Keep up-to-date

Keep up to date with what’s going on. You can browse timely and relevant posts that might be helpful to you. Check back regularly to see what’s new.

Health challenges can strike anyone. Critical illness insurance provides financial support when you need it most — helping you focus on recovery instead of financial stress. Whether you're supporting a loved one or managing personal expenses, having protection in place is invaluable. Let's talk! https://advisor.sunlife.ca/cristian.tonon

Health challenges can strike anyone. Critical illness insurance provides financial support when you need it most — helping you focus on recovery instead of financial stress. Whether you're supporting a loved one or managing personal expenses, having protection in place is invaluable. Let's talk! https://advisor.sunlife.ca/cristian.tonon

Disability can impact more than just your income — it can affect your financial priorities all at once. The right coverage can help create breathing room if you’re unable to work due to illness or injury. If your paycheque fuels your plans, they may be worth protecting. Get in touch to talk about your options. https://advisor.sunlife.ca/cristian.tonon

Disability can impact more than just your income — it can affect your financial priorities all at once. The right coverage can help create breathing room if you’re unable to work due to illness or injury. If your paycheque fuels your plans, they may be worth protecting. Get in touch to talk about your options. https://advisor.sunlife.ca/cristian.tonon

A growing family is exciting — and it changes everything from monthly cash flow to longer-term goals. Childcare, activities, housing, education… it adds up fast. A realistic plan can help you balance today’s costs while still making progress on what matters most.

A growing family is exciting — and it changes everything from monthly cash flow to longer-term goals. Childcare, activities, housing, education… it adds up fast. A realistic plan can help you balance today’s costs while still making progress on what matters most.

Your mortgage is likely one of your biggest financial commitments. What happens to it if something unexpected occurs? Mortgage protection insurance helps ensure your family can keep your home secure, no matter what life brings. Let's review your coverage and give you peace of mind. Reach out to discuss your options today.

https://advisor.sunlife.ca/cristian.tonon

https://advisor.sunlife.ca/cristian.tonon

Your mortgage is likely one of your biggest financial commitments. What happens to it if something unexpected occurs? Mortgage protection insurance helps ensure your family can keep your home secure, no matter what life brings. Let's review your coverage and give you peace of mind. Reach out to discuss your options today.

https://advisor.sunlife.ca/cristian.tonon

https://advisor.sunlife.ca/cristian.tonon

Congratulations on graduating! Now comes the next chapter, managing student debt while building your future. From repayment strategies to integrating loans into your financial roadmap, let's make sure you're set up for success. Whether it's buying a first home or saving for further education, we can help you navigate it all. Let's talk!

Congratulations on graduating! Now comes the next chapter, managing student debt while building your future. From repayment strategies to integrating loans into your financial roadmap, let's make sure you're set up for success. Whether it's buying a first home or saving for further education, we can help you navigate it all. Let's talk!

Why choose between protection and savings when you can have both? Bundle term and permanent life insurance to save 10% for life on your permanent policy, AND get money back on critical illness coverage.

Build complete protection for multiple life scenarios while maximizing your savings. Let's talk about your protection needs!

Build complete protection for multiple life scenarios while maximizing your savings. Let's talk about your protection needs!

Why choose between protection and savings when you can have both? Bundle term and permanent life insurance to save 10% for life on your permanent policy, AND get money back on critical illness coverage.

Build complete protection for multiple life scenarios while maximizing your savings. Let's talk about your protection needs!

Build complete protection for multiple life scenarios while maximizing your savings. Let's talk about your protection needs!

You're building your future – let's help make sure it's protected.

Whether you're planning for your growing family or thinking about what you'll leave behind, our current offers make comprehensive coverage more affordable. Get 10% off permanent insurance when bundled with term insurance, and cash back on critical illness protection. Real savings for real life. Let’s chat! Offer ends July 31.

Whether you're planning for your growing family or thinking about what you'll leave behind, our current offers make comprehensive coverage more affordable. Get 10% off permanent insurance when bundled with term insurance, and cash back on critical illness protection. Real savings for real life. Let’s chat! Offer ends July 31.

You're building your future – let's help make sure it's protected.

Whether you're planning for your growing family or thinking about what you'll leave behind, our current offers make comprehensive coverage more affordable. Get 10% off permanent insurance when bundled with term insurance, and cash back on critical illness protection. Real savings for real life. Let’s chat! Offer ends July 31.

Whether you're planning for your growing family or thinking about what you'll leave behind, our current offers make comprehensive coverage more affordable. Get 10% off permanent insurance when bundled with term insurance, and cash back on critical illness protection. Real savings for real life. Let’s chat! Offer ends July 31.

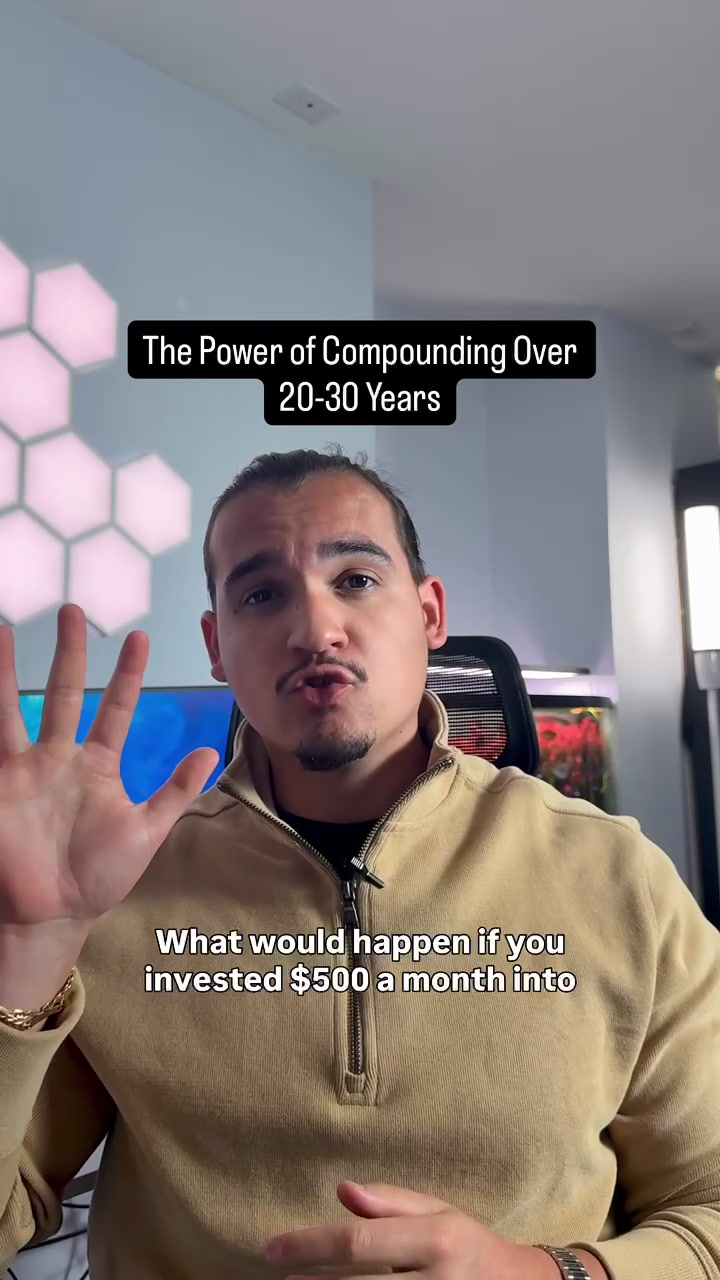

The Power of Compounding in Your TFSA Over 20-30 Years

[Disclaimer: The amounts and rates are for sample/presentation purposes only]

Invest $500/month in your TFSA at 6% average annual return.

After 20 years: ~$230,000

After 30 years: Over $500,000

You only contributed $180,000. The rest? Tax-free growth.

No taxes on dividends, capital gains, or withdrawals. Ever.

Time and consistency are how you build real wealth in a TFSA.

📅 Book an appointment to maximize your TFSA strategy: 👉 https://advisor.sunlife.ca/cristian.tonon/

FOLLOW me on IG 👉 @cristian.tonon.sunlife

Invest $500/month in your TFSA at 6% average annual return.

After 20 years: ~$230,000

After 30 years: Over $500,000

You only contributed $180,000. The rest? Tax-free growth.

No taxes on dividends, capital gains, or withdrawals. Ever.

Time and consistency are how you build real wealth in a TFSA.

📅 Book an appointment to maximize your TFSA strategy: 👉 https://advisor.sunlife.ca/cristian.tonon/

FOLLOW me on IG 👉 @cristian.tonon.sunlife

Watch video

Why Your Work Disability Coverage Probably Isn’t Enough

[This data is for presentation purposes only, the information is illustrative rather than definitive]

Your group disability plan covers 60% of your income. After taxes, that might be 40-50% of your actual take-home pay.

Can you cover your mortgage, bills, and lifestyle on half your income?

Personal disability insurance tops up your group coverage, is portable if you change jobs, and pays tax-free benefits if you pay the premiums yourself.

Your income is your most valuable asset — protect it properly.

📅 Book an appointment to review your disability coverage: 👉 https://advisor.sunlife.ca/cristian.tonon/

FOLLOW me on IG 👉 @cristian.tonon.sunlife

Your group disability plan covers 60% of your income. After taxes, that might be 40-50% of your actual take-home pay.

Can you cover your mortgage, bills, and lifestyle on half your income?

Personal disability insurance tops up your group coverage, is portable if you change jobs, and pays tax-free benefits if you pay the premiums yourself.

Your income is your most valuable asset — protect it properly.

📅 Book an appointment to review your disability coverage: 👉 https://advisor.sunlife.ca/cristian.tonon/

FOLLOW me on IG 👉 @cristian.tonon.sunlife

Watch video

Planning that dream summer getaway? Travel insurance is your safety net. From medical emergencies to trip cancellations, the right coverage means you can explore the world with confidence. Don't let unexpected costs derail your plans. You want to be protected for every adventure. What's your next destination?

Planning that dream summer getaway? Travel insurance is your safety net. From medical emergencies to trip cancellations, the right coverage means you can explore the world with confidence. Don't let unexpected costs derail your plans. You want to be protected for every adventure. What's your next destination?

Growing your family is exciting but can also be expensive. Balancing today's costs (childcare, diapers, activities) with tomorrow's goals (education, home, experiences) takes planning. Let's build a family cash-flow roadmap that helps you save without sacrificing the moments that matter. Ready to create a strategy that works for your family? Get in touch. https://advisor.sunlife.ca/cristian.tonon

Growing your family is exciting but can also be expensive. Balancing today's costs (childcare, diapers, activities) with tomorrow's goals (education, home, experiences) takes planning. Let's build a family cash-flow roadmap that helps you save without sacrificing the moments that matter. Ready to create a strategy that works for your family? Get in touch. https://advisor.sunlife.ca/cristian.tonon

Paying Off Debt vs Investing?

Extra money in your account. Should it be put towards paying off debt or should it be invested?

Often, the best approach is a balance — pay down some debt while investing some.

📅 Book an appointment to figure out the right strategy for you: 👉 https://advisor.sunlife.ca/cristian.tonon/

FOLLOW me on IG 👉 @cristian.tonon.sunlife

Often, the best approach is a balance — pay down some debt while investing some.

📅 Book an appointment to figure out the right strategy for you: 👉 https://advisor.sunlife.ca/cristian.tonon/

FOLLOW me on IG 👉 @cristian.tonon.sunlife

Watch video

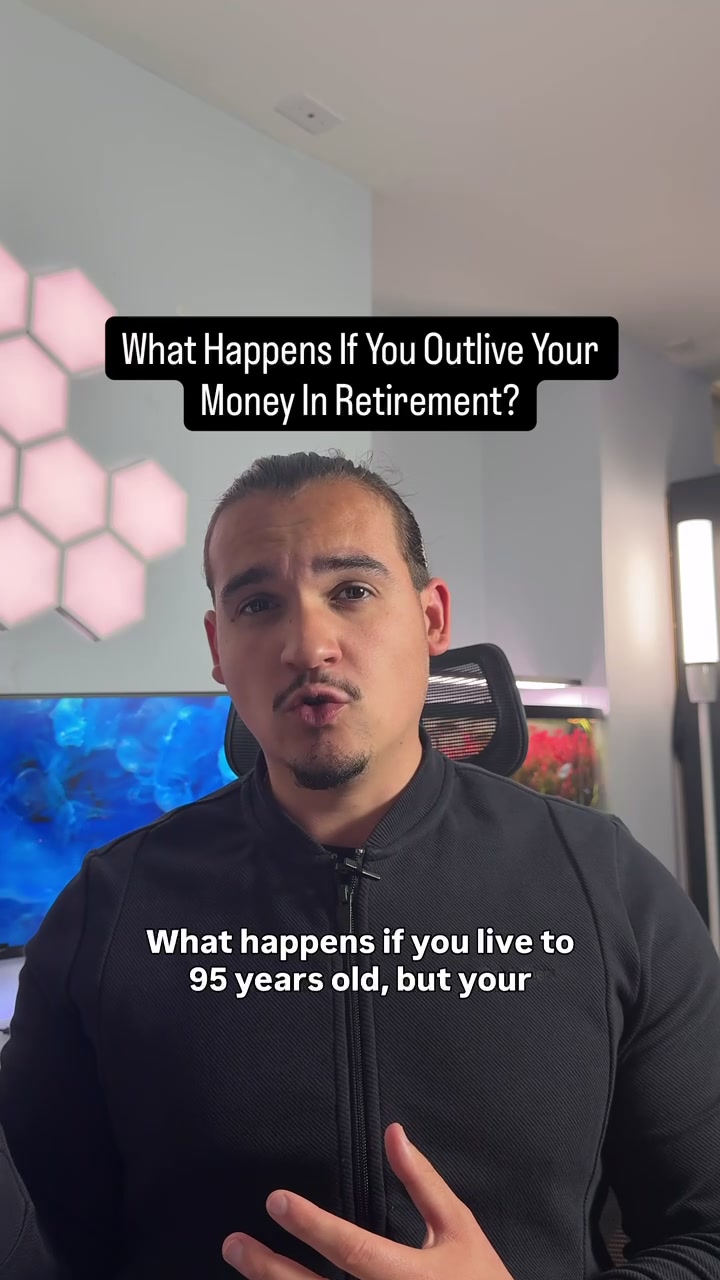

What Happens If You Outlive Your Money in Retirement?

What if you live to 95… but your money only lasts until 80?

Longevity risk is real. Canadians are living longer, which means retirement savings need to stretch 25-30 years or more.

Running out of money in your 80s is scarier than most financial risks because you can’t go back to work.

You need a sustainable withdrawal strategy, a diversified portfolio that keeps growing, and potentially guaranteed income sources to fill the gaps.

📅 Book an appointment to build a retirement plan that lasts as long as you do: 👉 https://advisor.sunlife.ca/cristian.tonon/

FOLLOW me on IG 👉 @cristian.tonon.sunlife

Longevity risk is real. Canadians are living longer, which means retirement savings need to stretch 25-30 years or more.

Running out of money in your 80s is scarier than most financial risks because you can’t go back to work.

You need a sustainable withdrawal strategy, a diversified portfolio that keeps growing, and potentially guaranteed income sources to fill the gaps.

📅 Book an appointment to build a retirement plan that lasts as long as you do: 👉 https://advisor.sunlife.ca/cristian.tonon/

FOLLOW me on IG 👉 @cristian.tonon.sunlife

Watch video

Your leisure goals matter just as much as your long-term plans. Whether it's a dream vacation or a weekend getaway, let's build a savings strategy that lets you enjoy life now while securing your future. Small contributions can add up fast. Let’s chat about options that work for you. https://advisor.sunlife.ca/cristian.tonon

Your leisure goals matter just as much as your long-term plans. Whether it's a dream vacation or a weekend getaway, let's build a savings strategy that lets you enjoy life now while securing your future. Small contributions can add up fast. Let’s chat about options that work for you. https://advisor.sunlife.ca/cristian.tonon

Using Whole Life Insurance to Offset Future Tax Liabilities

When you die, your RRSP is taxed as income at the highest rate.

If you have a large RRSP, your estate could owe hundreds of thousands in taxes before anything goes to your beneficiaries.

Whole life insurance pays a tax-free death benefit that can cover that tax bill.

Your family gets the full estate without liquidating assets or paying out of pocket.

It’s not just about replacing income — it’s about protecting wealth transfer.

📅 Book an appointment to explore estate tax strategies: 👉 https://advisor.sunlife.ca/cristian.tonon/

FOLLOW me on IG 👉 @cristian.tonon.sunlife

If you have a large RRSP, your estate could owe hundreds of thousands in taxes before anything goes to your beneficiaries.

Whole life insurance pays a tax-free death benefit that can cover that tax bill.

Your family gets the full estate without liquidating assets or paying out of pocket.

It’s not just about replacing income — it’s about protecting wealth transfer.

📅 Book an appointment to explore estate tax strategies: 👉 https://advisor.sunlife.ca/cristian.tonon/

FOLLOW me on IG 👉 @cristian.tonon.sunlife

Watch video

Changing jobs or wrapping up your career? It's the perfect time to review your investments and benefits. Let's talk about transitioning your group investments smoothly and planning your next chapter. Whether it's consolidating accounts or adjusting your strategy, we're here to help.

https://www.sunlife.ca/en/choices/leaving-group-investments/

#CareerTransition #InvestmentPlanning

https://www.sunlife.ca/en/choices/leaving-group-investments/

#CareerTransition #InvestmentPlanning

Help make money discussions in your family normal. Simple conversations can help build strong habits. Get in touch for age-appropriate tips for your kid(s). Ask for our family finance checklist.

#FamilyFinances #FinancialLiteracy

#FamilyFinances #FinancialLiteracy

Help make money discussions in your family normal. Simple conversations can help build strong habits. Get in touch for age-appropriate tips for your kid(s). Ask for our family finance checklist.

#FamilyFinances #FinancialLiteracy

#FamilyFinances #FinancialLiteracy

Your Life Insurance Disappeared and You Don't Know It

You just left your job. Your paycheque stopped.

But so did something else you probably forgot about — your life insurance.

Most people have 1-2x their salary in group life coverage through work. Feels like enough, so they never think about it. But the second you leave, the coverage is gone.

And if your health changed since you started? Good luck qualifying for new coverage.

Group insurance is a benefit. Personal insurance is a plan. Big difference.

DM me if you only have coverage through work — I'll tell you what to look for.

But so did something else you probably forgot about — your life insurance.

Most people have 1-2x their salary in group life coverage through work. Feels like enough, so they never think about it. But the second you leave, the coverage is gone.

And if your health changed since you started? Good luck qualifying for new coverage.

Group insurance is a benefit. Personal insurance is a plan. Big difference.

DM me if you only have coverage through work — I'll tell you what to look for.

Watch video

Life insurance helps ensure your family can maintain their lifestyle, pay off debts and fund future goals even after you die. Simple, affordable coverage can make all the difference. Message me for a personalized coverage estimate. https://advisor.sunlife.ca/cristian.tonon

Life insurance helps ensure your family can maintain their lifestyle, pay off debts and fund future goals even after you die. Simple, affordable coverage can make all the difference. Message me for a personalized coverage estimate. https://advisor.sunlife.ca/cristian.tonon

Short‑, mid‑ and long‑term goals — consider organizing into a Sun Life One Plan so you can act with more confidence. Let’s get started on your #SunLifeOnePlan.

Message me for details. https://advisor.sunlife.ca/cristian.tonon

Message me for details. https://advisor.sunlife.ca/cristian.tonon

Short‑, mid‑ and long‑term goals — consider organizing into a Sun Life One Plan so you can act with more confidence. Let’s get started on your #SunLifeOnePlan.

Message me for details. https://advisor.sunlife.ca/cristian.tonon

Message me for details. https://advisor.sunlife.ca/cristian.tonon

Have questions?

Here to help answer your questions, provide clarity about products and get you started on the road to achieving your goals.

We are contracted with Sun Life Financial Distributors (Canada) Inc., a member of the Sun Life group of companies. Mutual funds distributed by Sun Life Financial Investment Services (Canada) Inc.