Stay informed

Stay informed with what’s going on. Browse posts that might be helpful to you or check out an event happening in your area. Come back regularly as this page is kept up-to-date with a lot of relevant information.

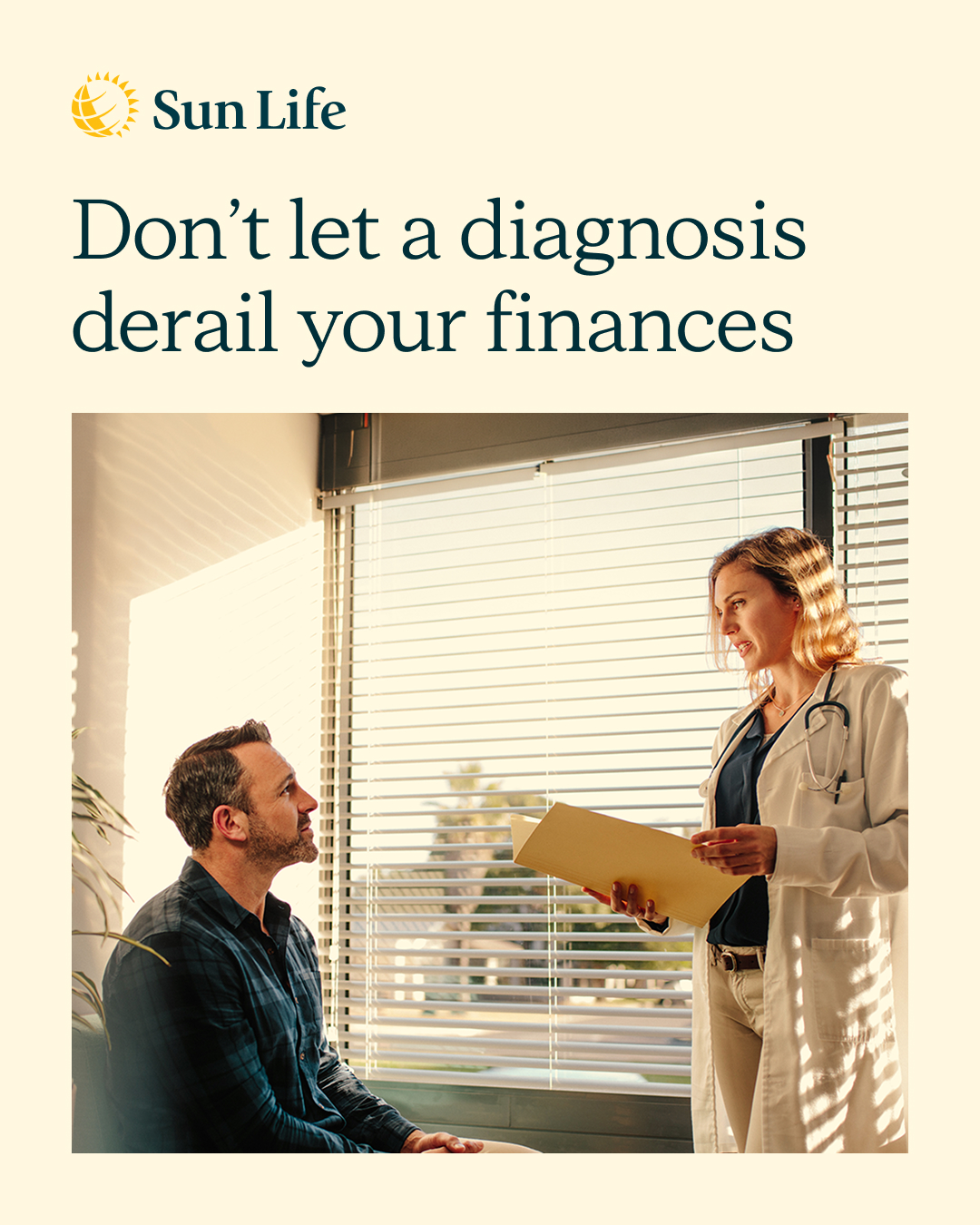

A serious illness can impact more than your health, it can disrupt your income, savings and long-term goals. Critical illness insurance pays a lump sum benefit upon diagnosis of covered conditions like cancer, heart attack or stroke, so you have financial support when it matters most. Let’s talk about how critical illness coverage can protect your financial plan before you need it. https://advisor.sunlife.ca/jane.mcmillan/

A serious illness can impact more than your health, it can disrupt your income, savings and long-term goals. Critical illness insurance pays a lump sum benefit upon diagnosis of covered conditions like cancer, heart attack or stroke, so you have financial support when it matters most. Let’s talk about how critical illness coverage can protect your financial plan before you need it. https://advisor.sunlife.ca/jane.mcmillan/

It's never too early to start. When kids learn about money young, they make smarter choices later. 💡

Here's how to get started:

• Give them an allowance and let them decide how to spend it

• Talk openly about budgeting and saving

• Show them how saving reaches big goals 🎯

• Make learning fun and age-appropriate

Small money conversations today build confident adults tomorrow.

Ready to help your kids build money confidence? Reach out and let's talk about it. https://advisor.sunlife.ca/jane.mcmillan/

Here's how to get started:

• Give them an allowance and let them decide how to spend it

• Talk openly about budgeting and saving

• Show them how saving reaches big goals 🎯

• Make learning fun and age-appropriate

Small money conversations today build confident adults tomorrow.

Ready to help your kids build money confidence? Reach out and let's talk about it. https://advisor.sunlife.ca/jane.mcmillan/

It's never too early to start. When kids learn about money young, they make smarter choices later. 💡

Here's how to get started:

• Give them an allowance and let them decide how to spend it

• Talk openly about budgeting and saving

• Show them how saving reaches big goals 🎯

• Make learning fun and age-appropriate

Small money conversations today build confident adults tomorrow.

Ready to help your kids build money confidence? Reach out and let's talk about it. https://advisor.sunlife.ca/jane.mcmillan/

Here's how to get started:

• Give them an allowance and let them decide how to spend it

• Talk openly about budgeting and saving

• Show them how saving reaches big goals 🎯

• Make learning fun and age-appropriate

Small money conversations today build confident adults tomorrow.

Ready to help your kids build money confidence? Reach out and let's talk about it. https://advisor.sunlife.ca/jane.mcmillan/

Estate planning isn't just about money, it's about legacy. Have you thought about how your assets will be managed and distributed? Let's create a strategy that reflects your values and protects what matters most.

Ready to get started? Reach out to discuss your estate plan today. https://advisor.sunlife.ca/jane.mcmillan/

Ready to get started? Reach out to discuss your estate plan today. https://advisor.sunlife.ca/jane.mcmillan/

Estate planning isn't just about money, it's about legacy. Have you thought about how your assets will be managed and distributed? Let's create a strategy that reflects your values and protects what matters most.

Ready to get started? Reach out to discuss your estate plan today. https://advisor.sunlife.ca/jane.mcmillan/

Ready to get started? Reach out to discuss your estate plan today. https://advisor.sunlife.ca/jane.mcmillan/

無論您是自僱人士、正處於工作轉換期,還是沒有公司提供的福利,保障上的缺口可能會讓您暴露於風險。

個人健康保險和危疾保障有助於填補這些缺口,並在突發狀況下守護您的財務穩健。

讓我們商討適合您的策略。

個人健康保險和危疾保障有助於填補這些缺口,並在突發狀況下守護您的財務穩健。

讓我們商討適合您的策略。

無論您是自僱人士、正處於工作轉換期,還是沒有公司提供的福利,保障上的缺口可能會讓您暴露於風險。

個人健康保險和危疾保障有助於填補這些缺口,並在突發狀況下守護您的財務穩健。

讓我們商討適合您的策略。

個人健康保險和危疾保障有助於填補這些缺口,並在突發狀況下守護您的財務穩健。

讓我們商討適合您的策略。

如果您是自由职业者、正处于职业过渡期,或暂时没有公司提供的福利,保障缺口可能会让您暴露在风险之中。

个人健康保险与重疾险可以帮您填补这些缺口,在意外来临时守护您的财务安全。

我们可以一起探讨适合您的保障方案。

个人健康保险与重疾险可以帮您填补这些缺口,在意外来临时守护您的财务安全。

我们可以一起探讨适合您的保障方案。

如果您是自由职业者、正处于职业过渡期,或暂时没有公司提供的福利,保障缺口可能会让您暴露在风险之中。

个人健康保险与重疾险可以帮您填补这些缺口,在意外来临时守护您的财务安全。

我们可以一起探讨适合您的保障方案。

个人健康保险与重疾险可以帮您填补这些缺口,在意外来临时守护您的财务安全。

我们可以一起探讨适合您的保障方案。

Your investments should do more than grow — they should support where you’re headed. A well-balanced strategy can help align your money with your goals as they evolve. Let’s build an investment approach designed around you. https://advisor.sunlife.ca/jane.mcmillan/

Your investments should do more than grow — they should support where you’re headed. A well-balanced strategy can help align your money with your goals as they evolve. Let’s build an investment approach designed around you. https://advisor.sunlife.ca/jane.mcmillan/

Thinking it's time to upgrade your investment strategy? I'd love to walk you through how Elevate Portfolio Program could support your financial goals. Every portfolio journey is unique, and I'm here to help you find the right approach.

Reach out to schedule a quick conversation! https://advisor.sunlife.ca/jane.mcmillan/

Reach out to schedule a quick conversation! https://advisor.sunlife.ca/jane.mcmillan/

Thinking it's time to upgrade your investment strategy? I'd love to walk you through how Elevate Portfolio Program could support your financial goals. Every portfolio journey is unique, and I'm here to help you find the right approach.

Reach out to schedule a quick conversation! https://advisor.sunlife.ca/jane.mcmillan/

Reach out to schedule a quick conversation! https://advisor.sunlife.ca/jane.mcmillan/

Running a business today often means managing rising costs, tighter margins and constant pressure on cash flow. A clear financial approach can help you stay in control, manage expenses, protect against risk and keep your business moving forward.

Let’s review your strategy to find ways to strengthen your margins.https://advisor.sunlife.ca/jane.mcmillan/

Let’s review your strategy to find ways to strengthen your margins.https://advisor.sunlife.ca/jane.mcmillan/

Running a business today often means managing rising costs, tighter margins and constant pressure on cash flow. A clear financial approach can help you stay in control, manage expenses, protect against risk and keep your business moving forward.

Let’s review your strategy to find ways to strengthen your margins.https://advisor.sunlife.ca/jane.mcmillan/

Let’s review your strategy to find ways to strengthen your margins.https://advisor.sunlife.ca/jane.mcmillan/

Buying a home, growing your family, building your career — there’s a lot to balance. Creating a personalized financial roadmap early can help you stay on track while still living for today. Small steps today can make a meaningful difference over time. Get in touch to discuss options that will work best for you. https://advisor.sunlife.ca/jane.mcmillan/

Buying a home, growing your family, building your career — there’s a lot to balance. Creating a personalized financial roadmap early can help you stay on track while still living for today. Small steps today can make a meaningful difference over time. Get in touch to discuss options that will work best for you. https://advisor.sunlife.ca/jane.mcmillan/

You’ve built significant wealth. Now it’s about making it last. With the right approach, you can help reduce tax impacts, protect your estate and create a legacy that supports the people and causes you care about. Let’s build a strategy that helps you move into retirement with clarity and confidence. Book a conversation to start shaping your legacy. https://advisor.sunlife.ca/jane.mcmillan/

You’ve built significant wealth. Now it’s about making it last. With the right approach, you can help reduce tax impacts, protect your estate and create a legacy that supports the people and causes you care about. Let’s build a strategy that helps you move into retirement with clarity and confidence. Book a conversation to start shaping your legacy. https://advisor.sunlife.ca/jane.mcmillan/

Not all investors are the same — so why should all portfolios be? The Elevate Portfolio Program comes with options to match your risk comfort level and timeline.

Let's find the portfolio that aligns with your vision for the future. https://advisor.sunlife.ca/jane.mcmillan/

Let's find the portfolio that aligns with your vision for the future. https://advisor.sunlife.ca/jane.mcmillan/

Not all investors are the same — so why should all portfolios be? The Elevate Portfolio Program comes with options to match your risk comfort level and timeline.

Let's find the portfolio that aligns with your vision for the future. https://advisor.sunlife.ca/jane.mcmillan/

Let's find the portfolio that aligns with your vision for the future. https://advisor.sunlife.ca/jane.mcmillan/

Life can be unpredictable. The right protection can help you stay financially secure when it matters most. Insurance can play a key role in supporting your overall financial approach. Let’s review your coverage and make sure it fits your needs. https://advisor.sunlife.ca/jane.mcmillan/

Life can be unpredictable. The right protection can help you stay financially secure when it matters most. Insurance can play a key role in supporting your overall financial approach. Let’s review your coverage and make sure it fits your needs. https://advisor.sunlife.ca/jane.mcmillan/

Avec un parcours financier bien structuré, vous vous assurez que votre patrimoine soutiendra les personnes et les causes qui vous tiennent à cœur, d’une génération à l’autre.

Ensemble, façonnons un héritage qui reflète votre vision grâce à Un Plan, simplement Sun Life. Communiquez avec nous pour commencer. https://conseiller.sunlife.ca/f/jane.mcmillan

#UnPlanSimplementSunLife #SunLife

Ensemble, façonnons un héritage qui reflète votre vision grâce à Un Plan, simplement Sun Life. Communiquez avec nous pour commencer. https://conseiller.sunlife.ca/f/jane.mcmillan

#UnPlanSimplementSunLife #SunLife

Avec un parcours financier bien structuré, vous vous assurez que votre patrimoine soutiendra les personnes et les causes qui vous tiennent à cœur, d’une génération à l’autre.

Ensemble, façonnons un héritage qui reflète votre vision grâce à Un Plan, simplement Sun Life. Communiquez avec nous pour commencer. https://conseiller.sunlife.ca/f/jane.mcmillan

#UnPlanSimplementSunLife #SunLife

Ensemble, façonnons un héritage qui reflète votre vision grâce à Un Plan, simplement Sun Life. Communiquez avec nous pour commencer. https://conseiller.sunlife.ca/f/jane.mcmillan

#UnPlanSimplementSunLife #SunLife

Retirement isn’t an end. It’s your next chapter.

Retirement looks different for everyone. Whether you’re planning to slow down, travel, or explore new passions, having a thoughtful strategy can help you get there with confidence. Explore ways to transition your savings into income that supports the lifestyle you envision. Let’s build a strategy that helps you move into retirement with clarity and confidence.

Watch video

You’ve worked hard to build your business, but without clear next steps, transitions could put it at risk.

A clear succession strategy can help protect your business, support your team, and create a smoother path forward. Book a quick chat to discuss your next steps. https://advisor.sunlife.ca/jane.mcmillan/

A clear succession strategy can help protect your business, support your team, and create a smoother path forward. Book a quick chat to discuss your next steps. https://advisor.sunlife.ca/jane.mcmillan/

You’ve worked hard to build your business, but without clear next steps, transitions could put it at risk.

A clear succession strategy can help protect your business, support your team, and create a smoother path forward. Book a quick chat to discuss your next steps. https://advisor.sunlife.ca/jane.mcmillan/

A clear succession strategy can help protect your business, support your team, and create a smoother path forward. Book a quick chat to discuss your next steps. https://advisor.sunlife.ca/jane.mcmillan/

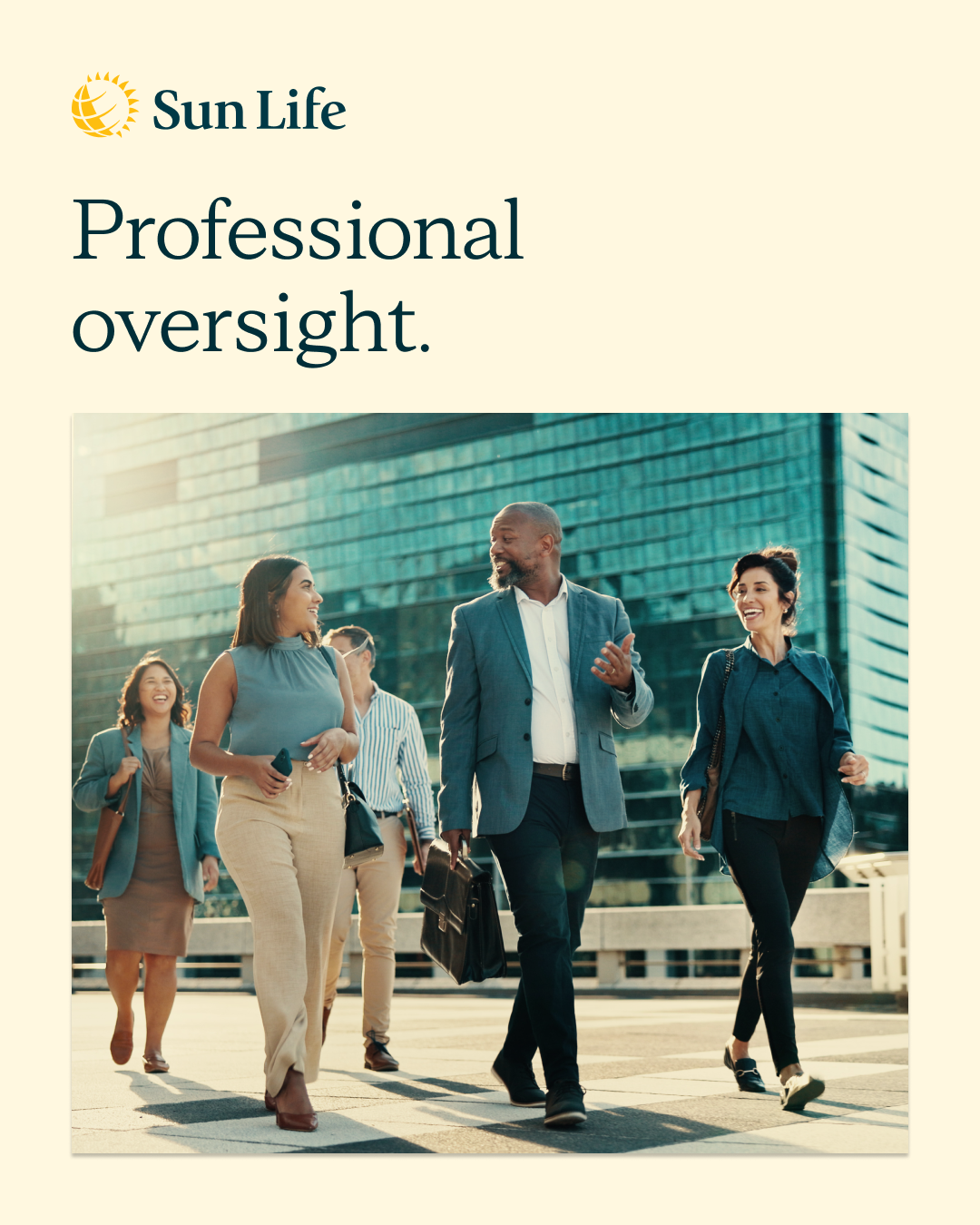

Your portfolio deserves professional attention. The Elevate Portfolio Program features carefully selected funds from leading asset managers.

Want to learn how this can benefit your portfolio? Reach out! https://advisor.sunlife.ca/jane.mcmillan/

Want to learn how this can benefit your portfolio? Reach out! https://advisor.sunlife.ca/jane.mcmillan/

Your portfolio deserves professional attention. The Elevate Portfolio Program features carefully selected funds from leading asset managers.

Want to learn how this can benefit your portfolio? Reach out! https://advisor.sunlife.ca/jane.mcmillan/

Want to learn how this can benefit your portfolio? Reach out! https://advisor.sunlife.ca/jane.mcmillan/

Health events can happen without warning — and the costs aren’t always medical. Critical illness insurance can provide financial support during a serious diagnosis, helping with time off work, travel for care, or everyday expenses so you can focus on recovery. Want to explore if it fits your plan? https://advisor.sunlife.ca/jane.mcmillan/

Health events can happen without warning — and the costs aren’t always medical. Critical illness insurance can provide financial support during a serious diagnosis, helping with time off work, travel for care, or everyday expenses so you can focus on recovery. Want to explore if it fits your plan? https://advisor.sunlife.ca/jane.mcmillan/

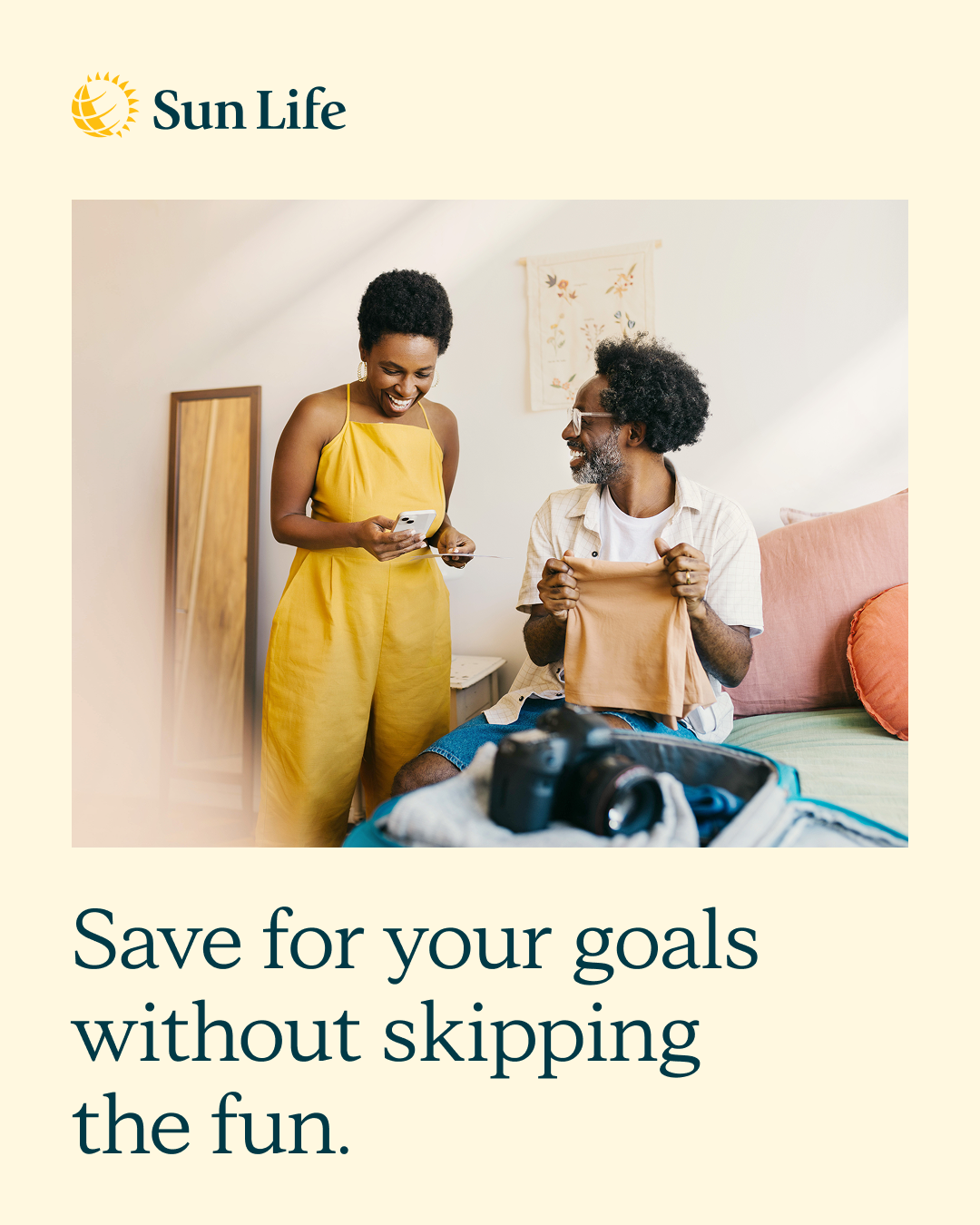

Saving for your goals shouldn’t mean skipping the fun. Whether you’re planning travel, a wedding, a big experience or your next “chapter,” the right strategy can help you set aside cash intentionally while still staying on track. Let's transform your priorities into a financial roadmap you can commit to. https://advisor.sunlife.ca/jane.mcmillan/

Saving for your goals shouldn’t mean skipping the fun. Whether you’re planning travel, a wedding, a big experience or your next “chapter,” the right strategy can help you set aside cash intentionally while still staying on track. Let's transform your priorities into a financial roadmap you can commit to. https://advisor.sunlife.ca/jane.mcmillan/

Greater wealth can bring greater complexity. From tax-aware approaches to estate considerations, having a thoughtful plan in place can help you protect and preserve what matters most — today and for the future. Let’s help simplify your next steps with a personalized roadmap. https://advisor.sunlife.ca/jane.mcmillan/

Greater wealth can bring greater complexity. From tax-aware approaches to estate considerations, having a thoughtful plan in place can help you protect and preserve what matters most — today and for the future. Let’s help simplify your next steps with a personalized roadmap. https://advisor.sunlife.ca/jane.mcmillan/

Here's the thing: lower fees can mean more of your money stays invested and working harder for you. The Elevate Portfolio Program offers transparent, competitive pricing that can benefit your returns.

Curious how much you could save? Let's talk! https://advisor.sunlife.ca/jane.mcmillan/

Curious how much you could save? Let's talk! https://advisor.sunlife.ca/jane.mcmillan/

Here's the thing: lower fees can mean more of your money stays invested and working harder for you. The Elevate Portfolio Program offers transparent, competitive pricing that can benefit your returns.

Curious how much you could save? Let's talk! https://advisor.sunlife.ca/jane.mcmillan/

Curious how much you could save? Let's talk! https://advisor.sunlife.ca/jane.mcmillan/

Have questions?

Here to help answer your questions, provide clarity about products and get you started on the road to achieving your goals.