Stay informed

Stay informed with what’s going on. Browse posts that might be helpful to you or check out an event happening in your area. Come back regularly as this page is kept up-to-date with a lot of relevant information.

A tax refund can feel like “extra” money — but it can also be a powerful planning moment. Putting it toward the right goal (RRSP, TFSA, debt strategy, or a targeted savings plan) can help you build momentum. The best move depends on your priorities — and your timeline. Let’s chat about your goals.

A tax refund can feel like “extra” money — but it can also be a powerful planning moment. Putting it toward the right goal (RRSP, TFSA, debt strategy, or a targeted savings plan) can help you build momentum. The best move depends on your priorities — and your timeline. Let’s chat about your goals.

You are unique. So is your retirement roadmap.

Our OnePlan can help bring your goals, investments and income strategy together into one clear & holistic financial picture, so you see what’s possible and adjust as life changes. Would you like to explore your retirement options?

https://advisor.sunlife.ca/michael.wang

#SunLifeOnePlan #RetirementPlanning

Our OnePlan can help bring your goals, investments and income strategy together into one clear & holistic financial picture, so you see what’s possible and adjust as life changes. Would you like to explore your retirement options?

https://advisor.sunlife.ca/michael.wang

#SunLifeOnePlan #RetirementPlanning

You are unique. So is your retirement roadmap.

Our OnePlan can help bring your goals, investments and income strategy together into one clear & holistic financial picture, so you see what’s possible and adjust as life changes. Would you like to explore your retirement options?

https://advisor.sunlife.ca/michael.wang

#SunLifeOnePlan #RetirementPlanning

Our OnePlan can help bring your goals, investments and income strategy together into one clear & holistic financial picture, so you see what’s possible and adjust as life changes. Would you like to explore your retirement options?

https://advisor.sunlife.ca/michael.wang

#SunLifeOnePlan #RetirementPlanning

Your mortgage is likely one of your biggest financial commitments. What happens to it if something unexpected occurs? Mortgage protection insurance helps ensure your family can keep your home secure, no matter what life brings. Let's review your coverage and give you peace of mind. Reach out to discuss your options today.

https://advisor.sunlife.ca/michael.wang

https://advisor.sunlife.ca/michael.wang

Your mortgage is likely one of your biggest financial commitments. What happens to it if something unexpected occurs? Mortgage protection insurance helps ensure your family can keep your home secure, no matter what life brings. Let's review your coverage and give you peace of mind. Reach out to discuss your options today.

https://advisor.sunlife.ca/michael.wang

https://advisor.sunlife.ca/michael.wang

Congratulations on graduating! Now comes the next chapter, managing student debt while building your future. From repayment strategies to integrating loans into your financial roadmap, let's make sure you're set up for success. Whether it's buying a first home or saving for further education, we can help you navigate it all. Let's talk!

Congratulations on graduating! Now comes the next chapter, managing student debt while building your future. From repayment strategies to integrating loans into your financial roadmap, let's make sure you're set up for success. Whether it's buying a first home or saving for further education, we can help you navigate it all. Let's talk!

When your finances are complex, an intentional and well-executed strategy is key to maximizing what's possible.

Coordinating taxes, investments, and protection can help you preserve what you’ve built — and when it's time to pass it on, your beneficiaries can receive what you intended for them to receive, tax efficiently, or even tax-free.

Transferring wealth can be about more than assets; it’s about values, fairness, and protecting the people you care about. With the right planning, you can help reduce friction, manage tax impacts and keep your legacy aligned with your wishes.

Let’s talk about strategies that work best for you and your family's and future. https://advisor.sunlife.ca/michael.wang

Coordinating taxes, investments, and protection can help you preserve what you’ve built — and when it's time to pass it on, your beneficiaries can receive what you intended for them to receive, tax efficiently, or even tax-free.

Transferring wealth can be about more than assets; it’s about values, fairness, and protecting the people you care about. With the right planning, you can help reduce friction, manage tax impacts and keep your legacy aligned with your wishes.

Let’s talk about strategies that work best for you and your family's and future. https://advisor.sunlife.ca/michael.wang

When your finances are complex, an intentional and well-executed strategy is key to maximizing what's possible.

Coordinating taxes, investments, and protection can help you preserve what you’ve built — and when it's time to pass it on, your beneficiaries can receive what you intended for them to receive, tax efficiently, or even tax-free.

Transferring wealth can be about more than assets; it’s about values, fairness, and protecting the people you care about. With the right planning, you can help reduce friction, manage tax impacts and keep your legacy aligned with your wishes.

Let’s talk about strategies that work best for you and your family's and future. https://advisor.sunlife.ca/michael.wang

Coordinating taxes, investments, and protection can help you preserve what you’ve built — and when it's time to pass it on, your beneficiaries can receive what you intended for them to receive, tax efficiently, or even tax-free.

Transferring wealth can be about more than assets; it’s about values, fairness, and protecting the people you care about. With the right planning, you can help reduce friction, manage tax impacts and keep your legacy aligned with your wishes.

Let’s talk about strategies that work best for you and your family's and future. https://advisor.sunlife.ca/michael.wang

Taxes complete? Now is the perfect time to think bigger. Your tax refund is an opportunity to strengthen your financial foundation. Whether it's boosting RRSP contributions, maximizing investment strategies or planning for next year, let's help ensure every dollar works harder for you. Questions about how to best utilize your tax return? Let's chat!

https://advisor.sunlife.ca/michael.wang

https://advisor.sunlife.ca/michael.wang

Taxes complete? Now is the perfect time to think bigger. Your tax refund is an opportunity to strengthen your financial foundation. Whether it's boosting RRSP contributions, maximizing investment strategies or planning for next year, let's help ensure every dollar works harder for you. Questions about how to best utilize your tax return? Let's chat!

https://advisor.sunlife.ca/michael.wang

https://advisor.sunlife.ca/michael.wang

Retirement doesn't have to be just a number.

It can become a real strategy and we can all take concrete steps towards it, starting from today.

Pension, personal income, investment returns, "what-if's", health needs, certain event timings, and tax consequences all come together to impact your lifestyle in your retirement.

The sooner you explore and understand your options, the more choices you are likely to have later.

Let's connect to build your personal retirement roadmap!

It can become a real strategy and we can all take concrete steps towards it, starting from today.

Pension, personal income, investment returns, "what-if's", health needs, certain event timings, and tax consequences all come together to impact your lifestyle in your retirement.

The sooner you explore and understand your options, the more choices you are likely to have later.

Let's connect to build your personal retirement roadmap!

Retirement doesn't have to be just a number.

It can become a real strategy and we can all take concrete steps towards it, starting from today.

Pension, personal income, investment returns, "what-if's", health needs, certain event timings, and tax consequences all come together to impact your lifestyle in your retirement.

The sooner you explore and understand your options, the more choices you are likely to have later.

Let's connect to build your personal retirement roadmap!

It can become a real strategy and we can all take concrete steps towards it, starting from today.

Pension, personal income, investment returns, "what-if's", health needs, certain event timings, and tax consequences all come together to impact your lifestyle in your retirement.

The sooner you explore and understand your options, the more choices you are likely to have later.

Let's connect to build your personal retirement roadmap!

This Seniors Month, let's talk about staying safe. Grandparent scams are targeting our older adults. Awareness is your best defense.

How It Works:

Scammers call claiming to be a grandchild in legal trouble, asking for urgent money via wire transfer, crypto or gift cards. They pressure you to keep it secret.

Don't Fall for It:

• Hang up and verify – Call your grandchild directly to confirm the story

• Ask questions – If they say "It's me," ask which grandchild is calling

• Set a family password – Agree on a code word for real emergencies

• Never rush – Legitimate agencies don't send couriers for cash payments

• Never send money - Lawyers and police don't collect money this way

If something feels off, it probably is. Trust your instincts and reach out to family or authorities. Stay informed. Stay safe. Protect what matters.

How It Works:

Scammers call claiming to be a grandchild in legal trouble, asking for urgent money via wire transfer, crypto or gift cards. They pressure you to keep it secret.

Don't Fall for It:

• Hang up and verify – Call your grandchild directly to confirm the story

• Ask questions – If they say "It's me," ask which grandchild is calling

• Set a family password – Agree on a code word for real emergencies

• Never rush – Legitimate agencies don't send couriers for cash payments

• Never send money - Lawyers and police don't collect money this way

If something feels off, it probably is. Trust your instincts and reach out to family or authorities. Stay informed. Stay safe. Protect what matters.

This Seniors Month, let's talk about staying safe. Grandparent scams are targeting our older adults. Awareness is your best defense.

How It Works:

Scammers call claiming to be a grandchild in legal trouble, asking for urgent money via wire transfer, crypto or gift cards. They pressure you to keep it secret.

Don't Fall for It:

• Hang up and verify – Call your grandchild directly to confirm the story

• Ask questions – If they say "It's me," ask which grandchild is calling

• Set a family password – Agree on a code word for real emergencies

• Never rush – Legitimate agencies don't send couriers for cash payments

• Never send money - Lawyers and police don't collect money this way

If something feels off, it probably is. Trust your instincts and reach out to family or authorities. Stay informed. Stay safe. Protect what matters.

How It Works:

Scammers call claiming to be a grandchild in legal trouble, asking for urgent money via wire transfer, crypto or gift cards. They pressure you to keep it secret.

Don't Fall for It:

• Hang up and verify – Call your grandchild directly to confirm the story

• Ask questions – If they say "It's me," ask which grandchild is calling

• Set a family password – Agree on a code word for real emergencies

• Never rush – Legitimate agencies don't send couriers for cash payments

• Never send money - Lawyers and police don't collect money this way

If something feels off, it probably is. Trust your instincts and reach out to family or authorities. Stay informed. Stay safe. Protect what matters.

Why choose between protection and savings when you can have both? Bundle term and permanent life insurance to save 10% for life on your permanent policy, AND get money back on critical illness coverage.

Build complete protection for multiple life scenarios while maximizing your savings. Let's talk about your protection needs!

Build complete protection for multiple life scenarios while maximizing your savings. Let's talk about your protection needs!

Why choose between protection and savings when you can have both? Bundle term and permanent life insurance to save 10% for life on your permanent policy, AND get money back on critical illness coverage.

Build complete protection for multiple life scenarios while maximizing your savings. Let's talk about your protection needs!

Build complete protection for multiple life scenarios while maximizing your savings. Let's talk about your protection needs!

You're building your future – let's help make sure it's protected.

Whether you're planning for your growing family or thinking about what you'll leave behind, our current offers make comprehensive coverage more affordable. Get 10% off permanent insurance when bundled with term insurance, and cash back on critical illness protection. Real savings for real life. Let’s chat! Offer ends July 31.

Whether you're planning for your growing family or thinking about what you'll leave behind, our current offers make comprehensive coverage more affordable. Get 10% off permanent insurance when bundled with term insurance, and cash back on critical illness protection. Real savings for real life. Let’s chat! Offer ends July 31.

You're building your future – let's help make sure it's protected.

Whether you're planning for your growing family or thinking about what you'll leave behind, our current offers make comprehensive coverage more affordable. Get 10% off permanent insurance when bundled with term insurance, and cash back on critical illness protection. Real savings for real life. Let’s chat! Offer ends July 31.

Whether you're planning for your growing family or thinking about what you'll leave behind, our current offers make comprehensive coverage more affordable. Get 10% off permanent insurance when bundled with term insurance, and cash back on critical illness protection. Real savings for real life. Let’s chat! Offer ends July 31.

Key person insurance and disability coverage aren't just good planning, they're essential. Whether you're a solo entrepreneur or running a team, having the right protection helps ensure your business (and your financial security) stays on track. Let's discuss potential gaps in your coverage.

Key person insurance and disability coverage aren't just good planning, they're essential. Whether you're a solo entrepreneur or running a team, having the right protection helps ensure your business (and your financial security) stays on track. Let's discuss potential gaps in your coverage.

3 TSX Stocks Built for Higher-for-Longer Interest Rates

Three TSX stocks are strong buys if a higher-for-longer interest rate environment is forthcoming. https://advisor.sunlife.ca/michael.wang

Everyone’s financial situation is different — and your investment approach should reflect that. Beyond stocks and bonds, there are other ways to help grow your wealth and reduce risk. Let's explore options that fit your comfort level, goals and the legacy you want to leave.

Everyone’s financial situation is different — and your investment approach should reflect that. Beyond stocks and bonds, there are other ways to help grow your wealth and reduce risk. Let's explore options that fit your comfort level, goals and the legacy you want to leave.

The Daily Chase: Inflation hits highest level in two years

Higher energy prices drove up Canada’s inflation rate to 2.8 per cent in April, reaching its highest level in nearly two years. https://advisor.sunlife.ca/michael.wang

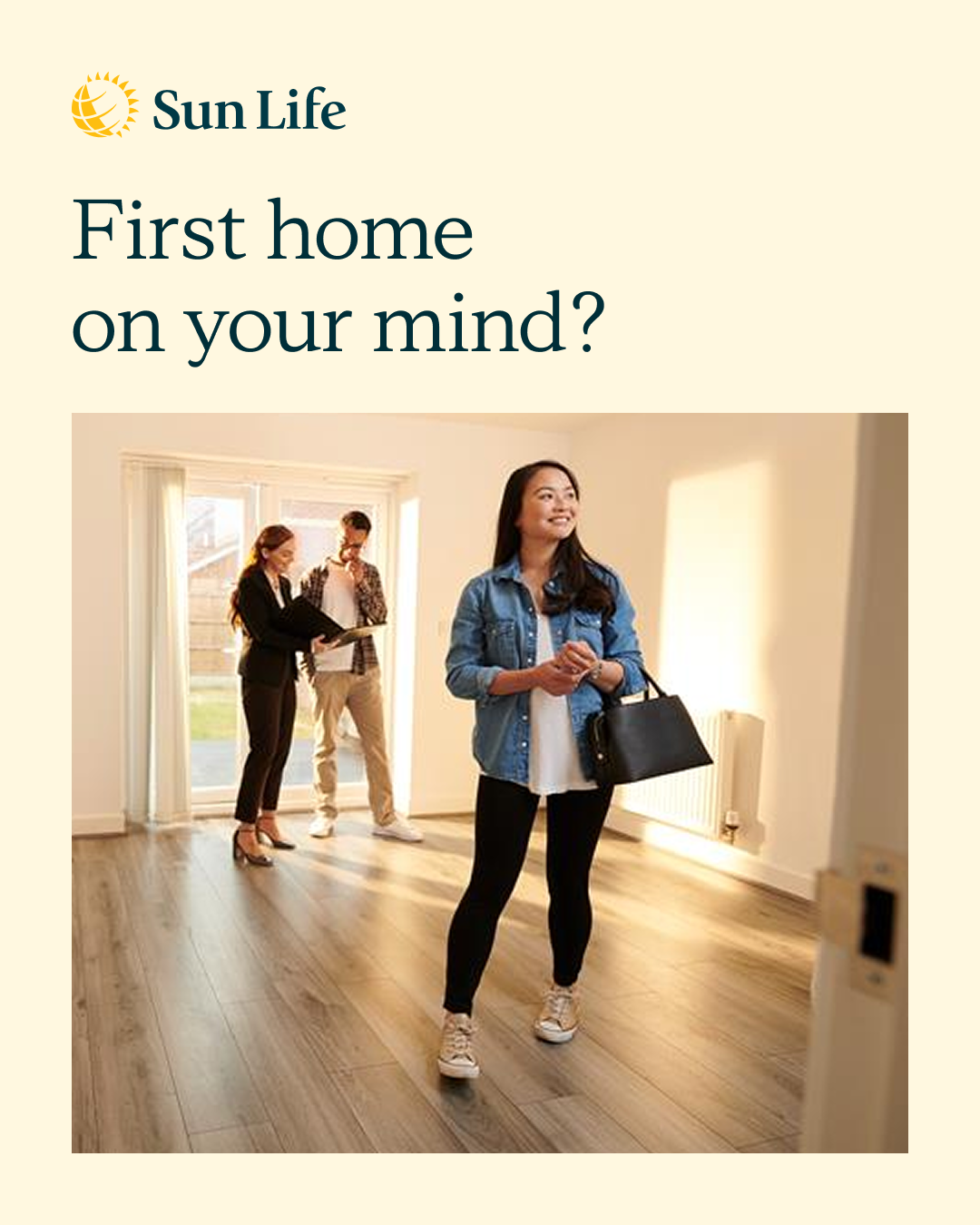

Dreaming of owning your first home? You might not know all the tools available to help you get there.

From RRSP Home Buyer's Plan withdrawals to the new First Home Savings Account (FHSA), there are smart strategies to help accelerate your down payment savings. Let's explore which options work best for your situation. Reach out today!

From RRSP Home Buyer's Plan withdrawals to the new First Home Savings Account (FHSA), there are smart strategies to help accelerate your down payment savings. Let's explore which options work best for your situation. Reach out today!

Dreaming of owning your first home? You might not know all the tools available to help you get there.

From RRSP Home Buyer's Plan withdrawals to the new First Home Savings Account (FHSA), there are smart strategies to help accelerate your down payment savings. Let's explore which options work best for your situation. Reach out today!

From RRSP Home Buyer's Plan withdrawals to the new First Home Savings Account (FHSA), there are smart strategies to help accelerate your down payment savings. Let's explore which options work best for your situation. Reach out today!

Retirement doesn't mean the end of growth — it's the start of a new, exciting life chapter! Did you know Revenue Canada lets you withdraw from you Sun Life RRSP to pay for education and development, helping keep your mind sharp and your skills current?

Whether it's picking up a new hobby, certification or passion project, let's explore how to fund your next adventure. Let’s talk about a plan that’s right for you.

Whether it's picking up a new hobby, certification or passion project, let's explore how to fund your next adventure. Let’s talk about a plan that’s right for you.

Retirement doesn't mean the end of growth — it's the start of a new, exciting life chapter! Did you know Revenue Canada lets you withdraw from you Sun Life RRSP to pay for education and development, helping keep your mind sharp and your skills current?

Whether it's picking up a new hobby, certification or passion project, let's explore how to fund your next adventure. Let’s talk about a plan that’s right for you.

Whether it's picking up a new hobby, certification or passion project, let's explore how to fund your next adventure. Let’s talk about a plan that’s right for you.

Health challenges can strike anyone. Critical illness insurance provides financial support when you need it most — helping you focus on recovery instead of financial stress. Whether you're supporting a loved one or managing personal expenses, having protection in place is invaluable. Let's talk! https://advisor.sunlife.ca/michael.wang

Health challenges can strike anyone. Critical illness insurance provides financial support when you need it most — helping you focus on recovery instead of financial stress. Whether you're supporting a loved one or managing personal expenses, having protection in place is invaluable. Let's talk! https://advisor.sunlife.ca/michael.wang

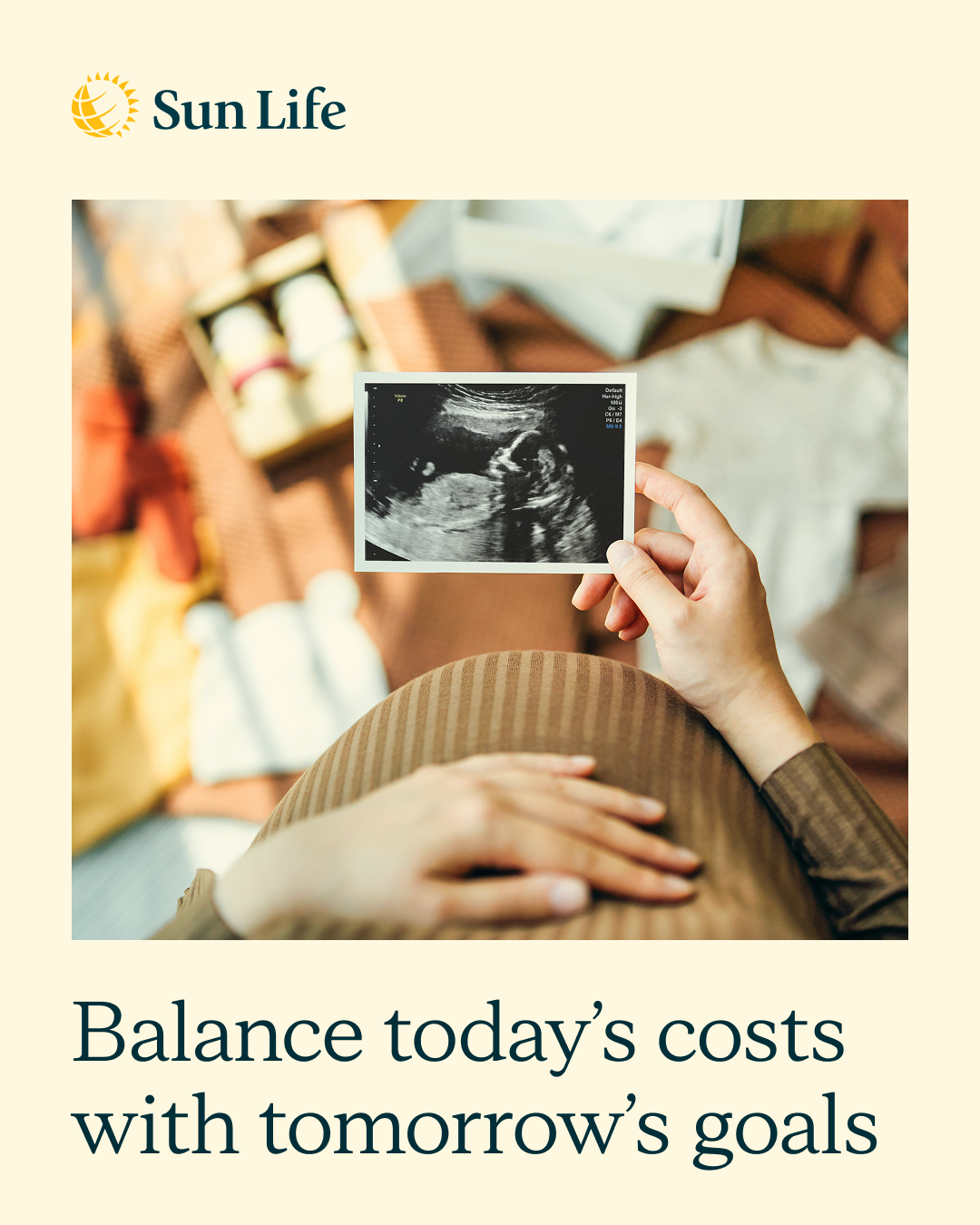

Growing your family is exciting but can also be expensive. Balancing today's costs (childcare, diapers, activities) with tomorrow's goals (education, home, experiences) takes planning. Let's build a family cash-flow roadmap that helps you save without sacrificing the moments that matter. Ready to create a strategy that works for your family? Get in touch. https://advisor.sunlife.ca/michael.wang

Growing your family is exciting but can also be expensive. Balancing today's costs (childcare, diapers, activities) with tomorrow's goals (education, home, experiences) takes planning. Let's build a family cash-flow roadmap that helps you save without sacrificing the moments that matter. Ready to create a strategy that works for your family? Get in touch. https://advisor.sunlife.ca/michael.wang

退休不僅僅是一個數字——更是一種生活方式。

無論您嚮往提早退休、轉換跑道,或是循序漸進地過渡到退休生活,我們都能協助您將夢想變為現實。從收入規劃到投資策略,讓我們運用 Sun Life One Plan 為您打造一份獨一無二的退休藍圖。您的退休故事,從這裡開始。您理想中的退休生活是什麼樣子?

無論您嚮往提早退休、轉換跑道,或是循序漸進地過渡到退休生活,我們都能協助您將夢想變為現實。從收入規劃到投資策略,讓我們運用 Sun Life One Plan 為您打造一份獨一無二的退休藍圖。您的退休故事,從這裡開始。您理想中的退休生活是什麼樣子?

退休不僅僅是一個數字——更是一種生活方式。

無論您嚮往提早退休、轉換跑道,或是循序漸進地過渡到退休生活,我們都能協助您將夢想變為現實。從收入規劃到投資策略,讓我們運用 Sun Life One Plan 為您打造一份獨一無二的退休藍圖。您的退休故事,從這裡開始。您理想中的退休生活是什麼樣子?

無論您嚮往提早退休、轉換跑道,或是循序漸進地過渡到退休生活,我們都能協助您將夢想變為現實。從收入規劃到投資策略,讓我們運用 Sun Life One Plan 為您打造一份獨一無二的退休藍圖。您的退休故事,從這裡開始。您理想中的退休生活是什麼樣子?

Strategic life insurance is a cornerstone of sophisticated financial planning. It allows you to help protect your family. It's not just coverage; it's a wealth transfer tool. Let's help ensure your life insurance strategy matches your net worth and goals. Ready for a conversation? https://advisor.sunlife.ca/michael.wang

Strategic life insurance is a cornerstone of sophisticated financial planning. It allows you to help protect your family. It's not just coverage; it's a wealth transfer tool. Let's help ensure your life insurance strategy matches your net worth and goals. Ready for a conversation? https://advisor.sunlife.ca/michael.wang

Have questions?

Here to help answer your questions, provide clarity about products and get you started on the road to achieving your goals.