Where Strategy Meets Your Scroll

You're busy running a business, raising a family and living your life - or all 3! We get it. That's exactly why we created a space where you can get real, practical financial insights without digging through confusing jargon or salesy fluff.

Our Instagram is built for people like you: entrepreneurs, professional and families who want to protect what they've built, grow what's next and create a legacy worth passing on. We break down the complex stuff - like taxes, investing, insurance and retirement into bite sized tips that actually make sense and fit your life.

From "why no one talks about corporate investing" to "how to spend smarter in retirement" our feed is full of strategy-backed advice that we'd give our own families (because we've been in your shoes).

Ready to go beyond the scroll? Tap the link below and book a meeting to see how we work differently... then follow us on Instagram to stay one step ahead, every step of the way.

It’s not.

Your TFSA is one of the most underutilized wealth building tools available to Canadian business owners.

Every dollar that grows inside it is completely tax free.

Every dollar you withdraw is completely tax free. No income inclusion. No CRA. No catch.

For incorporated business owners in Ontario the TFSA becomes even more powerful when coordinated alongside your corporate structure and RRSP withdrawal strategy.

The problem isn’t access. It’s awareness.

Swipe through for 5 things they never told you about your TFSA.

Which one surprised you most?

Own your plan. Own the outcome.

#GenerationalWealth #LegacyPlanning #CanadianWealth #WealthManagement #BusinessOwners

It’s not.

Your TFSA is one of the most underutilized wealth building tools available to Canadian business owners.

Every dollar that grows inside it is completely tax free.

Every dollar you withdraw is completely tax free. No income inclusion. No CRA. No catch.

For incorporated business owners in Ontario the TFSA becomes even more powerful when coordinated alongside your corporate structure and RRSP withdrawal strategy.

The problem isn’t access. It’s awareness.

Swipe through for 5 things they never told you about your TFSA.

Which one surprised you most?

Own your plan. Own the outcome.

#GenerationalWealth #LegacyPlanning #CanadianWealth #WealthManagement #BusinessOwners

But here’s what most people were never told.

Every dollar sitting in that account is still owed to CRA.

You didn’t eliminate the tax. You deferred it.

And without a clear strategy for how and when to withdraw — that deferral could cost you significantly more in retirement than you ever saved contributing to it.

For Ontario business owners especially — your RRSP can’t sit in isolation. It needs to work alongside your TFSA, your corporate structure and your estate plan. Without that coordination you’re not building a plan.

You’re building a problem.

Swipe through for the 5 things they never told you about your RRSP.

Which one surprised you most?

Own your plan. Own the outcome.

#GenerationalWealth #LegacyPlanning

#CanadianWealth #WealthManagement #BusinessOwners

But here’s what most people were never told.

Every dollar sitting in that account is still owed to CRA.

You didn’t eliminate the tax. You deferred it.

And without a clear strategy for how and when to withdraw — that deferral could cost you significantly more in retirement than you ever saved contributing to it.

For Ontario business owners especially — your RRSP can’t sit in isolation. It needs to work alongside your TFSA, your corporate structure and your estate plan. Without that coordination you’re not building a plan.

You’re building a problem.

Swipe through for the 5 things they never told you about your RRSP.

Which one surprised you most?

Own your plan. Own the outcome.

#GenerationalWealth #LegacyPlanning

#CanadianWealth #WealthManagement #BusinessOwners

Insurance can seem complicated (it doesn't need to be) and most people either think they are fully covered, or they don't want it at all... Until they really understand what they have and what they need.

Term coverage protects your family for a lower coast in the short term.

Mortgage insurance coverage protects what is owning on your house, but nothing more than that.

Work coverage helps, but that is the icing on the cake as the coverage is tied to your employer - change in work means change or loss of coverage.

The problem isn't the coverage itself. It's understanding how it works, how it fits together and whether it truly protects the people and lifestyle you care about.

Our focus is to simplify these conversations so business owners and families can make confident, intentional choice that help build lasting legacies.

Wealth and legacy don't happen by accident, they happen by strategy.

Comment WEALTH or DM me to build yours.

Insurance can seem complicated (it doesn't need to be) and most people either think they are fully covered, or they don't want it at all... Until they really understand what they have and what they need.

Term coverage protects your family for a lower coast in the short term.

Mortgage insurance coverage protects what is owning on your house, but nothing more than that.

Work coverage helps, but that is the icing on the cake as the coverage is tied to your employer - change in work means change or loss of coverage.

The problem isn't the coverage itself. It's understanding how it works, how it fits together and whether it truly protects the people and lifestyle you care about.

Our focus is to simplify these conversations so business owners and families can make confident, intentional choice that help build lasting legacies.

Wealth and legacy don't happen by accident, they happen by strategy.

Comment WEALTH or DM me to build yours.

OnePlan takes everything, your income, assets, retirement goals, and lifestyle plans and creates a step-by-step path to get you from today to retirement in the most tax efficient way.

It doesn’t stop there. OnePlan also shows you how to spend strategically so your money lasts and your legacy stays intact.

Wealth and legacy don’t happen by accident, they happen by strategy.

Comment WEALTH to start building yours.

#RetirementPlanning #WealthStrategy #LegacyPlanning #FinancialFreedom #TaxEfficient #BuildWithPurpose

OnePlan takes everything, your income, assets, retirement goals, and lifestyle plans and creates a step-by-step path to get you from today to retirement in the most tax efficient way.

It doesn’t stop there. OnePlan also shows you how to spend strategically so your money lasts and your legacy stays intact.

Wealth and legacy don’t happen by accident, they happen by strategy.

Comment WEALTH to start building yours.

#RetirementPlanning #WealthStrategy #LegacyPlanning #FinancialFreedom #TaxEfficient #BuildWithPurpose

When I talk to business owners about their financial strategy, one thing comes up again and again:

They’ve heard of the TFSA, but most think it’s just a place to stash a bit of extra cash.

The truth?

It’s one of the most powerful and flexible wealth-building tools available — especially when you understand how to use it strategically.

Think of your TFSA like a bucket that never leaks.

You fill it with after-tax dollars.

Those dollars grow — through investments like stocks, ETFs, or mutual funds — and none of that growth is ever taxed.

When you need the money, you can take it out freely, no penalties, no restrictions.

That kind of flexibility is rare.

It means you can use it to support your business cash flow, fund a big goal, or quietly build long-term wealth in the background.

The secret isn’t how much you start with — it’s how consistently you fill the bucket, and where you choose to pour from it when it’s full.

Because wealth doesn’t happen by accident.

It happens by strategy.

💬 Comment WEALTH to start building yours.

When I talk to business owners about their financial strategy, one thing comes up again and again:

They’ve heard of the TFSA, but most think it’s just a place to stash a bit of extra cash.

The truth?

It’s one of the most powerful and flexible wealth-building tools available — especially when you understand how to use it strategically.

Think of your TFSA like a bucket that never leaks.

You fill it with after-tax dollars.

Those dollars grow — through investments like stocks, ETFs, or mutual funds — and none of that growth is ever taxed.

When you need the money, you can take it out freely, no penalties, no restrictions.

That kind of flexibility is rare.

It means you can use it to support your business cash flow, fund a big goal, or quietly build long-term wealth in the background.

The secret isn’t how much you start with — it’s how consistently you fill the bucket, and where you choose to pour from it when it’s full.

Because wealth doesn’t happen by accident.

It happens by strategy.

💬 Comment WEALTH to start building yours.

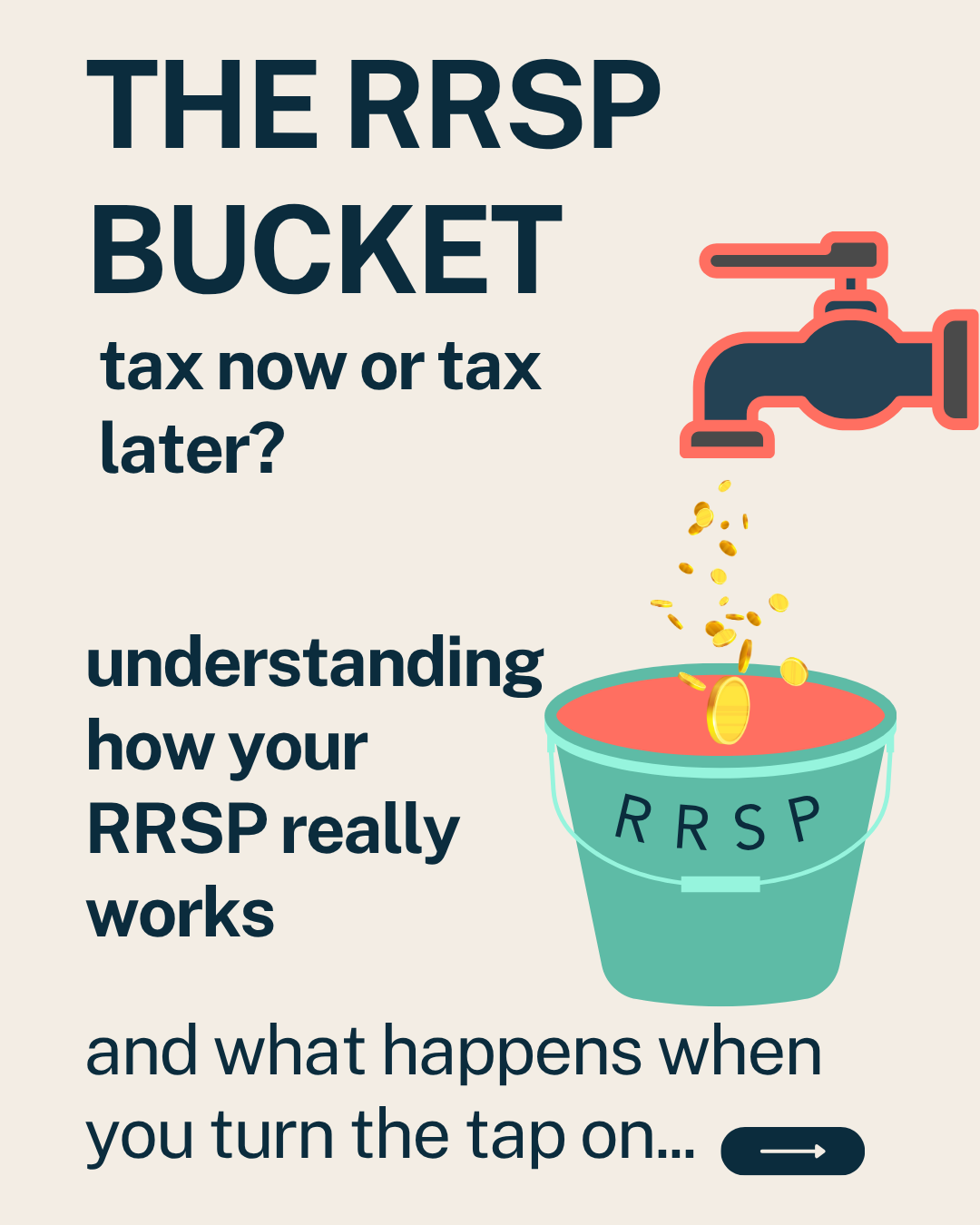

Most people see RRSPs as the golden ticket for retirement savings… and they can be.

But here’s what many forget — at some point, you have to stop filling the bucket and start turning the tap on.

✅ Contributions help reduce taxable income today

✅ Growth happens tax-deferred

🚰 Withdrawals are taxed as income — and by age 71, the government requires you to start drawing down

RRSPs work best when you understand how (and when) to use them.

It’s not just about saving into the right bucket — it’s about knowing when and how to take it out.

If you’re building toward retirement, now’s the time to start planning how your income flows out just as efficiently as it flows in.

#RetirementPlanning #TaxSmartStrategies #WealthBuilding #SunLife #FinancialEducation

Most people see RRSPs as the golden ticket for retirement savings… and they can be.

But here’s what many forget — at some point, you have to stop filling the bucket and start turning the tap on.

✅ Contributions help reduce taxable income today

✅ Growth happens tax-deferred

🚰 Withdrawals are taxed as income — and by age 71, the government requires you to start drawing down

RRSPs work best when you understand how (and when) to use them.

It’s not just about saving into the right bucket — it’s about knowing when and how to take it out.

If you’re building toward retirement, now’s the time to start planning how your income flows out just as efficiently as it flows in.

#RetirementPlanning #TaxSmartStrategies #WealthBuilding #SunLife #FinancialEducation

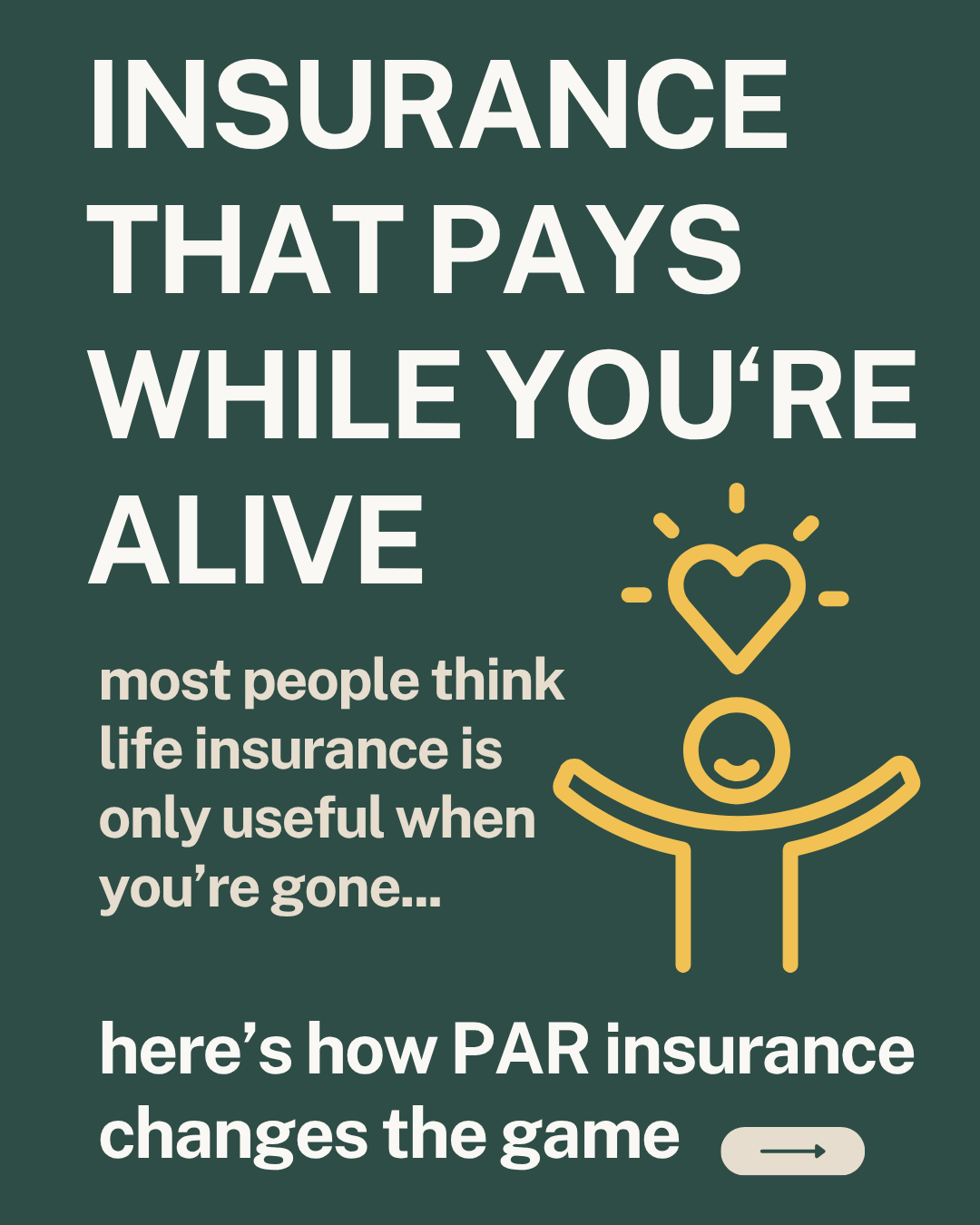

It’s not “just insurance.” It’s a strategy that can:

✅ Protect your family and business

✅ Build tax-advantaged cash value

✅ Participate in annual dividends

✅ Create flexible access to funds during your lifetime

Here’s how I explain it to clients:

Term protects what you have.

Permanent ensures it lasts.

Participating helps it grow while it’s protected.

A par policy isn’t for everyone... but for many incorporated professionals and business owners, it’s a cornerstone of a protection-first, tax-efficient legacy plan.

If you’re building long-term wealth for your family or your corporation, this strategy deserves a conversation.

💡 We help business owners, professionals and families protect what they’ve built and grow what’s next — with tax-smart, legacy-focused planning.

#LegacyAdvisory #WealthStrategy #InsurancePlanning #BusinessOwner #FinancialWellness

It’s not “just insurance.” It’s a strategy that can:

✅ Protect your family and business

✅ Build tax-advantaged cash value

✅ Participate in annual dividends

✅ Create flexible access to funds during your lifetime

Here’s how I explain it to clients:

Term protects what you have.

Permanent ensures it lasts.

Participating helps it grow while it’s protected.

A par policy isn’t for everyone... but for many incorporated professionals and business owners, it’s a cornerstone of a protection-first, tax-efficient legacy plan.

If you’re building long-term wealth for your family or your corporation, this strategy deserves a conversation.

💡 We help business owners, professionals and families protect what they’ve built and grow what’s next — with tax-smart, legacy-focused planning.

#LegacyAdvisory #WealthStrategy #InsurancePlanning #BusinessOwner #FinancialWellness

When it comes to saving for retirement, most people focus on how much they’re saving — not where they’re saving it.

RRSP. TFSA. Non-Registered.

Three different names for the same goal: building future wealth.

But here’s the truth most people overlook:

💡 The real difference between these accounts isn’t how they grow — it’s how they’re taxed.

🪣 Bucket 1: The RRSP

Think of this as your tax-deferral bucket.

You contribute before tax, lower your taxable income today, and pay tax later — ideally when your income is lower in retirement.

✅ Great for high-income earners or business owners with fluctuating income.

🪣 Bucket 2: The TFSA

Your tax-free growth bucket.

You contribute after tax, but everything you earn — interest, dividends, capital gains — grows and comes out completely tax-free.

✅ Ideal for long-term growth or flexible access before retirement.

🪣 Bucket 3: The Non-Registered Account

Your no-limit bucket.

No contribution caps, no withdrawal rules — but you’ll pay tax along the way on interest, dividends, and capital gains.

✅ Great for business owners or incorporated professionals who’ve maxed other options and want flexibility.

The truth is, it’s all the same water, your money.

What changes is how each bucket is taxed and when you choose to pay that tax.

The smartest plan isn’t about picking one bucket…

It’s about knowing how to fill each one strategically based on your income, goals, and future tax outlook.

Protect. Grow. Transfer.

That’s how we help business owners and families create tax-smart retirement and legacy strategies that last generations.

#LegacyAdvisory #WealthStrategy #TaxSmartWealth #BusinessOwnerPlanning #RetirementStrategy

When it comes to saving for retirement, most people focus on how much they’re saving — not where they’re saving it.

RRSP. TFSA. Non-Registered.

Three different names for the same goal: building future wealth.

But here’s the truth most people overlook:

💡 The real difference between these accounts isn’t how they grow — it’s how they’re taxed.

🪣 Bucket 1: The RRSP

Think of this as your tax-deferral bucket.

You contribute before tax, lower your taxable income today, and pay tax later — ideally when your income is lower in retirement.

✅ Great for high-income earners or business owners with fluctuating income.

🪣 Bucket 2: The TFSA

Your tax-free growth bucket.

You contribute after tax, but everything you earn — interest, dividends, capital gains — grows and comes out completely tax-free.

✅ Ideal for long-term growth or flexible access before retirement.

🪣 Bucket 3: The Non-Registered Account

Your no-limit bucket.

No contribution caps, no withdrawal rules — but you’ll pay tax along the way on interest, dividends, and capital gains.

✅ Great for business owners or incorporated professionals who’ve maxed other options and want flexibility.

The truth is, it’s all the same water, your money.

What changes is how each bucket is taxed and when you choose to pay that tax.

The smartest plan isn’t about picking one bucket…

It’s about knowing how to fill each one strategically based on your income, goals, and future tax outlook.

Protect. Grow. Transfer.

That’s how we help business owners and families create tax-smart retirement and legacy strategies that last generations.

#LegacyAdvisory #WealthStrategy #TaxSmartWealth #BusinessOwnerPlanning #RetirementStrategy

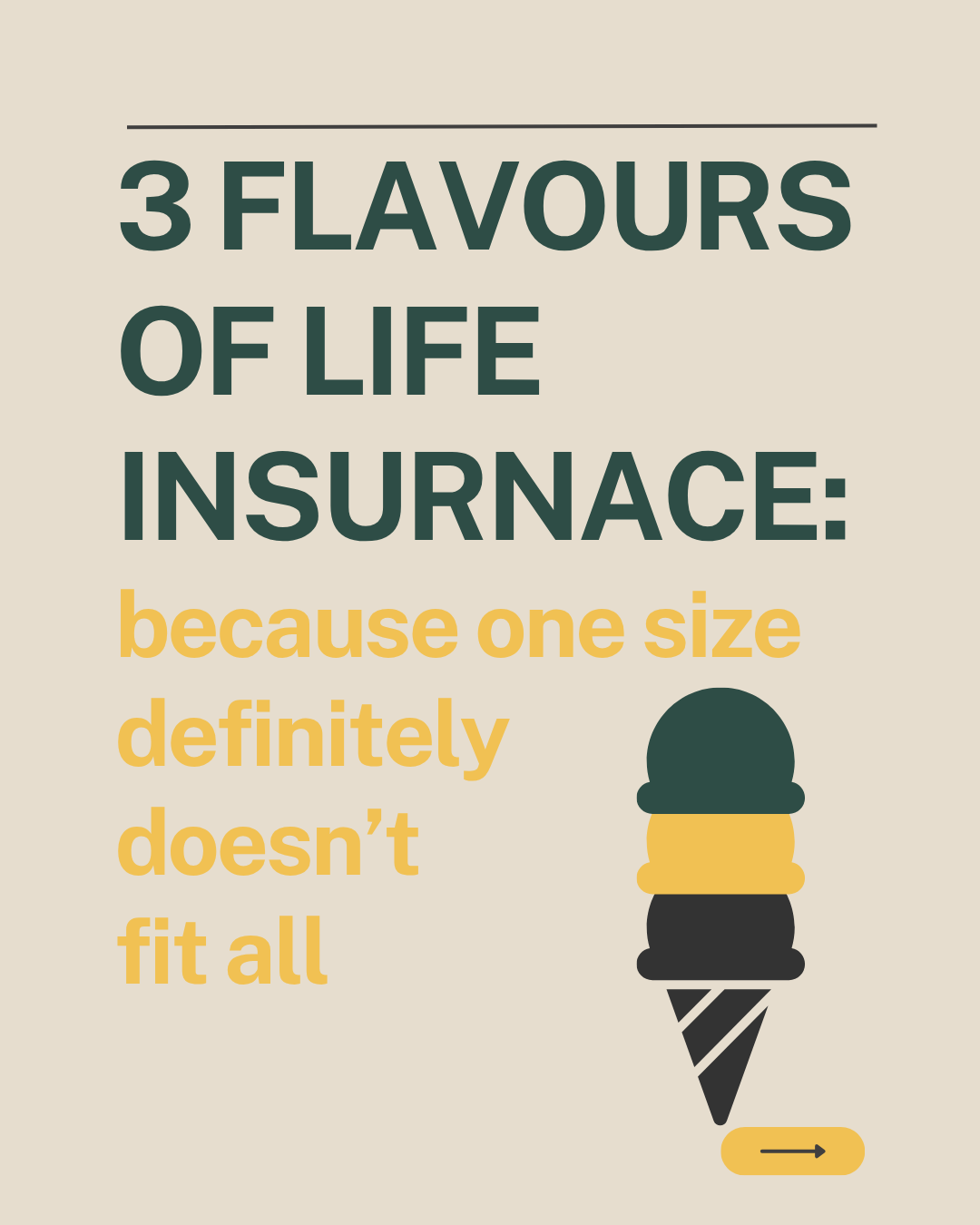

Let’s talk about life insurance — because yes, it’s more exciting than it sounds (especially when it’s protecting everything you’ve built).

Here’s the scoop 🍨👇

1️⃣ Term — “The Temporary Fix”

Think of it like renting coverage.

✅ Great for young families or new business owners

✅ Covers mortgages, income, and debts

💡 Low cost, high coverage — but it expires when the term’s up

2️⃣ Permanent — “The Lifelong Ride”

Coverage that never ends.

✅ Perfect for long-term protection or estate needs

✅ Premiums stay predictable

💡 Think: peace of mind that doesn’t expire

3️⃣ Participating (Par) — “The Legacy Builder”

Insurance that can actually grow over time.

✅ You’re part owner of the policy

✅ Earn potential dividends

💡 Great for building tax-advantaged wealth inside your plan

Bottom line — there’s no “best” type, just the one that fits your goals.

That’s where a proper strategy (and the right guide 👋) comes in.

If you’re ready to find out which type makes sense for you, let’s map it out together.

#LegacyAdvisory #WealthStrategy #BusinessOwnerPlanning #SunLifeAdvisor #ProtectGrowTransfer #TaxSmartWealth #FinancialConfidence

Let’s talk about life insurance — because yes, it’s more exciting than it sounds (especially when it’s protecting everything you’ve built).

Here’s the scoop 🍨👇

1️⃣ Term — “The Temporary Fix”

Think of it like renting coverage.

✅ Great for young families or new business owners

✅ Covers mortgages, income, and debts

💡 Low cost, high coverage — but it expires when the term’s up

2️⃣ Permanent — “The Lifelong Ride”

Coverage that never ends.

✅ Perfect for long-term protection or estate needs

✅ Premiums stay predictable

💡 Think: peace of mind that doesn’t expire

3️⃣ Participating (Par) — “The Legacy Builder”

Insurance that can actually grow over time.

✅ You’re part owner of the policy

✅ Earn potential dividends

💡 Great for building tax-advantaged wealth inside your plan

Bottom line — there’s no “best” type, just the one that fits your goals.

That’s where a proper strategy (and the right guide 👋) comes in.

If you’re ready to find out which type makes sense for you, let’s map it out together.

#LegacyAdvisory #WealthStrategy #BusinessOwnerPlanning #SunLifeAdvisor #ProtectGrowTransfer #TaxSmartWealth #FinancialConfidence

When I owned restaurants, I protected the business before I ever protected myself or my family.

Most business owners do the same...and it’s backwards.

We spend years protecting what we’ve built, instead of protecting the people we’re building it for.

Here’s the truth most entrepreneurs learn the hard way:

Your business isn’t the plan — it’s the engine that funds it.

A sustainable wealth and legacy plan starts by separating your business from your personal protection.

Because when something happens to you…

– The business loses its driver.

– The family loses its income.

– And the dream you worked for can stall overnight.

The right protection plan ensures that what you’ve built continues running — for your family, your employees, and your legacy.

It’s not just about life insurance or disability coverage.

It’s about designing a plan that protects:

✅ Your income

✅ Your business continuity

✅ Your family’s lifestyle

✅ And the future you’ve been working toward

Once protection is in place, that’s when we start optimizing for wealth and tax efficiency — corporate investing, legacy transfers, retirement income strategies.

But protection always comes first.

Because without it, everything else is built on hope.

If you’re a business owner or incorporated professional, and you’ve been meaning to “get around” to your personal protection plan…

This is your sign to start.

Let’s make sure the plan that protects your business also protects the people who matter most.

Send me a message — I’ll help you build it the right way.

When I owned restaurants, I protected the business before I ever protected myself or my family.

Most business owners do the same...and it’s backwards.

We spend years protecting what we’ve built, instead of protecting the people we’re building it for.

Here’s the truth most entrepreneurs learn the hard way:

Your business isn’t the plan — it’s the engine that funds it.

A sustainable wealth and legacy plan starts by separating your business from your personal protection.

Because when something happens to you…

– The business loses its driver.

– The family loses its income.

– And the dream you worked for can stall overnight.

The right protection plan ensures that what you’ve built continues running — for your family, your employees, and your legacy.

It’s not just about life insurance or disability coverage.

It’s about designing a plan that protects:

✅ Your income

✅ Your business continuity

✅ Your family’s lifestyle

✅ And the future you’ve been working toward

Once protection is in place, that’s when we start optimizing for wealth and tax efficiency — corporate investing, legacy transfers, retirement income strategies.

But protection always comes first.

Because without it, everything else is built on hope.

If you’re a business owner or incorporated professional, and you’ve been meaning to “get around” to your personal protection plan…

This is your sign to start.

Let’s make sure the plan that protects your business also protects the people who matter most.

Send me a message — I’ll help you build it the right way.

I look at every financial plan in three stages:

1️⃣ Protect what you’ve built

Before anything else, protect your income, your family, and your business. That’s your foundation — life insurance, disability coverage, and critical illness protection. You can’t build wealth if your base isn’t secure.

2️⃣ Grow your wealth intentionally

Once you’ve protected your foundation, you can focus on corporate investing, RRSPs, TFSAs, and passive growth strategies. The goal is to make your money work as hard as you do.

3️⃣ Transfer it tax-efficiently

This is where true legacy planning begins. Using corporate structures, permanent insurance, and tax-smart estate tools, you make sure your wealth passes to your family — not the CRA.

👉 Skipping any of these stages means you’re building on sand.

The smartest families I work with build backwards, starting with protection, then stacking growth and legacy on top.

Most people want to start and stop at growth, but the real magic starts with protection and truly shows up when you plan the transfer.

Let's talk about how to not miss the first step, and make the last one seamless!

I look at every financial plan in three stages:

1️⃣ Protect what you’ve built

Before anything else, protect your income, your family, and your business. That’s your foundation — life insurance, disability coverage, and critical illness protection. You can’t build wealth if your base isn’t secure.

2️⃣ Grow your wealth intentionally

Once you’ve protected your foundation, you can focus on corporate investing, RRSPs, TFSAs, and passive growth strategies. The goal is to make your money work as hard as you do.

3️⃣ Transfer it tax-efficiently

This is where true legacy planning begins. Using corporate structures, permanent insurance, and tax-smart estate tools, you make sure your wealth passes to your family — not the CRA.

👉 Skipping any of these stages means you’re building on sand.

The smartest families I work with build backwards, starting with protection, then stacking growth and legacy on top.

Most people want to start and stop at growth, but the real magic starts with protection and truly shows up when you plan the transfer.

Let's talk about how to not miss the first step, and make the last one seamless!

When I sit with business owners and families, one of the first questions I get is: “Where do I start?”

For most, the answer is Term Life Insurance.

Here’s why:

✅ It’s affordable — giving you maximum coverage during the years when your obligations are highest.

✅ It protects your family against the unexpected — mortgage, business loans, income replacement.

✅ It creates a foundation for your legacy plan — making sure your loved ones are secure while you grow and build wealth.

Term insurance isn’t the finish line. It’s the starting point.

And while none of us want to “win” this bet, taking it is one of the smartest moves you can make for your family and business.

If you’re still in the “growth years,” don’t skip the most important step. Let’s make sure your protection matches the life you’re building.

#LegacyPlanning #LifeInsurance #Entrepreneurship #FamilyWealth #OntarioBusiness #BusinessOwners

When I sit with business owners and families, one of the first questions I get is: “Where do I start?”

For most, the answer is Term Life Insurance.

Here’s why:

✅ It’s affordable — giving you maximum coverage during the years when your obligations are highest.

✅ It protects your family against the unexpected — mortgage, business loans, income replacement.

✅ It creates a foundation for your legacy plan — making sure your loved ones are secure while you grow and build wealth.

Term insurance isn’t the finish line. It’s the starting point.

And while none of us want to “win” this bet, taking it is one of the smartest moves you can make for your family and business.

If you’re still in the “growth years,” don’t skip the most important step. Let’s make sure your protection matches the life you’re building.

#LegacyPlanning #LifeInsurance #Entrepreneurship #FamilyWealth #OntarioBusiness #BusinessOwners

Here are three core types of life insurance I walk clients through:

🔹 Term Insurance

Best for: Young families, business owners with debt, or anyone needing affordable coverage for a set period.

Why: It’s simple, cost-effective protection during the “what if” years when obligations are highest.

🔹 Whole Life Insurance

Best for: Professionals and families looking for permanent protection and stability.

Why: Provides lifelong coverage, guaranteed cash value, and estate planning benefits.

🔹 Participating Whole Life (PAR) Insurance

Best for: High-net-worth individuals and entrepreneurs who want protection that also grows with them.

Why: Provides lifetime coverage and the opportunity to participate in dividends, creating tax-advantaged growth and a tool for generational wealth transfer.

👉 The best plan isn’t just about choosing a product — it’s about matching the strategy to your family’s goals and your business reality.

Here are three core types of life insurance I walk clients through:

🔹 Term Insurance

Best for: Young families, business owners with debt, or anyone needing affordable coverage for a set period.

Why: It’s simple, cost-effective protection during the “what if” years when obligations are highest.

🔹 Whole Life Insurance

Best for: Professionals and families looking for permanent protection and stability.

Why: Provides lifelong coverage, guaranteed cash value, and estate planning benefits.

🔹 Participating Whole Life (PAR) Insurance

Best for: High-net-worth individuals and entrepreneurs who want protection that also grows with them.

Why: Provides lifetime coverage and the opportunity to participate in dividends, creating tax-advantaged growth and a tool for generational wealth transfer.

👉 The best plan isn’t just about choosing a product — it’s about matching the strategy to your family’s goals and your business reality.

Not investing.

Not scaling.

Not chasing the next opportunity.

The truth is, none of that matters if your foundation isn’t secure.

I’ve seen entrepreneurs build incredible businesses and professionals work decades to create wealth, only to see large portions of it lost due to injury, illness, death or poor planning.

The most successful families I work with don’t just think about today. They plan with the end in mind, building wealth backward from the legacy they want to leave.

👉 That’s how you ensure your family, your business, and your values last longer than you do.

If you’re curious about how Ontario’s most successful families structure their legacy, let’s start the conversation.

Not investing.

Not scaling.

Not chasing the next opportunity.

The truth is, none of that matters if your foundation isn’t secure.

I’ve seen entrepreneurs build incredible businesses and professionals work decades to create wealth, only to see large portions of it lost due to injury, illness, death or poor planning.

The most successful families I work with don’t just think about today. They plan with the end in mind, building wealth backward from the legacy they want to leave.

👉 That’s how you ensure your family, your business, and your values last longer than you do.

If you’re curious about how Ontario’s most successful families structure their legacy, let’s start the conversation.

When it comes to passing wealth from one generation to the next, tax efficiency isn’t automatic — it’s engineered.

Too often, I see entrepreneurs and families with significant assets but no coordinated plan. The result?

• More tax than necessary

• Less control over how wealth is passed down

• Missed opportunities to create lasting impact for future generations

A properly structured plan does more than grow wealth. It ensures wealth moves efficiently, privately, and intentionally — instead of being eroded by avoidable tax.

If you’re unsure whether your current plan is optimized, we offer a quiet second opinion. No pressure. No agenda. Just a clear view of whether your legacy is as secure — and tax-efficient — as it could be.

Let’s make sure every dollar you’ve earned stays working for your family.

Message me directly to schedule a confidential conversation.

When it comes to passing wealth from one generation to the next, tax efficiency isn’t automatic — it’s engineered.

Too often, I see entrepreneurs and families with significant assets but no coordinated plan. The result?

• More tax than necessary

• Less control over how wealth is passed down

• Missed opportunities to create lasting impact for future generations

A properly structured plan does more than grow wealth. It ensures wealth moves efficiently, privately, and intentionally — instead of being eroded by avoidable tax.

If you’re unsure whether your current plan is optimized, we offer a quiet second opinion. No pressure. No agenda. Just a clear view of whether your legacy is as secure — and tax-efficient — as it could be.

Let’s make sure every dollar you’ve earned stays working for your family.

Message me directly to schedule a confidential conversation.

Every year, Canadian business owners and families hand over far more than they need to—not because they’re careless, but because no one ever showed them how to structure their business and personal finances properly.

With the right systems and planning, you can:

• Grow your wealth inside your corporation

• Protect your legacy for the next generation

• Put more of your hard-earned money into your family’s hands, not into taxes

This is exactly what I help Canadian business owners and families do every day, build tax-efficient strategies that ensure their effort translates into real, lasting wealth.

You’ve worked hard to earn it. Let’s make sure it stays with the people who matter most.

Every year, Canadian business owners and families hand over far more than they need to—not because they’re careless, but because no one ever showed them how to structure their business and personal finances properly.

With the right systems and planning, you can:

• Grow your wealth inside your corporation

• Protect your legacy for the next generation

• Put more of your hard-earned money into your family’s hands, not into taxes

This is exactly what I help Canadian business owners and families do every day, build tax-efficient strategies that ensure their effort translates into real, lasting wealth.

You’ve worked hard to earn it. Let’s make sure it stays with the people who matter most.

It’s exciting — but if you don’t get the financial side right, it can cost you more than you think.

Here are 4 tips to keep more of what you earn:

1️⃣ Separate your personal and business finances.

Open a dedicated account for your side gig. It’s the only way to clearly track how your business is growing (and avoid messy year-end surprises).

2️⃣ Keep detailed records.

Save receipts. Log every expense. Self-employment income can come with hefty tax implications — and clean records mean you can write off legitimate costs with confidence.

3️⃣ Plan for taxes before they plan for you.

Don’t wait until April to figure it out. Put systems in place early — whether that’s an accountant, bookkeeping software, or both — to make sure you’re maximizing what you keep.

4️⃣ Protect yourself with the right insurance.

Disability coverage (even for your non-working hours), life insurance, and strategic ways to turn your business into an asset-building machine — these aren’t just “extras,” they’re part of building something sustainable.

If you’ve recently launched a side gig and want to make sure your money’s working as hard as you are, reach out. I’ve been where you are — side hustles, brick-and-mortar businesses, and now working with business owners to build plans that really work.

If you have questions about how to handle your new income, reach out!

It’s exciting — but if you don’t get the financial side right, it can cost you more than you think.

Here are 4 tips to keep more of what you earn:

1️⃣ Separate your personal and business finances.

Open a dedicated account for your side gig. It’s the only way to clearly track how your business is growing (and avoid messy year-end surprises).

2️⃣ Keep detailed records.

Save receipts. Log every expense. Self-employment income can come with hefty tax implications — and clean records mean you can write off legitimate costs with confidence.

3️⃣ Plan for taxes before they plan for you.

Don’t wait until April to figure it out. Put systems in place early — whether that’s an accountant, bookkeeping software, or both — to make sure you’re maximizing what you keep.

4️⃣ Protect yourself with the right insurance.

Disability coverage (even for your non-working hours), life insurance, and strategic ways to turn your business into an asset-building machine — these aren’t just “extras,” they’re part of building something sustainable.

If you’ve recently launched a side gig and want to make sure your money’s working as hard as you are, reach out. I’ve been where you are — side hustles, brick-and-mortar businesses, and now working with business owners to build plans that really work.

If you have questions about how to handle your new income, reach out!

If you run your own business or have a side hustle, you are your most valuable asset.

Without you, there’s no sales, no service, no revenue.

Yet, most self-employed people I speak with have zero disability protection in place.

Here’s the hard truth:

• An injury or illness can take you out of work for months—or longer.

• Without coverage, your income stops, but your bills and business expenses don’t.

• Your savings (and retirement plans) can be wiped out faster than you think.

If your ability to work is your greatest income-producing asset, why leave it unprotected?

Disability insurance is designed to replace a portion of your income if you can’t work due to illness or injury—helping you keep your business afloat, your personal bills paid, and your long-term plans intact.

The reality:

➡️ Employees often have group coverage.

➡️ Self-employed and side-business owners rarely do.

➡️ The financial fallout of not having it can be devastating.

You wouldn’t run your business without protecting your equipment, your inventory, or your intellectual property.

So why run it without protecting you?

If you’re self-employed or running a side business, it’s time to take this seriously.

Your income powers everything else—make sure it’s protected.

The process for coverage is simple, but the benefits are huge!

Interested? Let’s talk about if it’s right for you.

If you run your own business or have a side hustle, you are your most valuable asset.

Without you, there’s no sales, no service, no revenue.

Yet, most self-employed people I speak with have zero disability protection in place.

Here’s the hard truth:

• An injury or illness can take you out of work for months—or longer.

• Without coverage, your income stops, but your bills and business expenses don’t.

• Your savings (and retirement plans) can be wiped out faster than you think.

If your ability to work is your greatest income-producing asset, why leave it unprotected?

Disability insurance is designed to replace a portion of your income if you can’t work due to illness or injury—helping you keep your business afloat, your personal bills paid, and your long-term plans intact.

The reality:

➡️ Employees often have group coverage.

➡️ Self-employed and side-business owners rarely do.

➡️ The financial fallout of not having it can be devastating.

You wouldn’t run your business without protecting your equipment, your inventory, or your intellectual property.

So why run it without protecting you?

If you’re self-employed or running a side business, it’s time to take this seriously.

Your income powers everything else—make sure it’s protected.

The process for coverage is simple, but the benefits are huge!

Interested? Let’s talk about if it’s right for you.

As parents, we wear a lot of titles — provider, protector, role model, coach, problem solver. But if I’m being honest, the most important role we’ll ever have is making sure our families are cared for no matter what happens.

Here’s the truth: too many families are walking around under protected, relying on a single work policy or a bit of term coverage. And while those are steps in the right direction, they often fall short of what’s truly needed.

The families I work with are often surprised to learn that building a layered protection strategy doesn’t just mean “having insurance.” It means creating a plan that works for you in real life — one that covers the unexpected today and fuels your goals for tomorrow.

• Term insurance: Affordable protection during the years your family depends on you most.

• Permanent insurance: Lifetime coverage that guarantees stability and peace of mind.

• Participating policies: Protection that not only provides a growing death benefit but also builds tax-advantaged cash value you can use while you’re alive — for opportunities, emergencies, or to supercharge your retirement.

• Critical illness coverage: For you — and even your children — so that if a serious diagnosis ever strikes, you have the ability to step away from work, focus on what truly matters, and still keep your financial goals on track. With return-of-premium options, if you stay healthy, you can get your money back — turning peace of mind into a win-win.

When layered together, these solutions don’t just protect your family — they create a legacy and a financial foundation that lasts for generations.

Because at the end of the day, the cars, the house, the lifestyle… none of it matters if the people you love most aren’t secure.

So I’ll ask you this: If something happened tomorrow, would your family have certainty — or just hope?

As parents, we wear a lot of titles — provider, protector, role model, coach, problem solver. But if I’m being honest, the most important role we’ll ever have is making sure our families are cared for no matter what happens.

Here’s the truth: too many families are walking around under protected, relying on a single work policy or a bit of term coverage. And while those are steps in the right direction, they often fall short of what’s truly needed.

The families I work with are often surprised to learn that building a layered protection strategy doesn’t just mean “having insurance.” It means creating a plan that works for you in real life — one that covers the unexpected today and fuels your goals for tomorrow.

• Term insurance: Affordable protection during the years your family depends on you most.

• Permanent insurance: Lifetime coverage that guarantees stability and peace of mind.

• Participating policies: Protection that not only provides a growing death benefit but also builds tax-advantaged cash value you can use while you’re alive — for opportunities, emergencies, or to supercharge your retirement.

• Critical illness coverage: For you — and even your children — so that if a serious diagnosis ever strikes, you have the ability to step away from work, focus on what truly matters, and still keep your financial goals on track. With return-of-premium options, if you stay healthy, you can get your money back — turning peace of mind into a win-win.

When layered together, these solutions don’t just protect your family — they create a legacy and a financial foundation that lasts for generations.

Because at the end of the day, the cars, the house, the lifestyle… none of it matters if the people you love most aren’t secure.

So I’ll ask you this: If something happened tomorrow, would your family have certainty — or just hope?

I get it. You’re watching expenses. You’re trying to keep payroll moving. You’re hoping this quarter doesn’t turn into a longer storm.

But here’s the truth: the right insurance strategy doesn’t drain your business, it protects it from sinking. Especially in tough times.

Over the past few months, I’ve had conversations with business owners who’ve been navigating slower sales, rising costs, and unpredictable markets. Some of them have taken hits. Others are just trying to hold the line.

And here’s the pattern I’ve seen:

The ones who built proper risk protection into their financial plan, well before things got hard, have stayed afloat. Their families are protected. Their cash flow isn’t crippled. And their long-term goals haven’t been derailed.

Because when things go sideways, whether it’s a critical illness, a lawsuit, a sudden disability, or even an early death the right insurance solution can be the one thing that saves the business, the family, and the legacy you’ve worked so hard to build.

Here’s the key, though:

Protection can’t be built in isolation.

It needs to be part of a bigger plan that understands how your corporation operates, what your accountant is optimizing for, and how your legal structures are set up.

That’s where working with the right advisor matters.

I don’t just sell policies. I help business owners:

• Integrate protection into their corporate tax strategy

• Build legacy and succession plans that make sense

• Collaborate with their accountant, lawyer, and bookkeeper to ensure everything works together, not against each other

Whether it’s corporate-owned insurance for tax-efficient wealth transfer, buy-sell protection between partners, or a holding company strategy that supports retirement income down the road—it all starts with a plan that aligns with your goals and your business model.

If you’re building something that supports your family, your team, and your future…

Then now is the time to ask:

➡️ Is your business protected from the risks that could undo it all?

➡️ Have you built insurance into your offense strategy, not just as a backup?

➡️ Is your plan working hand-in-hand with your accountant and lawyer—or is it sitting in a drawer somewhere?

If the answer isn’t crystal clear, it might be time for a conversation.

Let’s build a plan that protects your hard work, honors your goals, and grows alongside your business.

📩 Send me a message if you want to chat. I’ll walk you through the same process we use with business owners to protect what matters, without overcomplicating things.

And if you’ve worked with me and know someone who needs this kind of support, I’d be grateful for the introduction.

#BusinessPlanning #LegacyPlanning #InsuranceForBusinessOwners #CorporateStrategy #TaxEfficiency #FamilyLegacy #WealthPlanning #Entrepreneurs

I get it. You’re watching expenses. You’re trying to keep payroll moving. You’re hoping this quarter doesn’t turn into a longer storm.

But here’s the truth: the right insurance strategy doesn’t drain your business, it protects it from sinking. Especially in tough times.

Over the past few months, I’ve had conversations with business owners who’ve been navigating slower sales, rising costs, and unpredictable markets. Some of them have taken hits. Others are just trying to hold the line.

And here’s the pattern I’ve seen:

The ones who built proper risk protection into their financial plan, well before things got hard, have stayed afloat. Their families are protected. Their cash flow isn’t crippled. And their long-term goals haven’t been derailed.

Because when things go sideways, whether it’s a critical illness, a lawsuit, a sudden disability, or even an early death the right insurance solution can be the one thing that saves the business, the family, and the legacy you’ve worked so hard to build.

Here’s the key, though:

Protection can’t be built in isolation.

It needs to be part of a bigger plan that understands how your corporation operates, what your accountant is optimizing for, and how your legal structures are set up.

That’s where working with the right advisor matters.

I don’t just sell policies. I help business owners:

• Integrate protection into their corporate tax strategy

• Build legacy and succession plans that make sense

• Collaborate with their accountant, lawyer, and bookkeeper to ensure everything works together, not against each other

Whether it’s corporate-owned insurance for tax-efficient wealth transfer, buy-sell protection between partners, or a holding company strategy that supports retirement income down the road—it all starts with a plan that aligns with your goals and your business model.

If you’re building something that supports your family, your team, and your future…

Then now is the time to ask:

➡️ Is your business protected from the risks that could undo it all?

➡️ Have you built insurance into your offense strategy, not just as a backup?

➡️ Is your plan working hand-in-hand with your accountant and lawyer—or is it sitting in a drawer somewhere?

If the answer isn’t crystal clear, it might be time for a conversation.

Let’s build a plan that protects your hard work, honors your goals, and grows alongside your business.

📩 Send me a message if you want to chat. I’ll walk you through the same process we use with business owners to protect what matters, without overcomplicating things.

And if you’ve worked with me and know someone who needs this kind of support, I’d be grateful for the introduction.

#BusinessPlanning #LegacyPlanning #InsuranceForBusinessOwners #CorporateStrategy #TaxEfficiency #FamilyLegacy #WealthPlanning #Entrepreneurs

Have questions?

Here to help answer your questions, provide clarity about products and get you started on the road to achieving your goals.