Keep up-to-date

Keep up to date with what’s going on. You can browse timely and relevant posts that might be helpful to you. Check back regularly to see what’s new.

Your Life Insurance Disappeared and You Don't Know It

You just left your job. Your paycheque stopped.

But so did something else you probably forgot about — your life insurance.

Most people have 1-2x their salary in group life coverage through work. Feels like enough, so they never think about it. But the second you leave, the coverage is gone.

And if your health changed since you started? Good luck qualifying for new coverage.

Group insurance is a benefit. Personal insurance is a plan. Big difference.

DM me if you only have coverage through work — I'll tell you what to look for.

But so did something else you probably forgot about — your life insurance.

Most people have 1-2x their salary in group life coverage through work. Feels like enough, so they never think about it. But the second you leave, the coverage is gone.

And if your health changed since you started? Good luck qualifying for new coverage.

Group insurance is a benefit. Personal insurance is a plan. Big difference.

DM me if you only have coverage through work — I'll tell you what to look for.

Watch video

Life insurance helps ensure your family can maintain their lifestyle, pay off debts and fund future goals even after you die. Simple, affordable coverage can make all the difference. Message me for a personalized coverage estimate. https://advisor.sunlife.ca/cristian.tonon

Life insurance helps ensure your family can maintain their lifestyle, pay off debts and fund future goals even after you die. Simple, affordable coverage can make all the difference. Message me for a personalized coverage estimate. https://advisor.sunlife.ca/cristian.tonon

Short‑, mid‑ and long‑term goals — consider organizing into a Sun Life One Plan so you can act with more confidence. Let’s get started on your #SunLifeOnePlan.

Message me for details. https://advisor.sunlife.ca/cristian.tonon

Message me for details. https://advisor.sunlife.ca/cristian.tonon

Short‑, mid‑ and long‑term goals — consider organizing into a Sun Life One Plan so you can act with more confidence. Let’s get started on your #SunLifeOnePlan.

Message me for details. https://advisor.sunlife.ca/cristian.tonon

Message me for details. https://advisor.sunlife.ca/cristian.tonon

Should You Trust a Robo-Advisor?

Robo-advisors charge less. They're easy to set up.

But when markets crash 20% and you're staring at your phone at 2 AM — can an algorithm talk you off the ledge?

A robo picks investments based on a questionnaire and rebalances automatically. That's it. No tax planning. No insurance review. No behavioral coaching.

A financial advisor builds a plan around your entire life — not just your portfolio. We're the person who tells you to stay invested when everyone else is selling.

If your finances are simple, a robo is fine. If your life is more complex — family, property, insurance, taxes — you need a human.

Which do you use? Comment below. Follow for honest money talk.

But when markets crash 20% and you're staring at your phone at 2 AM — can an algorithm talk you off the ledge?

A robo picks investments based on a questionnaire and rebalances automatically. That's it. No tax planning. No insurance review. No behavioral coaching.

A financial advisor builds a plan around your entire life — not just your portfolio. We're the person who tells you to stay invested when everyone else is selling.

If your finances are simple, a robo is fine. If your life is more complex — family, property, insurance, taxes — you need a human.

Which do you use? Comment below. Follow for honest money talk.

Watch video

Child Insurance Policies — Smart Planning or Unnecessary?

Should you buy life insurance for your kids?

Before you say no, here's what most people don't realize:

1️⃣ It locks in their insurability for life — even if they develop a health condition at 18 or 25

2️⃣ It builds cash value they can access as adults for school, a home, or starting a business

3️⃣ It's incredibly cheap when they're young

Think of it less like insurance and more like a financial gift that grows with them.

It's not for everyone. But if you're thinking long-term about your kids' financial future, it's worth knowing about.

Would you do this for your kids? Comment yes or no — I want to hear your take.

Before you say no, here's what most people don't realize:

1️⃣ It locks in their insurability for life — even if they develop a health condition at 18 or 25

2️⃣ It builds cash value they can access as adults for school, a home, or starting a business

3️⃣ It's incredibly cheap when they're young

Think of it less like insurance and more like a financial gift that grows with them.

It's not for everyone. But if you're thinking long-term about your kids' financial future, it's worth knowing about.

Would you do this for your kids? Comment yes or no — I want to hear your take.

Watch video

One Missing Form Could Cost Your Family Thousands

Your family could lose thousands of dollars from your investments because of one form you never filled out.

If you don't name beneficiaries on your RRSP, TFSA, and RRIF, the money doesn't automatically go to your spouse or kids. It gets sucked into your estate, goes through probate, and your family pays legal fees, delays, and higher taxes.

Naming a beneficiary takes 10 minutes. It means the money bypasses your estate and goes straight to your loved ones.

But life changes. Marriages, divorces, new kids — if your forms are outdated, the wrong person could get your money.

10 minutes of paperwork now saves your family months of stress later.

Save this. Share it with your partner. When's the last time you checked yours?

If you don't name beneficiaries on your RRSP, TFSA, and RRIF, the money doesn't automatically go to your spouse or kids. It gets sucked into your estate, goes through probate, and your family pays legal fees, delays, and higher taxes.

Naming a beneficiary takes 10 minutes. It means the money bypasses your estate and goes straight to your loved ones.

But life changes. Marriages, divorces, new kids — if your forms are outdated, the wrong person could get your money.

10 minutes of paperwork now saves your family months of stress later.

Save this. Share it with your partner. When's the last time you checked yours?

Watch video

The Insurance Most Canadians Forget About

$6,000 a month. That's what long-term care can cost in Canada. And most families don't plan for it until it's too late.

Critical illness insurance pays a lump sum on diagnosis — cancer, stroke, heart attack. Long-term care insurance covers the actual monthly costs when someone can't live independently.

Government programs won't cover this. Your savings probably won't either.

The families who handle this well? They planned for it before they needed to.

Save this for your parents. DM me if you want to know what coverage actually looks like.

Critical illness insurance pays a lump sum on diagnosis — cancer, stroke, heart attack. Long-term care insurance covers the actual monthly costs when someone can't live independently.

Government programs won't cover this. Your savings probably won't either.

The families who handle this well? They planned for it before they needed to.

Save this for your parents. DM me if you want to know what coverage actually looks like.

Watch video

The RRSP Withdrawal Trap To Avoid

You pull $50,000 out of your RRSP.

Only $25,000 hits your bank account.

Here's how that happens:

The bank withholds 30% immediately on anything over $15,000. That's $15,000 gone before you see it. Then at tax time, the full $50K gets added to your income — pushing you into a higher bracket.

The fix? Don't pull large amounts all at once. Spread withdrawals over multiple years. Convert to a RRIF strategically. Coordinate with your other income sources.

Your RRSP is your money. But the CRA gets their cut. The question is how much you let them take.

Save this before you make a withdrawal you regret. Share it with anyone sitting on a big RRSP.

Only $25,000 hits your bank account.

Here's how that happens:

The bank withholds 30% immediately on anything over $15,000. That's $15,000 gone before you see it. Then at tax time, the full $50K gets added to your income — pushing you into a higher bracket.

The fix? Don't pull large amounts all at once. Spread withdrawals over multiple years. Convert to a RRIF strategically. Coordinate with your other income sources.

Your RRSP is your money. But the CRA gets their cut. The question is how much you let them take.

Save this before you make a withdrawal you regret. Share it with anyone sitting on a big RRSP.

Watch video

You Can Be Denied Life Insurance...

Think you can get life insurance whenever you want?

Not always.

Pre-existing conditions like diabetes or heart disease can mean higher premiums or flat-out denial. Mental health history, certain medications, even your hobbies — skydiving, scuba diving, motorcycles — all factor in.

Smoking? Your rates could be 2-3x higher. Dangerous occupation? Same thing.

The window to lock in affordable coverage is when you're young and healthy. Once something changes, you can't go back.

Don't wait until you need it to find out you can't get it.

Save this. Share it with someone who's been putting it off.

Not always.

Pre-existing conditions like diabetes or heart disease can mean higher premiums or flat-out denial. Mental health history, certain medications, even your hobbies — skydiving, scuba diving, motorcycles — all factor in.

Smoking? Your rates could be 2-3x higher. Dangerous occupation? Same thing.

The window to lock in affordable coverage is when you're young and healthy. Once something changes, you can't go back.

Don't wait until you need it to find out you can't get it.

Save this. Share it with someone who's been putting it off.

Watch video

$500/mo to Invest — Here's Exactly Where It Goes

$500 a month. 6 accounts screaming for your money.

Here's the exact priority order:

1️⃣ Get your employer RRSP match — that's free money

2️⃣ If buying a first home, max the FHSA for the double tax benefit

3️⃣ Build your emergency fund in a TFSA for flexible, tax-free access

4️⃣ RRSP if you're in a higher bracket for the tax deduction

5️⃣ RESP if you have kids — government matches 20%

6️⃣ Fill up remaining TFSA room

The right order depends on your income, goals, and timeline. But having a priority list means your money works harder.

Comment your age and I'll tell you which account to prioritize first. Save this for reference.

Here's the exact priority order:

1️⃣ Get your employer RRSP match — that's free money

2️⃣ If buying a first home, max the FHSA for the double tax benefit

3️⃣ Build your emergency fund in a TFSA for flexible, tax-free access

4️⃣ RRSP if you're in a higher bracket for the tax deduction

5️⃣ RESP if you have kids — government matches 20%

6️⃣ Fill up remaining TFSA room

The right order depends on your income, goals, and timeline. But having a priority list means your money works harder.

Comment your age and I'll tell you which account to prioritize first. Save this for reference.

Watch video

Why 'Buy Term and Invest the Difference' Doesn't Always Work

"Buy term and invest the difference" sounds smart in theory... but fails for most people in reality.

Here's why: most people don't actually invest the difference — they spend it.

Plus, term insurance expires. If you still need coverage in your 60s or 70s, renewing becomes prohibitively expensive or unavailable.

There's no one-size-fits-all answer. Term, permanent, or a mix — it depends on your goals and discipline.

📅 Book an appointment to figure out what's right for you:

https://advisor.sunlife.ca/cristian.tonon/

FOLLOW me on IG 👉 @cristian.tonon.sunlife

Here's why: most people don't actually invest the difference — they spend it.

Plus, term insurance expires. If you still need coverage in your 60s or 70s, renewing becomes prohibitively expensive or unavailable.

There's no one-size-fits-all answer. Term, permanent, or a mix — it depends on your goals and discipline.

📅 Book an appointment to figure out what's right for you:

https://advisor.sunlife.ca/cristian.tonon/

FOLLOW me on IG 👉 @cristian.tonon.sunlife

Watch video

From health spending accounts to enhanced benefits, there are ways to cover what provincial plans don't — and sometimes save on taxes too. Let's explore what fits your needs and budget.

From health spending accounts to enhanced benefits, there are ways to cover what provincial plans don't — and sometimes save on taxes too. Let's explore what fits your needs and budget.

Tax season isn't just about filing — it's about planning ahead. From RRSP contributions to income splitting strategies, there are things you can do now to better position your finances for next year and beyond.

Get in touch to find out what strategies work best for you. https://advisor.sunlife.ca/cristian.tonon

Get in touch to find out what strategies work best for you. https://advisor.sunlife.ca/cristian.tonon

Tax season isn't just about filing — it's about planning ahead. From RRSP contributions to income splitting strategies, there are things you can do now to better position your finances for next year and beyond.

Get in touch to find out what strategies work best for you. https://advisor.sunlife.ca/cristian.tonon

Get in touch to find out what strategies work best for you. https://advisor.sunlife.ca/cristian.tonon

How Inflation Is Quietly Stealing Your Purchasing Power

Your money is losing value every single day — and most people don't even realize it.

If inflation runs at 3% but your savings account earns 1%, you're going backwards. $10,000 today will only buy what $7,400 buys in 10 years.

That's $2,600 in purchasing power... gone.

Cash has its place, but for long-term goals, you need growth that outpaces inflation.

Otherwise, you're falling behind without spending a dollar.

📅 Book an appointment to protect your money from inflation:

https://advisor.sunlife.ca/cristian.tonon/

FOLLOW me on IG 👉 @cristian.tonon.sunlife

If inflation runs at 3% but your savings account earns 1%, you're going backwards. $10,000 today will only buy what $7,400 buys in 10 years.

That's $2,600 in purchasing power... gone.

Cash has its place, but for long-term goals, you need growth that outpaces inflation.

Otherwise, you're falling behind without spending a dollar.

📅 Book an appointment to protect your money from inflation:

https://advisor.sunlife.ca/cristian.tonon/

FOLLOW me on IG 👉 @cristian.tonon.sunlife

Watch video

No, Your Investments Aren't 'Locked In' Forever

Myth: Once you invest, your money is locked up and you can't touch it.

Truth: Most investment accounts are liquid. You can access your money within a few business days if needed.

TFSAs, non-registered accounts, even RRSPs have withdrawal options (though RRSPs come with tax implications).

Understanding liquidity gives you the confidence to invest in the first place. Growth and flexibility aren't mutually exclusive.

📅 Book an appointment to find a strategy that gives you both:

https://advisor.sunlife.ca/cristian.tonon/

FOLLOW me on IG 👉 @cristian.tonon.sunlife

Truth: Most investment accounts are liquid. You can access your money within a few business days if needed.

TFSAs, non-registered accounts, even RRSPs have withdrawal options (though RRSPs come with tax implications).

Understanding liquidity gives you the confidence to invest in the first place. Growth and flexibility aren't mutually exclusive.

📅 Book an appointment to find a strategy that gives you both:

https://advisor.sunlife.ca/cristian.tonon/

FOLLOW me on IG 👉 @cristian.tonon.sunlife

Watch video

What to Do With Extra Money - The Priority Framework

Got a bonus, tax refund, or extra cash? Here's exactly what to do with it.

Most people either blow it or freeze up trying to decide.

But there's a priority order: emergency fund first, high-interest debt second, employer matching third, then TFSA/RRSP contributions, then long-term investing.

Following a framework takes the guesswork out and helps your money work harder for you.

📅 Book an appointment to create a clear plan for your money:

https://advisor.sunlife.ca/cristian.tonon/

FOLLOW me on IG 👉 @cristian.tonon.sunlife

Most people either blow it or freeze up trying to decide.

But there's a priority order: emergency fund first, high-interest debt second, employer matching third, then TFSA/RRSP contributions, then long-term investing.

Following a framework takes the guesswork out and helps your money work harder for you.

📅 Book an appointment to create a clear plan for your money:

https://advisor.sunlife.ca/cristian.tonon/

FOLLOW me on IG 👉 @cristian.tonon.sunlife

Watch video

How Ontario's Progressive Tax System Works

Think your entire income gets taxed at your top rate? Wrong.

Ontario's progressive tax system taxes your income in layers. Your first dollars are taxed low, the next chunk higher, and so on.

Only income above each threshold gets taxed at that rate.

Your effective rate is lower than your marginal rate. Understanding this = smarter money decisions.

📅 Book an appointment to optimize your tax strategy:

https://advisor.sunlife.ca/cristian.tonon

FOLLOW me on IG 👉 @cristian.tonon.sunlife

Ontario's progressive tax system taxes your income in layers. Your first dollars are taxed low, the next chunk higher, and so on.

Only income above each threshold gets taxed at that rate.

Your effective rate is lower than your marginal rate. Understanding this = smarter money decisions.

📅 Book an appointment to optimize your tax strategy:

https://advisor.sunlife.ca/cristian.tonon

FOLLOW me on IG 👉 @cristian.tonon.sunlife

Watch video

Feeling the winter blahs? You're not alone. There’s still time to prioritize your mental wellbeing this winter. Many Sun Life plans offer coverage for mental health services. Let's discuss how your insurance can support you.

Feeling the winter blahs? You're not alone. There’s still time to prioritize your mental wellbeing this winter. Many Sun Life plans offer coverage for mental health services. Let's discuss how your insurance can support you.

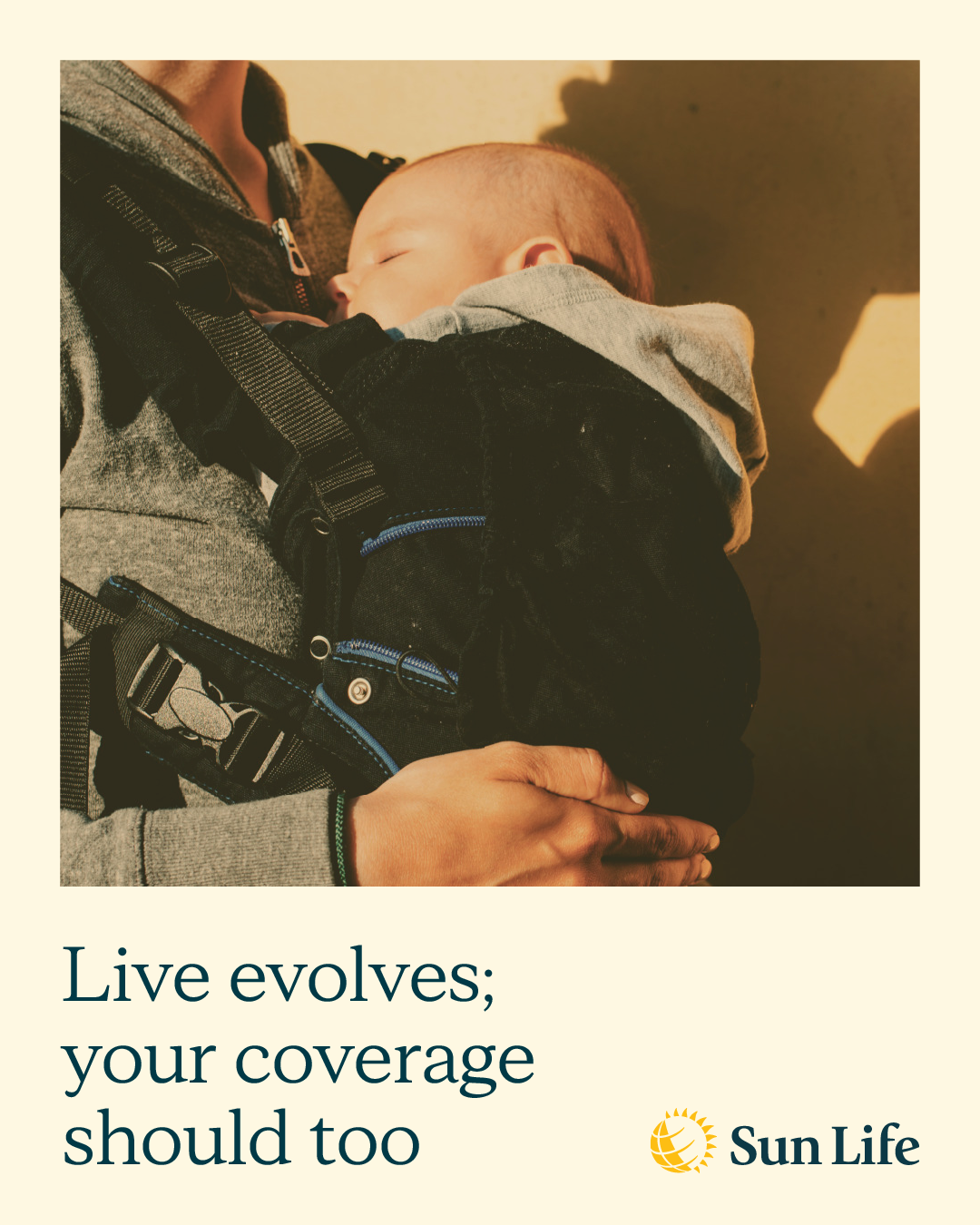

Navigating life insurance options can be overwhelming. Whether finishing school, buying a first home or starting a family, finding the right plan that fits life's unique journey is essential.

We can help secure your future together. Let us know how we can help.

We can help secure your future together. Let us know how we can help.

Navigating life insurance options can be overwhelming. Whether finishing school, buying a first home or starting a family, finding the right plan that fits life's unique journey is essential.

We can help secure your future together. Let us know how we can help.

We can help secure your future together. Let us know how we can help.

The Financial Checklist for Couples Moving In Together

Moving in with your partner? Before you split the rent, you need to have the money talk.

How will you split expenses? Are your beneficiaries updated? Do you know each other's debts and financial goals? Joint accounts or separate?

Getting on the same page financially doesn't kill the romance — it protects it. When money stress is off the table, your relationship gets stronger.

📅 Book an appointment to navigate the money conversation together:

https://advisor.sunlife.ca/cristian.tonon/

FOLLOW me on IG 👉 @cristian.tonon.sunlife

How will you split expenses? Are your beneficiaries updated? Do you know each other's debts and financial goals? Joint accounts or separate?

Getting on the same page financially doesn't kill the romance — it protects it. When money stress is off the table, your relationship gets stronger.

📅 Book an appointment to navigate the money conversation together:

https://advisor.sunlife.ca/cristian.tonon/

FOLLOW me on IG 👉 @cristian.tonon.sunlife

Watch video

Have questions?

Here to help answer your questions, provide clarity about products and get you started on the road to achieving your goals.

We are contracted with Sun Life Financial Distributors (Canada) Inc., a member of the Sun Life group of companies. Mutual funds distributed by Sun Life Financial Investment Services (Canada) Inc.