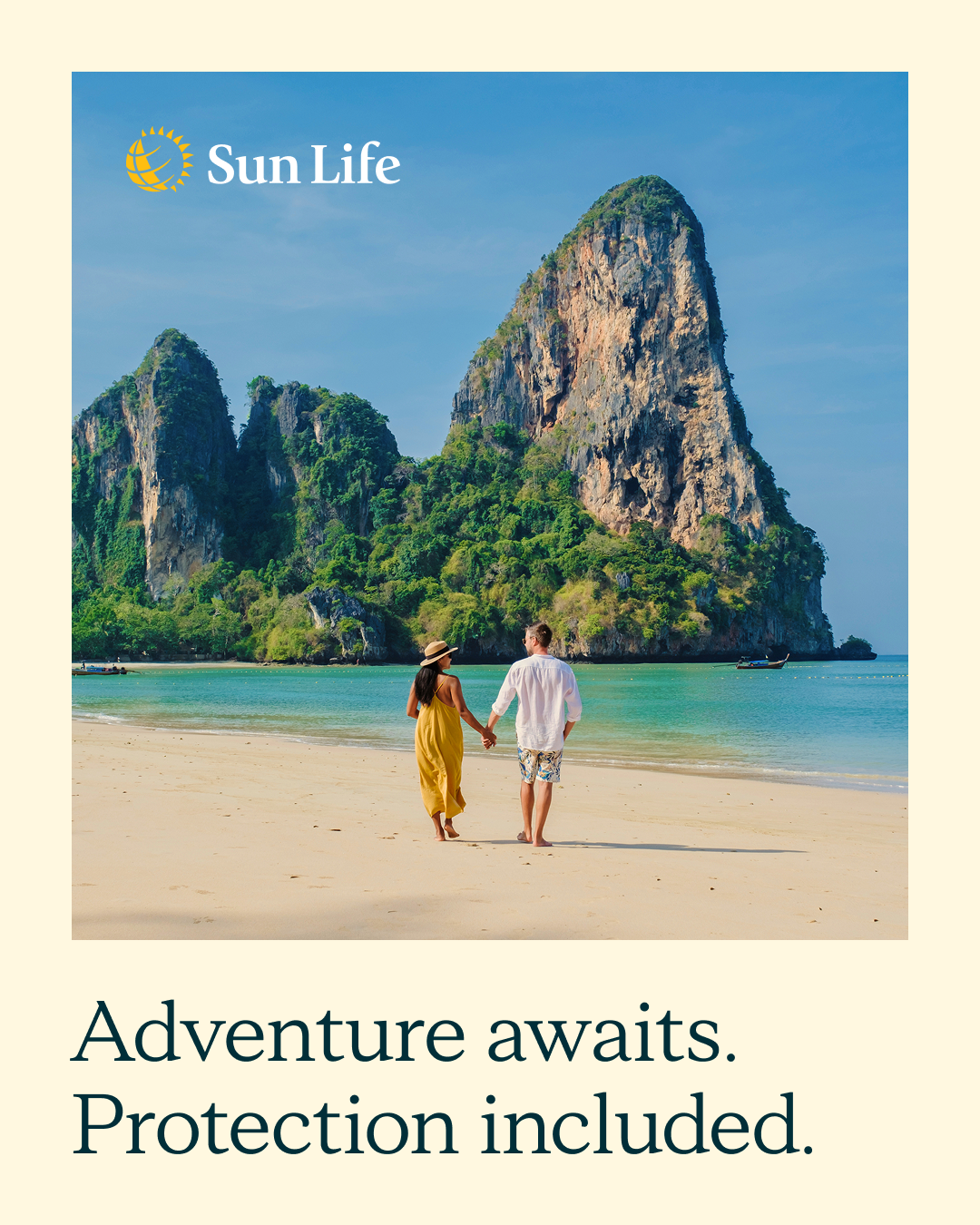

Planning that dream summer getaway? Travel insurance is your safety net. From medical emergencies to trip cancellations, the right coverage means you can explore the world with confidence. Don't let unexpected costs derail your plans. You want to be protected for every adventure. What's your next destination?

Planning that dream summer getaway? Travel insurance is your safety net. From medical emergencies to trip cancellations, the right coverage means you can explore the world with confidence. Don't let unexpected costs derail your plans. You want to be protected for every adventure. What's your next destination?

Sun Life recently hosted a conference in Waterloo for hundreds of young financial advisors. I am proud to wear my new jacket for completing the 2nd highest amount plans in the Toronto region.

Not only did I get a new jacket, but I helped 25 families feel more confident in their finances in the first three months of 2026!

These plans ranged from couples saving to buy their first home, soon to be retirees realizing when they can retire, and retirees making sure that their estate would not go to taxes.

After nearly every meeting with one of these plans presented, I was asked "how much do I owe you now?". Odd question considering I already explained how the pay works, but these plans are free.

If you would like a clear guideline on where you are financially and what it will take to reach your goals, look no further and don't hesitate to reach out.

Brock Vale

brock.vale@sunlife.com

613-243-0015

Not only did I get a new jacket, but I helped 25 families feel more confident in their finances in the first three months of 2026!

These plans ranged from couples saving to buy their first home, soon to be retirees realizing when they can retire, and retirees making sure that their estate would not go to taxes.

After nearly every meeting with one of these plans presented, I was asked "how much do I owe you now?". Odd question considering I already explained how the pay works, but these plans are free.

If you would like a clear guideline on where you are financially and what it will take to reach your goals, look no further and don't hesitate to reach out.

Brock Vale

brock.vale@sunlife.com

613-243-0015

Sun Life recently hosted a conference in Waterloo for hundreds of young financial advisors. I am proud to wear my new jacket for completing the 2nd highest amount plans in the Toronto region.

Not only did I get a new jacket, but I helped 25 families feel more confident in their finances in the first three months of 2026!

These plans ranged from couples saving to buy their first home, soon to be retirees realizing when they can retire, and retirees making sure that their estate would not go to taxes.

After nearly every meeting with one of these plans presented, I was asked "how much do I owe you now?". Odd question considering I already explained how the pay works, but these plans are free.

If you would like a clear guideline on where you are financially and what it will take to reach your goals, look no further and don't hesitate to reach out.

Brock Vale

brock.vale@sunlife.com

613-243-0015

Not only did I get a new jacket, but I helped 25 families feel more confident in their finances in the first three months of 2026!

These plans ranged from couples saving to buy their first home, soon to be retirees realizing when they can retire, and retirees making sure that their estate would not go to taxes.

After nearly every meeting with one of these plans presented, I was asked "how much do I owe you now?". Odd question considering I already explained how the pay works, but these plans are free.

If you would like a clear guideline on where you are financially and what it will take to reach your goals, look no further and don't hesitate to reach out.

Brock Vale

brock.vale@sunlife.com

613-243-0015

One of the most frequent questions I get in is: 'How much of my inheritance will the government take?'

In Canada, we don't have a direct 'inheritance tax' for the recipient, but that doesn’t mean the transition is tax-free. Between the deceased’s final tax return, capital gains on secondary properties (like that cottage that has been in the family forever), and Ontario’s probate fees, the estate can shrink quickly if not managed correctly.

3 Things to Check Today:

- Is the property a primary residence or an investment?

- Are there designated beneficiaries on RRSPs/TFSAs to bypass probate?

- Has the 'Estate Administration Tax' been calculated?

Strategic planning doesn't just save money; it preserves the legacy your loved ones worked hard to build. Let’s ensure the transition is as seamless as possible.

In Canada, we don't have a direct 'inheritance tax' for the recipient, but that doesn’t mean the transition is tax-free. Between the deceased’s final tax return, capital gains on secondary properties (like that cottage that has been in the family forever), and Ontario’s probate fees, the estate can shrink quickly if not managed correctly.

3 Things to Check Today:

- Is the property a primary residence or an investment?

- Are there designated beneficiaries on RRSPs/TFSAs to bypass probate?

- Has the 'Estate Administration Tax' been calculated?

Strategic planning doesn't just save money; it preserves the legacy your loved ones worked hard to build. Let’s ensure the transition is as seamless as possible.

Your tax refund is an opportunity to invest in the future. Instead of letting it sit, let's explore smart ways to put it to work. From RRSP contributions to investment strategies, there are options to help grow your wealth. Let's explore what works best for your goals. https://advisor.sunlife.ca/brock.vale/

Your tax refund is an opportunity to invest in the future. Instead of letting it sit, let's explore smart ways to put it to work. From RRSP contributions to investment strategies, there are options to help grow your wealth. Let's explore what works best for your goals. https://advisor.sunlife.ca/brock.vale/

Thinking about retirement? You're not alone — and the good news is you don't have to navigate it solo. Let's create a personalized retirement roadmap. Together we can explore income strategies, investment options and timelines that fit your vision. Get in touch today!

Thinking about retirement? You're not alone — and the good news is you don't have to navigate it solo. Let's create a personalized retirement roadmap. Together we can explore income strategies, investment options and timelines that fit your vision. Get in touch today!

Receiving an inheritance is a paradox. It’s a financial gain often born from a deeply personal loss.

In 2026, we are seeing more wealth being passed down than ever before, but that doesn't make the process any less overwhelming.

If you’ve recently found yourself managing an estate, my first piece of advice is often the most surprising: Do nothing. At least for a little while. I call this the 'Decision-Free Zone.' Before you pay off the mortgage or overhaul your portfolio, give yourself 3 to 6 months to simply process the change. Your future self will thank you for making decisions with a clear head rather than a grieving heart.

When you’re ready to talk about the next steps, without the pressure, I’m here to help you navigate the landscape.

In 2026, we are seeing more wealth being passed down than ever before, but that doesn't make the process any less overwhelming.

If you’ve recently found yourself managing an estate, my first piece of advice is often the most surprising: Do nothing. At least for a little while. I call this the 'Decision-Free Zone.' Before you pay off the mortgage or overhaul your portfolio, give yourself 3 to 6 months to simply process the change. Your future self will thank you for making decisions with a clear head rather than a grieving heart.

When you’re ready to talk about the next steps, without the pressure, I’m here to help you navigate the landscape.

Have questions?

Here to help answer your questions, provide clarity about products and get you started on the road to achieving your goals.