Steven Good

Job title: Financial Planner, Sun Life, Adm.A., B. Comm (Hons), B.A., B.A. (Finance), CA, CFA, CFP®, CHS™

A.Sc., AAMS, ACAS, B.A., B.A. (Finance)

Languages spoken: English, French, German, Spanish

Area(s) served: Kitchener-Waterloo-Toronto

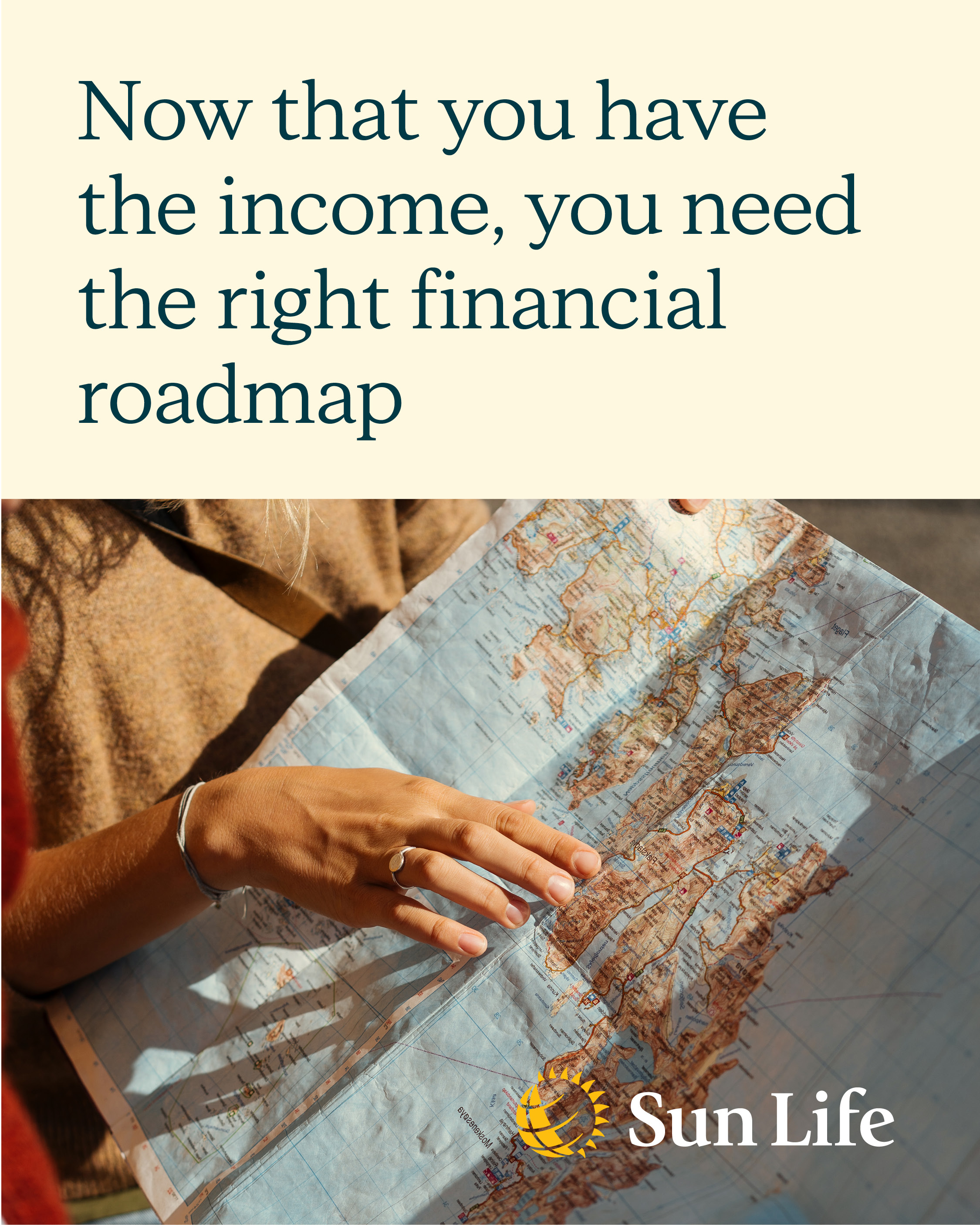

Trustworthy advice you can count on

Your financial strategy should be as unique as you are. Whether you’re just starting out, about to enter retirement, or somewhere in between, a strong financial roadmap can help you reach your short and long-term goals. Let’s work together to protect what matters most to you and help you secure your future. Reach out to get started. Let’s get you there.

Who we service

Learn more

Families

Investments

Millennials

My Story

Building successful partnerships

Relationships can be instrumental in helping you plan their financial future effectively. Our personalized partnerships allow us to gain understanding of you unique financial situation, goals, and risk tolerance. By tailoring strategies to individual needs, we can provide targeted guidance on investment choices, retirement planning, tax optimization, and estate planning. They can also help you navigate complex financial decisions, adjust plans as life circumstances change, and stay accountable to your long-term objectives. Regular meetings and open communication ensure that you remain informed and confident in your financial journey, while our expertise helps mitigate risks and capitalize on opportunities. This personalized approach often leads to more comprehensive and successful financial planning outcomes.

Products and services

Business owners

Mortgage protection insurance

Saving, budgeting and investing

Get to know us

The solutions team at Sample Financial works to address all your needs. The team consists of 5 specialists who each bring a unique set of skills to better serve Clients.

- A written financial plan increases confidence.

- A financial plan can jumpstart savings, even with a small amount of money.

- A financial plan can help you create an investment portfolio.

- A financial plan can lead to better habits.

Together this diverse group can offer full-service solutions that address every aspect of a Client's partnership us.

Watch this video to learn more about how we can help you.

Stay informed

See more articles

Voyons ensemble comment un bilan printanier peut faire fleurir vos finances. Le printemps est arrivé!

Voyons ensemble comment un bilan printanier peut faire fleurir vos finances. Le printemps est arrivé!

Test 6 min

Steven Good | Sun Life

Prescillia Chanteur

https://advisor.sunlife.ca/sg/

https://conseiller.sunlife.ca/jeanbrunet