Where Strategy Meets Your Scroll

You're busy running a business, raising a family and living your life - or all 3! We get it. That's exactly why we created a space where you can get real, practical financial insights without digging through confusing jargon or salesy fluff.

Our Instagram is built for people like you: entrepreneurs, professional and families who want to protect what they've built, grow what's next and create a legacy worth passing on. We break down the complex stuff - like taxes, investing, insurance and retirement into bite sized tips that actually make sense and fit your life.

From "why no one talks about corporate investing" to "how to spend smarter in retirement" our feed is full of strategy-backed advice that we'd give our own families (because we've been in your shoes).

Ready to go beyond the scroll? Tap the link below and book a meeting to see how we work differently... then follow us on Instagram to stay one step ahead, every step of the way.

✅ Max your RRSP.

✅ Invest what’s left.

✅ Hope it all works out.

The problem isn’t that an RRSP is bad.

The problem is when it becomes the only strategy.

Your RRSP has a job.

Your TFSA has a different job.

Your corporation has a different job.

Even your non-registered investments can have a completely different purpose.

The goal isn’t to find the best account.

The goal is to understand what job your next dollar needs to do.

That’s where proper planning changes everything.

Instead of asking…

“Should I max my RRSP?”

Start asking…

“Where should my next dollar create the most value?”

That’s the difference between collecting financial products…

…and building a connected strategy where every dollar has a purpose.

Comment RETIREMENT if you’d like to see how these different pieces can work together to create more tax-efficient retirement income.

✅ Max your RRSP.

✅ Invest what’s left.

✅ Hope it all works out.

The problem isn’t that an RRSP is bad.

The problem is when it becomes the only strategy.

Your RRSP has a job.

Your TFSA has a different job.

Your corporation has a different job.

Even your non-registered investments can have a completely different purpose.

The goal isn’t to find the best account.

The goal is to understand what job your next dollar needs to do.

That’s where proper planning changes everything.

Instead of asking…

“Should I max my RRSP?”

Start asking…

“Where should my next dollar create the most value?”

That’s the difference between collecting financial products…

…and building a connected strategy where every dollar has a purpose.

Comment RETIREMENT if you’d like to see how these different pieces can work together to create more tax-efficient retirement income.

For many Canadian business owners, that’s only one piece of the puzzle.

Your RRSP is an important tool.

So is your corporation.

So are your investments, your tax strategy, and how you plan to create income in retirement.

The question isn’t:

“Should I contribute to my RRSP?”

The better question is:

“What’s the best way to build retirement income for my situation?”

The answer is different for everyone.

That’s why good planning isn’t about following generic advice.

It’s about understanding how all the pieces work together.

You don’t need another retirement tip.

You need clarity.

Comment RETIREMENT if you’re a Canadian business owner who wants to understand how your corporation can fit into your long-term retirement strategy.

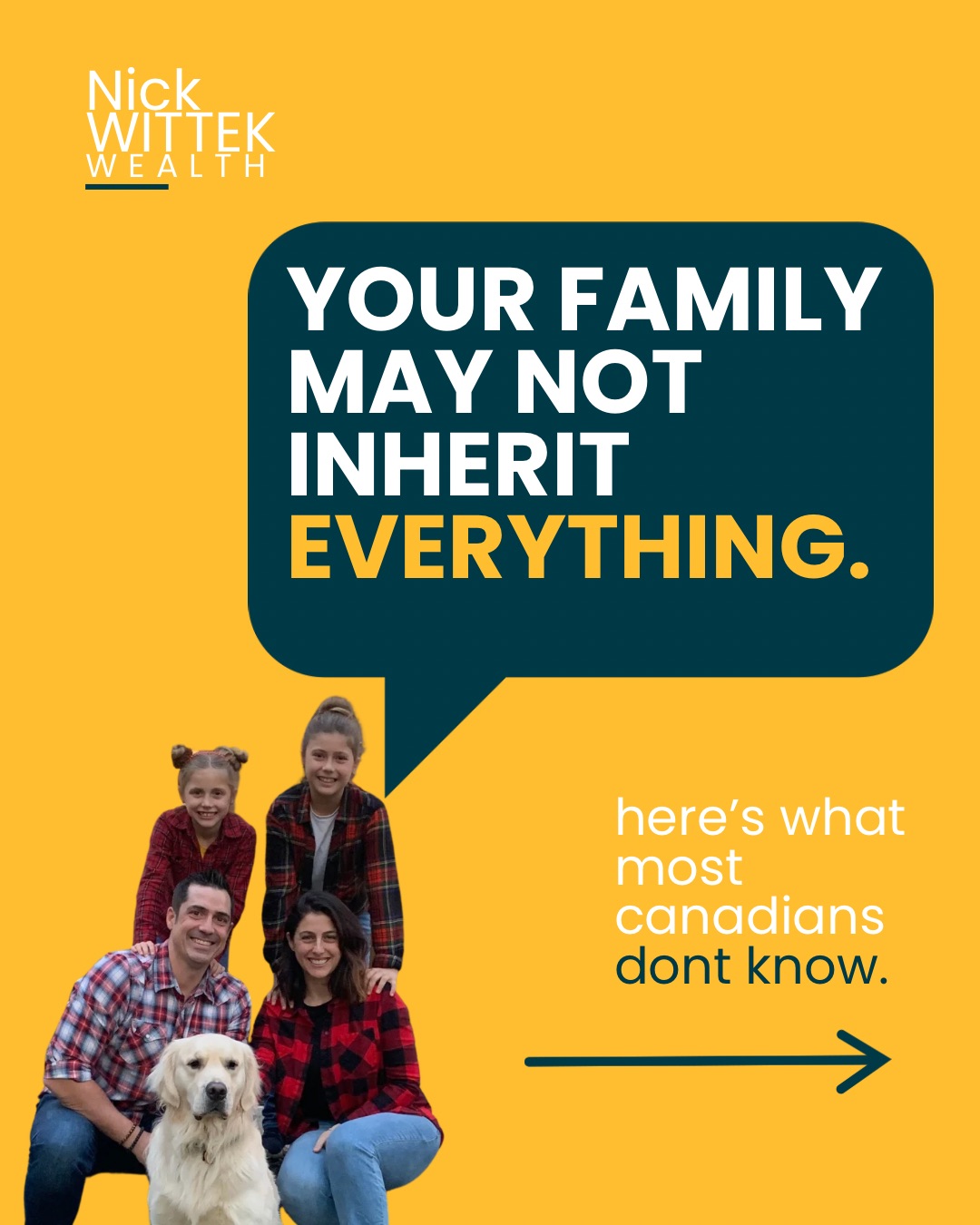

It doesn’t.

A will answers who gets your assets.

An estate plan answers the questions most people never think to ask.

What taxes could be triggered?

Will your family have enough cash to pay them?

Will they have to sell investments or property?

Could a business or family cottage have to be sold just to cover the tax bill?

That’s why estate planning isn’t about expecting the worst.

It’s about making sure the people you love aren’t left making difficult financial decisions while they’re grieving.

The best estate plans don’t happen by accident.

They happen by design.

You don’t need more information.

You need clarity.

Comment LEGACY and I’ll send you an invitation to an upcoming online conversation I’m hosting with an estate lawyer, where we’ll unpack wills, estate planning, tax planning, and the mistakes families don’t realize they’re making until it’s too late.

It doesn’t.

A will answers who gets your assets.

An estate plan answers the questions most people never think to ask.

What taxes could be triggered?

Will your family have enough cash to pay them?

Will they have to sell investments or property?

Could a business or family cottage have to be sold just to cover the tax bill?

That’s why estate planning isn’t about expecting the worst.

It’s about making sure the people you love aren’t left making difficult financial decisions while they’re grieving.

The best estate plans don’t happen by accident.

They happen by design.

You don’t need more information.

You need clarity.

Comment LEGACY and I’ll send you an invitation to an upcoming online conversation I’m hosting with an estate lawyer, where we’ll unpack wills, estate planning, tax planning, and the mistakes families don’t realize they’re making until it’s too late.

Without you actively working, revenue often slows or stops — but overhead doesn’t. Rent, payroll, and operating costs continue regardless of your ability to work.

Most owners insure their equipment more thoroughly than they insure themselves, despite being the primary driver of the business. This is why income and overhead protection is always the first step in any plan I build with a business owner — without the ability to earn, every other part of a financial plan becomes difficult to sustain.

#EstatePlanning #CorporateTaxPlanning #BusinessOwners #WealthTransfer #CanadianFinance

A shareholder agreement outlines what should happen — for example, buying out a deceased partner’s shares from their family. What it doesn’t answer is where that capital actually comes from. Most partnerships never work through that question until it’s urgent.

This is typically addressed with life insurance funding, ensuring the capital is available immediately when it’s needed, without loans, liquidation, or difficult negotiations during an already difficult time.

#EstatePlanning #CorporateTaxPlanning #BusinessOwners #WealthTransfer #CanadianFinance

That triggers capital gains tax on investments, real estate, and other holdings, often before your family receives anything. Most people aren’t aware this exposure exists until it’s already affecting their estate.

With proper planning, this tax liability can be anticipated and managed well in advance — rather than becoming a surprise for your family at the worst possible time.

#EstatePlanning #CorporateTaxPlanning #WealthTransfer #CanadianFinance #BusinessOwners

But here’s what people miss…

An agreement tells everyone what should happen.

It doesn’t tell you how you’re actually going to pay for it.

If one business owner passes away, the surviving owner still needs to buy those shares.

Where does that money come from?

Savings?

A loan?

Selling business assets?

Or was there already a plan in place?

That’s why properly funding a buy-sell agreement is just as important as having one in the first place.

Because the best plans don’t just look good on paper.

They work when life doesn’t go according to plan.

Swipe through the carousel, and ask yourself one question:

If something happened to my business partner tomorrow, do we actually have a plan… or just an agreement?

Comment PARTNER if you’d like to learn how business owners can protect their company, their families, and each other.

But here’s what people miss…

An agreement tells everyone what should happen.

It doesn’t tell you how you’re actually going to pay for it.

If one business owner passes away, the surviving owner still needs to buy those shares.

Where does that money come from?

Savings?

A loan?

Selling business assets?

Or was there already a plan in place?

That’s why properly funding a buy-sell agreement is just as important as having one in the first place.

Because the best plans don’t just look good on paper.

They work when life doesn’t go according to plan.

Swipe through the carousel, and ask yourself one question:

If something happened to my business partner tomorrow, do we actually have a plan… or just an agreement?

Comment PARTNER if you’d like to learn how business owners can protect their company, their families, and each other.

And to be clear, that’s not wrong. Your accountant is essential for filing, compliance, and keeping your books accurate. But that’s a fundamentally different function than proactive tax strategy.

Most accounting relationships are built around last year’s numbers — not what you could be structuring right now to reduce future exposure. That gap is where a lot of owners unknowingly leave money on the table.

Someone still needs to be looking forward, not just filing after the fact.

#EstatePlanning #CorporateTaxPlanning #BusinessOwners #WealthTransfer #CanadianFinance

“If you couldn’t work for the next six months, what would happen to your business?”

Most people answer with something like, “I’d figure it out.”

Maybe.

But let’s think it through.

Your revenue slows down—or stops completely.

Meanwhile, rent is still due.

Payroll doesn’t pause.

Loan payments continue.

Software subscriptions renew.

Utilities keep coming.

The business keeps spending money, even if you can’t generate it.

Here’s what’s interesting.

Most business owners have more insurance on their equipment than they do on themselves.

The truck is insured.

The office is insured.

The computers are insured.

But the person responsible for generating the revenue often isn’t.

That’s why I believe we’ve got financial planning backwards.

We spend a lot of time talking about investing, retirement, and growing wealth.

Those are important conversations.

They’re just not the first conversations.

The first conversation should always be about protecting the engine that makes everything else possible.

For most business owners…

You are the engine.

That’s why income protection and business overhead expense coverage are often the foundation of a strong business plan—not an afterthought.

I’d be curious to hear your perspective.

If you couldn’t work for six months, what part of your business would concern you the most?

“If you couldn’t work for the next six months, what would happen to your business?”

Most people answer with something like, “I’d figure it out.”

Maybe.

But let’s think it through.

Your revenue slows down—or stops completely.

Meanwhile, rent is still due.

Payroll doesn’t pause.

Loan payments continue.

Software subscriptions renew.

Utilities keep coming.

The business keeps spending money, even if you can’t generate it.

Here’s what’s interesting.

Most business owners have more insurance on their equipment than they do on themselves.

The truck is insured.

The office is insured.

The computers are insured.

But the person responsible for generating the revenue often isn’t.

That’s why I believe we’ve got financial planning backwards.

We spend a lot of time talking about investing, retirement, and growing wealth.

Those are important conversations.

They’re just not the first conversations.

The first conversation should always be about protecting the engine that makes everything else possible.

For most business owners…

You are the engine.

That’s why income protection and business overhead expense coverage are often the foundation of a strong business plan—not an afterthought.

I’d be curious to hear your perspective.

If you couldn’t work for six months, what part of your business would concern you the most?

You die.

Your family receives a tax-free benefit.

End of story.

That’s important.

But it’s not the whole story.

When structured properly, permanent life insurance can become much more than protection. It can become part of a broader corporate wealth strategy by creating liquidity, improving flexibility, and helping move wealth to the next generation in a tax-efficient way.

The mistake I see isn’t choosing the wrong product.

It’s starting with the product in the first place.

Before we talk about Term, Universal Life, or Participating Whole Life, we should be asking a much better question:

What job do you need this money to do?

The answer might be protecting your family.

It might be creating corporate liquidity.

It might be funding taxes at death.

It might be preserving wealth for the next generation.

The purpose should always determine the strategy.

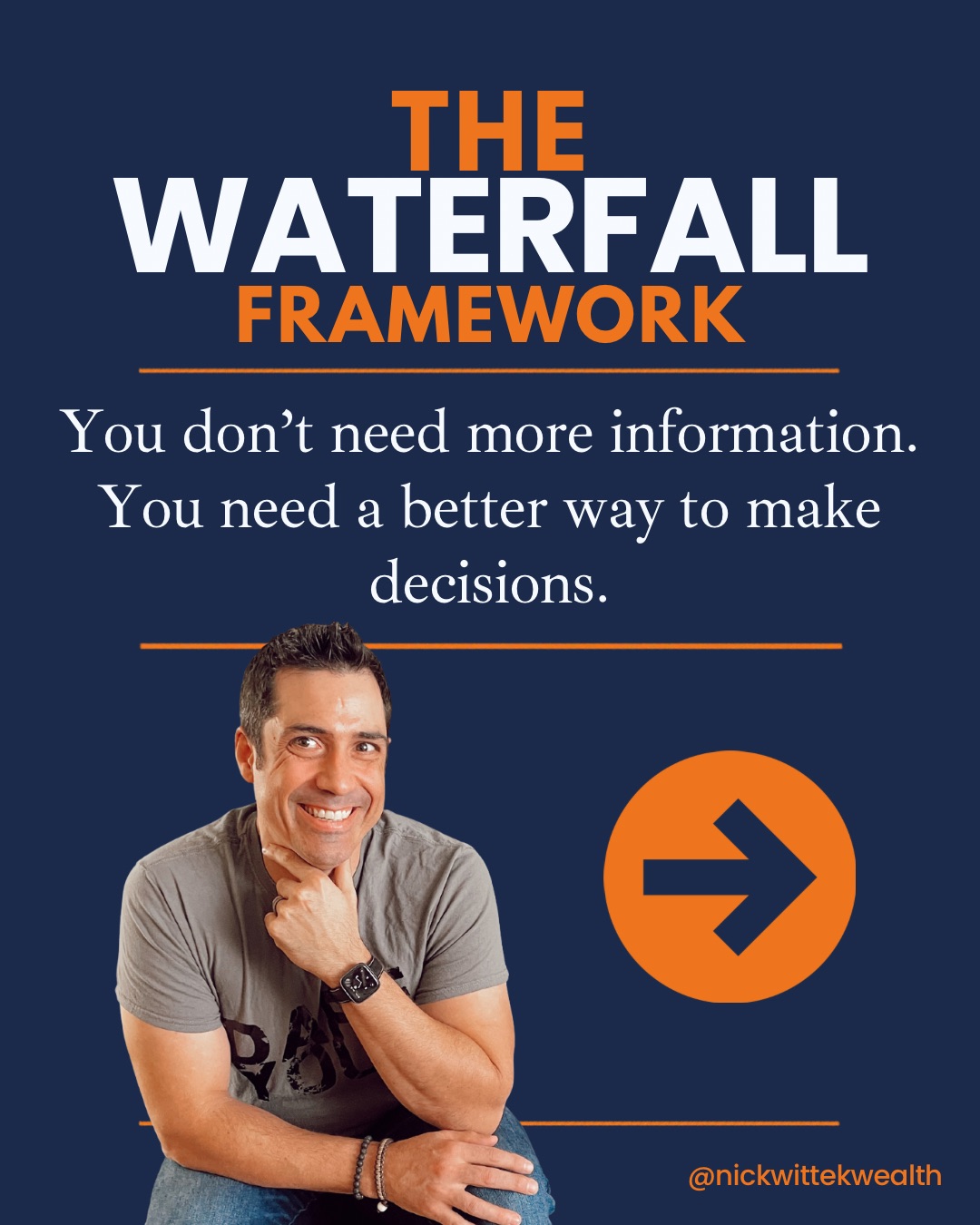

That’s the philosophy behind the Waterfall Framework. Every dollar should have a job, and every part of your financial plan should work together—not compete with each other.

How do you think about life insurance today: as protection, or as part of your overall financial strategy?

You die.

Your family receives a tax-free benefit.

End of story.

That’s important.

But it’s not the whole story.

When structured properly, permanent life insurance can become much more than protection. It can become part of a broader corporate wealth strategy by creating liquidity, improving flexibility, and helping move wealth to the next generation in a tax-efficient way.

The mistake I see isn’t choosing the wrong product.

It’s starting with the product in the first place.

Before we talk about Term, Universal Life, or Participating Whole Life, we should be asking a much better question:

What job do you need this money to do?

The answer might be protecting your family.

It might be creating corporate liquidity.

It might be funding taxes at death.

It might be preserving wealth for the next generation.

The purpose should always determine the strategy.

That’s the philosophy behind the Waterfall Framework. Every dollar should have a job, and every part of your financial plan should work together—not compete with each other.

How do you think about life insurance today: as protection, or as part of your overall financial strategy?

A bit going into the RRSP. Some money sitting in the corp. A real estate investment here. A market account there. Maybe some cash reserves tucked away somewhere.

Each decision made sense on its own at the time. But nobody ever stepped back and asked whether any of it was actually working together.

And that’s where the problem lives.

When your money is scattered across strategies with no coordinated structure behind them, every dollar is doing a different job — which means no dollar is doing its job properly.

It’s not a laziness problem. It’s not even a knowledge problem. It’s a structure problem.

Real wealth planning isn’t about how many places your money is. It’s about whether those places are connected, coordinated, and pulling in the same direction.

Protection first. Tax strategy built around that. Then investing and long term wealth building layered in properly.

A bit going into the RRSP. Some money sitting in the corp. A real estate investment here. A market account there. Maybe some cash reserves tucked away somewhere.

Each decision made sense on its own at the time. But nobody ever stepped back and asked whether any of it was actually working together.

And that’s where the problem lives.

When your money is scattered across strategies with no coordinated structure behind them, every dollar is doing a different job — which means no dollar is doing its job properly.

It’s not a laziness problem. It’s not even a knowledge problem. It’s a structure problem.

Real wealth planning isn’t about how many places your money is. It’s about whether those places are connected, coordinated, and pulling in the same direction.

Protection first. Tax strategy built around that. Then investing and long term wealth building layered in properly.

It’s asking the wrong question.

I often hear:

“Where should my next dollar go?”

Into the corporation?

Into the market?

Real estate?

Pay down debt?

The truth is, none of those answers are automatically right or wrong.

The real question is:

What job does that dollar need to do first?

That’s the thinking behind The Waterfall Framework for the Planning Process.

Every financial decision should build on the one before it.

First, create stability through healthy cash flow.

Then protect what you’ve built so one unexpected event doesn’t derail years of work.

Only then does it make sense to focus on long term wealth creation.

Finally, ensure that wealth creates the impact you want through retirement, succession, and legacy planning.

When each decision flows into the next, your financial strategy becomes connected instead of reactive.

Business owners don’t need more opinions.

They need a process that helps them make better decisions with confidence.

That’s exactly what The Waterfall Framework is designed to do.

What financial decision do you think business owners rush into before they’re truly ready?

It’s asking the wrong question.

I often hear:

“Where should my next dollar go?”

Into the corporation?

Into the market?

Real estate?

Pay down debt?

The truth is, none of those answers are automatically right or wrong.

The real question is:

What job does that dollar need to do first?

That’s the thinking behind The Waterfall Framework for the Planning Process.

Every financial decision should build on the one before it.

First, create stability through healthy cash flow.

Then protect what you’ve built so one unexpected event doesn’t derail years of work.

Only then does it make sense to focus on long term wealth creation.

Finally, ensure that wealth creates the impact you want through retirement, succession, and legacy planning.

When each decision flows into the next, your financial strategy becomes connected instead of reactive.

Business owners don’t need more opinions.

They need a process that helps them make better decisions with confidence.

That’s exactly what The Waterfall Framework is designed to do.

What financial decision do you think business owners rush into before they’re truly ready?

You’ve built the business. Taken the risks. Put in the work.

Now there’s capital in the corporation, and suddenly everyone has an opinion.

Invest it.

Buy real estate.

Leave it in the company.

Take it out.

Pay down debt.

The interesting part is that none of those suggestions are inherently wrong.

They’re simply answers.

The problem is that many business owners haven’t stopped to define the question they’re trying to answer.

Are you building financial independence?

Creating flexibility for your family?

Preparing for retirement?

Planning for a future business sale?

Reducing risk?

Leaving a legacy?

Without a clear objective, it’s easy to collect good advice that pulls you in different directions.

The most effective strategies don’t start with products or investments.

They start with purpose.

When you’re clear on what you want your money to accomplish, every other decision becomes easier to evaluate.

That’s the difference between collecting opinions and building a strategy.

What’s the first question you think every business owner should ask before deciding where their money goes?

You’ve built the business. Taken the risks. Put in the work.

Now there’s capital in the corporation, and suddenly everyone has an opinion.

Invest it.

Buy real estate.

Leave it in the company.

Take it out.

Pay down debt.

The interesting part is that none of those suggestions are inherently wrong.

They’re simply answers.

The problem is that many business owners haven’t stopped to define the question they’re trying to answer.

Are you building financial independence?

Creating flexibility for your family?

Preparing for retirement?

Planning for a future business sale?

Reducing risk?

Leaving a legacy?

Without a clear objective, it’s easy to collect good advice that pulls you in different directions.

The most effective strategies don’t start with products or investments.

They start with purpose.

When you’re clear on what you want your money to accomplish, every other decision becomes easier to evaluate.

That’s the difference between collecting opinions and building a strategy.

What’s the first question you think every business owner should ask before deciding where their money goes?

They have a clarity problem.

Once you’ve built a successful business and started accumulating wealth, the advice never stops.

Buy real estate.

Invest in the market.

Pay off debt.

Keep it in the corporation.

Take it out.

Everyone has an opinion.

Here’s what people miss:

The right strategy depends on what you’re trying to accomplish.

Before deciding where the money should go, get clear on what you want it to do.

More freedom.

More options.

Earlier retirement.

Supporting your children.

Building a legacy.

That’s the difference.

You don’t need more information. You need clarity.

Comment WEALTH to build yours.

#BusinessOwners #CorporatePlanning #WealthBuilding #LegacyPlanning #Entrepreneur

It’s a lack of clarity.

Every day, there are decisions to make:

Should money stay in the corporation?

Should it be invested?

Should debt be paid down?

Should more protection be put in place?

Should we focus on retirement or legacy planning?

The problem is that most of these decisions are made independently.

The investment strategy lives in one silo.

The protection strategy lives in another.

Tax planning becomes a separate conversation.

Estate planning gets pushed off until later.

What I have found is that the best outcomes happen when those conversations are connected.

That’s why we built the Waterfall Framework.

A process designed to help business owners and families connect protection, tax strategy, wealth building, retirement planning, and legacy planning into one coordinated strategy.

Because the goal isn’t to collect more financial products.

The goal is to make better decisions.

And better decisions happen when every piece is working toward the same objective.

What financial decision do you find business owners struggle with most?

It’s a lack of clarity.

Every day, there are decisions to make:

Should money stay in the corporation?

Should it be invested?

Should debt be paid down?

Should more protection be put in place?

Should we focus on retirement or legacy planning?

The problem is that most of these decisions are made independently.

The investment strategy lives in one silo.

The protection strategy lives in another.

Tax planning becomes a separate conversation.

Estate planning gets pushed off until later.

What I have found is that the best outcomes happen when those conversations are connected.

That’s why we built the Waterfall Framework.

A process designed to help business owners and families connect protection, tax strategy, wealth building, retirement planning, and legacy planning into one coordinated strategy.

Because the goal isn’t to collect more financial products.

The goal is to make better decisions.

And better decisions happen when every piece is working toward the same objective.

What financial decision do you find business owners struggle with most?

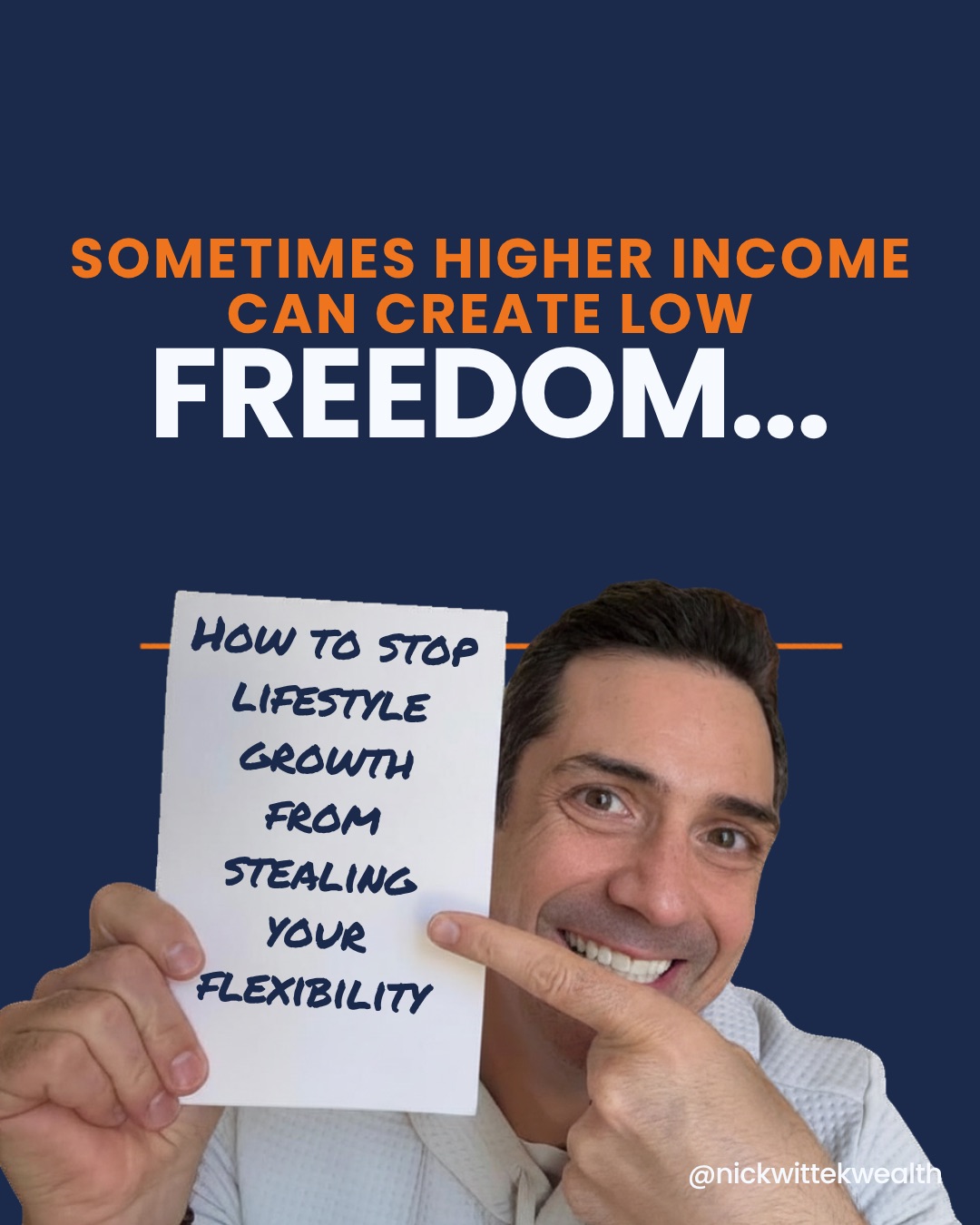

It is a lifestyle expansion problem.

As income rises, fixed expenses often rise immediately alongside it:

• larger homes

• higher vehicle payments

• increased overhead

• expanded lifestyle expectations

Over time, this can quietly reduce flexibility and increase long term financial pressure despite strong earnings.

The issue is rarely the lifestyle upgrade itself.

The issue is whether assets, liquidity, and financial structure are growing at the same pace.

One of the most valuable shifts for business owners and professionals is learning to increase:

• flexibility

• investment capacity

• cash reserves

• intentional cash flow

before allowing every raise to become a permanent obligation.

Because long term wealth is not just about income.

It is about maintaining options and control as life evolves.

#CanadianBusiness #CanadianEntrepreneur #WealthStrategy #CorporatePlanning #CanadianFinance

It is a lifestyle expansion problem.

As income rises, fixed expenses often rise immediately alongside it:

• larger homes

• higher vehicle payments

• increased overhead

• expanded lifestyle expectations

Over time, this can quietly reduce flexibility and increase long term financial pressure despite strong earnings.

The issue is rarely the lifestyle upgrade itself.

The issue is whether assets, liquidity, and financial structure are growing at the same pace.

One of the most valuable shifts for business owners and professionals is learning to increase:

• flexibility

• investment capacity

• cash reserves

• intentional cash flow

before allowing every raise to become a permanent obligation.

Because long term wealth is not just about income.

It is about maintaining options and control as life evolves.

#CanadianBusiness #CanadianEntrepreneur #WealthStrategy #CorporatePlanning #CanadianFinance

Most people think waiting is harmless because nothing changes overnight. But over time, delays can quietly become expensive.

Tax exposure increases.

Retirement timelines shift.

Protection gaps stay open.

And financial flexibility starts to disappear.

That’s why strong financial planning is not just about growing wealth. It’s about creating a clear strategy that protects your future options before they shrink.

For incorporated professionals, business owners, and families building long term wealth, having a tax efficient plan matters. The right structure can help reduce unnecessary tax, protect your family, support retirement income planning, and create a stronger legacy for future generations.

The goal is not just more information.

It’s clarity, direction, and a plan that evolves with your life.

Most people think waiting is harmless because nothing changes overnight. But over time, delays can quietly become expensive.

Tax exposure increases.

Retirement timelines shift.

Protection gaps stay open.

And financial flexibility starts to disappear.

That’s why strong financial planning is not just about growing wealth. It’s about creating a clear strategy that protects your future options before they shrink.

For incorporated professionals, business owners, and families building long term wealth, having a tax efficient plan matters. The right structure can help reduce unnecessary tax, protect your family, support retirement income planning, and create a stronger legacy for future generations.

The goal is not just more information.

It’s clarity, direction, and a plan that evolves with your life.

It’s not.

Your TFSA is one of the most underutilized wealth building tools available to Canadian business owners.

Every dollar that grows inside it is completely tax free.

Every dollar you withdraw is completely tax free. No income inclusion. No CRA. No catch.

For incorporated business owners in Ontario the TFSA becomes even more powerful when coordinated alongside your corporate structure and RRSP withdrawal strategy.

The problem isn’t access. It’s awareness.

Swipe through for 5 things they never told you about your TFSA.

Which one surprised you most?

Own your plan. Own the outcome.

#GenerationalWealth #LegacyPlanning #CanadianWealth #WealthManagement #BusinessOwners

It’s not.

Your TFSA is one of the most underutilized wealth building tools available to Canadian business owners.

Every dollar that grows inside it is completely tax free.

Every dollar you withdraw is completely tax free. No income inclusion. No CRA. No catch.

For incorporated business owners in Ontario the TFSA becomes even more powerful when coordinated alongside your corporate structure and RRSP withdrawal strategy.

The problem isn’t access. It’s awareness.

Swipe through for 5 things they never told you about your TFSA.

Which one surprised you most?

Own your plan. Own the outcome.

#GenerationalWealth #LegacyPlanning #CanadianWealth #WealthManagement #BusinessOwners

But here’s what most people were never told.

Every dollar sitting in that account is still owed to CRA.

You didn’t eliminate the tax. You deferred it.

And without a clear strategy for how and when to withdraw — that deferral could cost you significantly more in retirement than you ever saved contributing to it.

For Ontario business owners especially — your RRSP can’t sit in isolation. It needs to work alongside your TFSA, your corporate structure and your estate plan. Without that coordination you’re not building a plan.

You’re building a problem.

Swipe through for the 5 things they never told you about your RRSP.

Which one surprised you most?

Own your plan. Own the outcome.

#GenerationalWealth #LegacyPlanning

#CanadianWealth #WealthManagement #BusinessOwners

But here’s what most people were never told.

Every dollar sitting in that account is still owed to CRA.

You didn’t eliminate the tax. You deferred it.

And without a clear strategy for how and when to withdraw — that deferral could cost you significantly more in retirement than you ever saved contributing to it.

For Ontario business owners especially — your RRSP can’t sit in isolation. It needs to work alongside your TFSA, your corporate structure and your estate plan. Without that coordination you’re not building a plan.

You’re building a problem.

Swipe through for the 5 things they never told you about your RRSP.

Which one surprised you most?

Own your plan. Own the outcome.

#GenerationalWealth #LegacyPlanning

#CanadianWealth #WealthManagement #BusinessOwners

Insurance can seem complicated (it doesn't need to be) and most people either think they are fully covered, or they don't want it at all... Until they really understand what they have and what they need.

Term coverage protects your family for a lower coast in the short term.

Mortgage insurance coverage protects what is owning on your house, but nothing more than that.

Work coverage helps, but that is the icing on the cake as the coverage is tied to your employer - change in work means change or loss of coverage.

The problem isn't the coverage itself. It's understanding how it works, how it fits together and whether it truly protects the people and lifestyle you care about.

Our focus is to simplify these conversations so business owners and families can make confident, intentional choice that help build lasting legacies.

Wealth and legacy don't happen by accident, they happen by strategy.

Comment WEALTH or DM me to build yours.

Insurance can seem complicated (it doesn't need to be) and most people either think they are fully covered, or they don't want it at all... Until they really understand what they have and what they need.

Term coverage protects your family for a lower coast in the short term.

Mortgage insurance coverage protects what is owning on your house, but nothing more than that.

Work coverage helps, but that is the icing on the cake as the coverage is tied to your employer - change in work means change or loss of coverage.

The problem isn't the coverage itself. It's understanding how it works, how it fits together and whether it truly protects the people and lifestyle you care about.

Our focus is to simplify these conversations so business owners and families can make confident, intentional choice that help build lasting legacies.

Wealth and legacy don't happen by accident, they happen by strategy.

Comment WEALTH or DM me to build yours.

Have questions?

Here to help answer your questions, provide clarity about products and get you started on the road to achieving your goals.