Stay informed

Stay informed with what’s going on. Browse posts that might be helpful to you or check out an event happening in your area. Come back regularly as this page is kept up-to-date with a lot of relevant information.

Our office will be closed Friday, July 31 and Monday, August 3 for the long weekend.

We'll be back in the office and ready to assist you on Tuesday, August 4.

We hope you and your family have a safe and enjoyable long weekend!

We'll be back in the office and ready to assist you on Tuesday, August 4.

We hope you and your family have a safe and enjoyable long weekend!

Our office will be closed Friday, July 31 and Monday, August 3 for the long weekend.

We'll be back in the office and ready to assist you on Tuesday, August 4.

We hope you and your family have a safe and enjoyable long weekend!

We'll be back in the office and ready to assist you on Tuesday, August 4.

We hope you and your family have a safe and enjoyable long weekend!

“We’ll figure it out later.”

“The farm will pass to the kids.”

“There’s more than enough.”

Then suddenly:

• A massive tax bill

• Not enough cash

• Pressure to sell land

• Unequal inheritances

• Family conflict nobody saw coming

What’s fair is not always equal. And those conversations get very real, very fast.

Life insurance creates immediate liquidity without forcing the sale of farmland, equipment, or assets the family spent generations building.

The worst time to build a succession plan is when health changes, options disappear, or emotions are already involved.

If your transition plan only exists in your head, you do not have a plan yet.

“The farm will pass to the kids.”

“There’s more than enough.”

Then suddenly:

• A massive tax bill

• Not enough cash

• Pressure to sell land

• Unequal inheritances

• Family conflict nobody saw coming

What’s fair is not always equal. And those conversations get very real, very fast.

Life insurance creates immediate liquidity without forcing the sale of farmland, equipment, or assets the family spent generations building.

The worst time to build a succession plan is when health changes, options disappear, or emotions are already involved.

If your transition plan only exists in your head, you do not have a plan yet.

“We’ll figure it out later.”

“The farm will pass to the kids.”

“There’s more than enough.”

Then suddenly:

• A massive tax bill

• Not enough cash

• Pressure to sell land

• Unequal inheritances

• Family conflict nobody saw coming

What’s fair is not always equal. And those conversations get very real, very fast.

Life insurance creates immediate liquidity without forcing the sale of farmland, equipment, or assets the family spent generations building.

The worst time to build a succession plan is when health changes, options disappear, or emotions are already involved.

If your transition plan only exists in your head, you do not have a plan yet.

“The farm will pass to the kids.”

“There’s more than enough.”

Then suddenly:

• A massive tax bill

• Not enough cash

• Pressure to sell land

• Unequal inheritances

• Family conflict nobody saw coming

What’s fair is not always equal. And those conversations get very real, very fast.

Life insurance creates immediate liquidity without forcing the sale of farmland, equipment, or assets the family spent generations building.

The worst time to build a succession plan is when health changes, options disappear, or emotions are already involved.

If your transition plan only exists in your head, you do not have a plan yet.

Here’s the issue with traditional creditor insurance on farm debt:

The insurance pays the lender directly. That may clear the loan, but it can limit how much control the family and farm corporation have afterward.

A properly structured corporate-owned life insurance strategy creates far more flexibility:

• Protect the operation

• Preserve working capital

• Potentially create Capital Dividend Account (CDA) credits

• Allow surviving family members to make decisions based on what’s best for the farm, not just the lender

The difference between “loan protection” and “business protection” becomes very real and this is why insurance planning for farms and incorporated businesses needs to go deeper than simply checking a box at the bank.

If you own a farm or business corporation, it’s worth reviewing how your current coverage is actually structured.

The insurance pays the lender directly. That may clear the loan, but it can limit how much control the family and farm corporation have afterward.

A properly structured corporate-owned life insurance strategy creates far more flexibility:

• Protect the operation

• Preserve working capital

• Potentially create Capital Dividend Account (CDA) credits

• Allow surviving family members to make decisions based on what’s best for the farm, not just the lender

The difference between “loan protection” and “business protection” becomes very real and this is why insurance planning for farms and incorporated businesses needs to go deeper than simply checking a box at the bank.

If you own a farm or business corporation, it’s worth reviewing how your current coverage is actually structured.

Here’s the issue with traditional creditor insurance on farm debt:

The insurance pays the lender directly. That may clear the loan, but it can limit how much control the family and farm corporation have afterward.

A properly structured corporate-owned life insurance strategy creates far more flexibility:

• Protect the operation

• Preserve working capital

• Potentially create Capital Dividend Account (CDA) credits

• Allow surviving family members to make decisions based on what’s best for the farm, not just the lender

The difference between “loan protection” and “business protection” becomes very real and this is why insurance planning for farms and incorporated businesses needs to go deeper than simply checking a box at the bank.

If you own a farm or business corporation, it’s worth reviewing how your current coverage is actually structured.

The insurance pays the lender directly. That may clear the loan, but it can limit how much control the family and farm corporation have afterward.

A properly structured corporate-owned life insurance strategy creates far more flexibility:

• Protect the operation

• Preserve working capital

• Potentially create Capital Dividend Account (CDA) credits

• Allow surviving family members to make decisions based on what’s best for the farm, not just the lender

The difference between “loan protection” and “business protection” becomes very real and this is why insurance planning for farms and incorporated businesses needs to go deeper than simply checking a box at the bank.

If you own a farm or business corporation, it’s worth reviewing how your current coverage is actually structured.

Most business owners don't have a backup plan. They assume things will keep working, until they don't.

No protection. No cushion. No plan.

If something disrupted your business tomorrow, would it survive?

No protection. No cushion. No plan.

If something disrupted your business tomorrow, would it survive?

Most business owners don't have a backup plan. They assume things will keep working, until they don't.

No protection. No cushion. No plan.

If something disrupted your business tomorrow, would it survive?

No protection. No cushion. No plan.

If something disrupted your business tomorrow, would it survive?

You don't just protect a mortgage.

You protect the people living in the home.

If your income disappeared tomorrow, what happens to your home?

You protect the people living in the home.

If your income disappeared tomorrow, what happens to your home?

You don't just protect a mortgage.

You protect the people living in the home.

If your income disappeared tomorrow, what happens to your home?

You protect the people living in the home.

If your income disappeared tomorrow, what happens to your home?

Changing jobs or wrapping up your career? Let's talk about transitioning your group investments smoothly and planning for what's next.

#CareerTransition #InvestmentPlanning

#CareerTransition #InvestmentPlanning

Last summer, we shared a behind-the-scenes look at an exciting project we were working on. Now we’re proud to share it with you.

This video captures how we approach planning, and what matters most to us when working with Clients.

A big thank you to the Clients who stepped up and were part of this. We appreciate your trust and willingness to be involved.

If you’ve ever wondered what working with us actually looks like, this is a great place to start.

This video captures how we approach planning, and what matters most to us when working with Clients.

A big thank you to the Clients who stepped up and were part of this. We appreciate your trust and willingness to be involved.

If you’ve ever wondered what working with us actually looks like, this is a great place to start.

Watch video

Last summer, we shared a behind-the-scenes look at an exciting project we were working on. Now we’re proud to share it with you.

This video captures how we approach planning, and what matters most to us when working with Clients.

A big thank you to the Clients who stepped up and were part of this. We appreciate your trust and willingness to be involved.

If you’ve ever wondered what working with us actually looks like, this is a great place to start.

This video captures how we approach planning, and what matters most to us when working with Clients.

A big thank you to the Clients who stepped up and were part of this. We appreciate your trust and willingness to be involved.

If you’ve ever wondered what working with us actually looks like, this is a great place to start.

Watch video

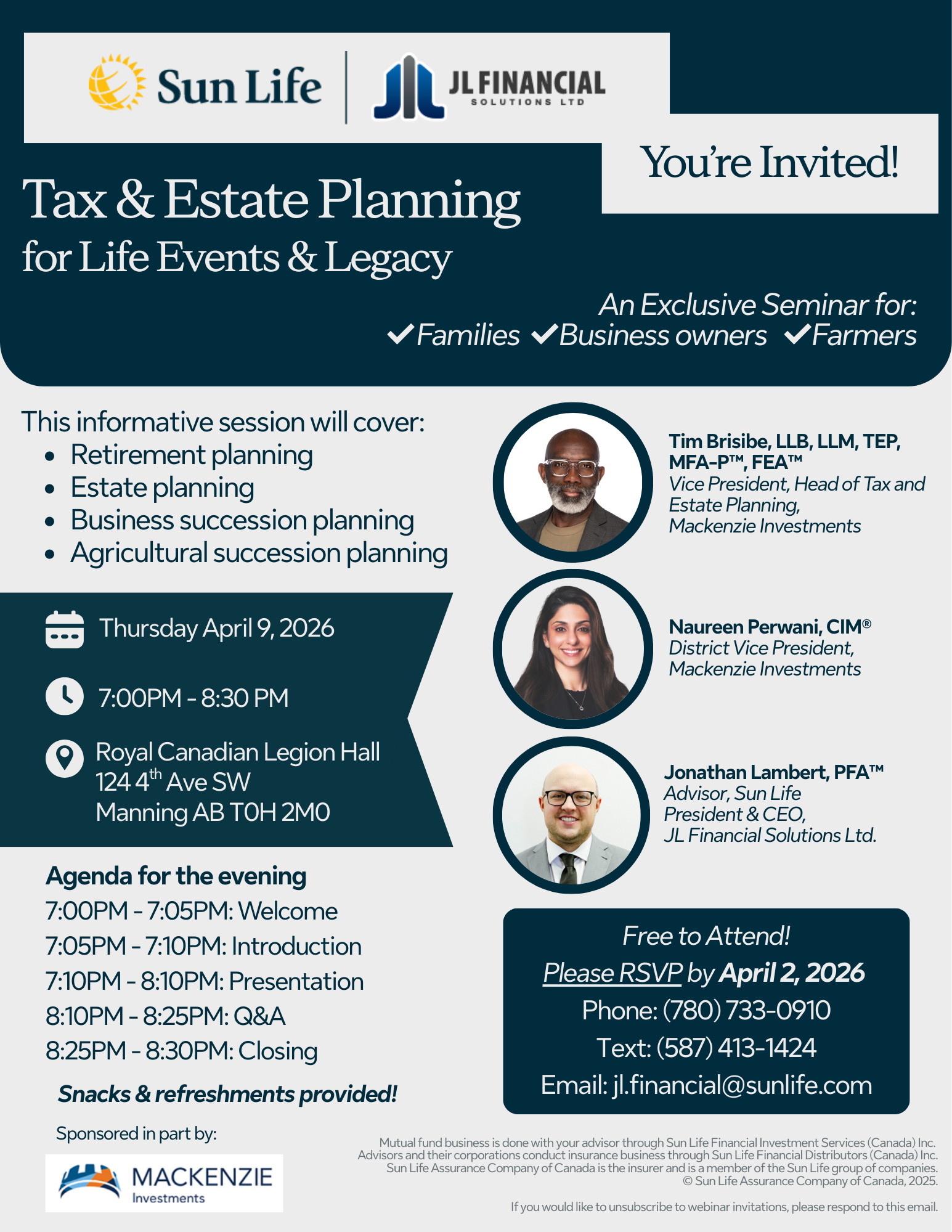

Planning for the future isn’t about “if.” It’s about “when.”

Retirement, business transition, farm succession, and estate distribution are realities every family and business will face. The real challenge is ensuring your plan works the way you intend when those moments arrive.

Next month, we’re hosting an in‑person Tax & Estate Planning seminar in Manning, featuring insights from Mackenzie Investments’ tax and estate specialists. We’ll be exploring practical strategies for retirement planning, business and agricultural succession, and building a legacy that lasts.

It’s an important conversation for families, business owners, and farmers who want clarity and confidence in their long‑term planning.

Retirement, business transition, farm succession, and estate distribution are realities every family and business will face. The real challenge is ensuring your plan works the way you intend when those moments arrive.

Next month, we’re hosting an in‑person Tax & Estate Planning seminar in Manning, featuring insights from Mackenzie Investments’ tax and estate specialists. We’ll be exploring practical strategies for retirement planning, business and agricultural succession, and building a legacy that lasts.

It’s an important conversation for families, business owners, and farmers who want clarity and confidence in their long‑term planning.

Planning for the future isn’t about “if.” It’s about “when.”

Retirement, business transition, farm succession, and estate distribution are realities every family and business will face. The real challenge is ensuring your plan works the way you intend when those moments arrive.

Next month, we’re hosting an in‑person Tax & Estate Planning seminar in Manning, featuring insights from Mackenzie Investments’ tax and estate specialists. We’ll be exploring practical strategies for retirement planning, business and agricultural succession, and building a legacy that lasts.

It’s an important conversation for families, business owners, and farmers who want clarity and confidence in their long‑term planning.

Retirement, business transition, farm succession, and estate distribution are realities every family and business will face. The real challenge is ensuring your plan works the way you intend when those moments arrive.

Next month, we’re hosting an in‑person Tax & Estate Planning seminar in Manning, featuring insights from Mackenzie Investments’ tax and estate specialists. We’ll be exploring practical strategies for retirement planning, business and agricultural succession, and building a legacy that lasts.

It’s an important conversation for families, business owners, and farmers who want clarity and confidence in their long‑term planning.

Today our office is closed for Family Day.

Whether related by blood or by choice, family is about the people who steady you and show up when it matters.

We'll be back in the office tomorrow, February 17th.

Enjoy the day with the people who matter most!

Whether related by blood or by choice, family is about the people who steady you and show up when it matters.

We'll be back in the office tomorrow, February 17th.

Enjoy the day with the people who matter most!

Today our office is closed for Family Day.

Whether related by blood or by choice, family is about the people who steady you and show up when it matters.

We'll be back in the office tomorrow, February 17th.

Enjoy the day with the people who matter most!

Whether related by blood or by choice, family is about the people who steady you and show up when it matters.

We'll be back in the office tomorrow, February 17th.

Enjoy the day with the people who matter most!

Thoughtful planning ensures your assets reach the right people at the right time — with minimal tax impact. Key considerations include:

-Estate planning strategies

-Tax-efficient wealth transfer

-Protecting family harmony

-Preserving your legacy

Start planning today for a seamless transition tomorrow. https://advisor.sunlife.ca/jl.financial/

-Estate planning strategies

-Tax-efficient wealth transfer

-Protecting family harmony

-Preserving your legacy

Start planning today for a seamless transition tomorrow. https://advisor.sunlife.ca/jl.financial/

Thoughtful planning ensures your assets reach the right people at the right time — with minimal tax impact. Key considerations include:

-Estate planning strategies

-Tax-efficient wealth transfer

-Protecting family harmony

-Preserving your legacy

Start planning today for a seamless transition tomorrow. https://advisor.sunlife.ca/jl.financial/

-Estate planning strategies

-Tax-efficient wealth transfer

-Protecting family harmony

-Preserving your legacy

Start planning today for a seamless transition tomorrow. https://advisor.sunlife.ca/jl.financial/

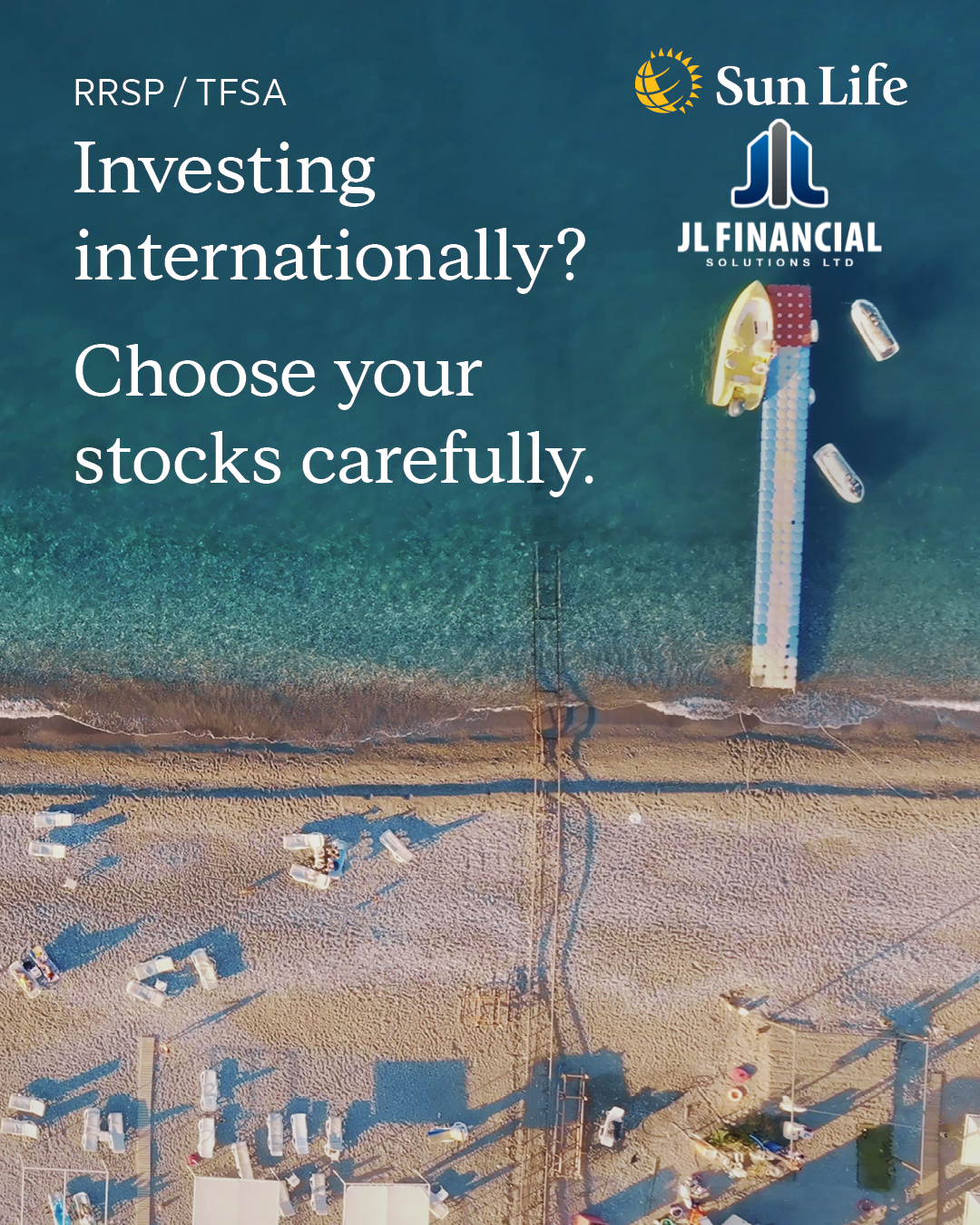

Investing in Canadian or U.S. stocks? Here's what you need to know:

TFSA:

- Canadian stocks: gains and dividends are tax-free.

- U.S. stocks: there’s a 15% withholding tax on dividends.

RRSP:

- There’s no withholding tax on U.S. stock dividends.

- Future withdrawals will be taxed as ordinary income.

Want to optimize your retirement savings? Let's talk about your RRSP and TFSA strategy.

TFSA:

- Canadian stocks: gains and dividends are tax-free.

- U.S. stocks: there’s a 15% withholding tax on dividends.

RRSP:

- There’s no withholding tax on U.S. stock dividends.

- Future withdrawals will be taxed as ordinary income.

Want to optimize your retirement savings? Let's talk about your RRSP and TFSA strategy.

Investing in Canadian or U.S. stocks? Here's what you need to know:

TFSA:

- Canadian stocks: gains and dividends are tax-free.

- U.S. stocks: there’s a 15% withholding tax on dividends.

RRSP:

- There’s no withholding tax on U.S. stock dividends.

- Future withdrawals will be taxed as ordinary income.

Want to optimize your retirement savings? Let's talk about your RRSP and TFSA strategy.

TFSA:

- Canadian stocks: gains and dividends are tax-free.

- U.S. stocks: there’s a 15% withholding tax on dividends.

RRSP:

- There’s no withholding tax on U.S. stock dividends.

- Future withdrawals will be taxed as ordinary income.

Want to optimize your retirement savings? Let's talk about your RRSP and TFSA strategy.

Whether navigating business/farm succession, protecting family wealth or maximizing tax efficiency, we help ensure your legacy reflects your current vision and helps protect what matters most.

Ready to review your plan? Reach out today. https://advisor.sunlife.ca/jl.financial/

Ready to review your plan? Reach out today. https://advisor.sunlife.ca/jl.financial/

Whether navigating business/farm succession, protecting family wealth or maximizing tax efficiency, we help ensure your legacy reflects your current vision and helps protect what matters most.

Ready to review your plan? Reach out today. https://advisor.sunlife.ca/jl.financial/

Ready to review your plan? Reach out today. https://advisor.sunlife.ca/jl.financial/

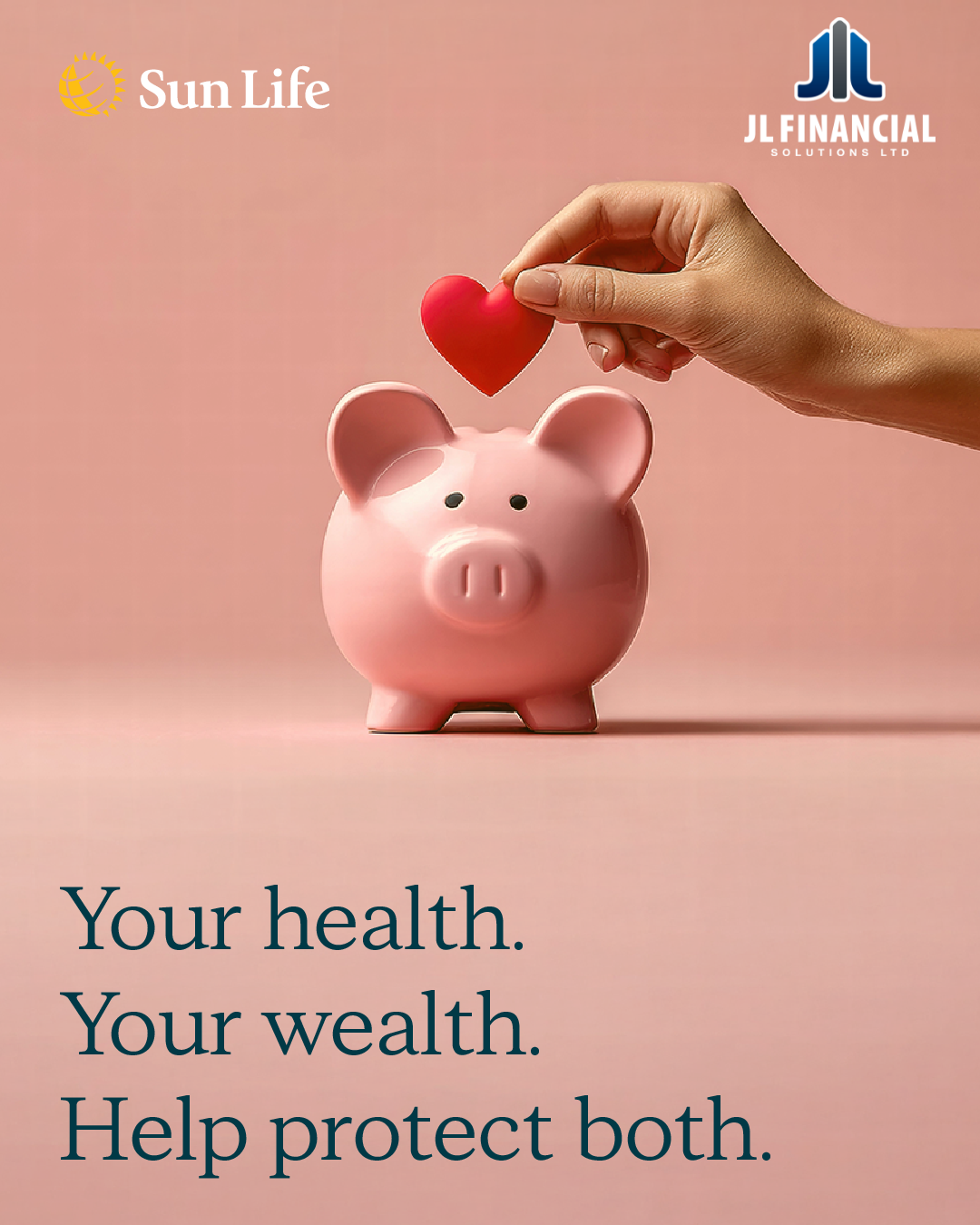

February is Heart Health Month. Heart disease affects 1 in 12 Canadian adults – a reminder of why protecting both your health and your financial wellbeing matters.

Critical illness insurance can help provide financial support when you need it most, helping you focus on recovery without the added stress of financial uncertainty. Connect with us to learn more.

Critical illness insurance can help provide financial support when you need it most, helping you focus on recovery without the added stress of financial uncertainty. Connect with us to learn more.

February is Heart Health Month. Heart disease affects 1 in 12 Canadian adults – a reminder of why protecting both your health and your financial wellbeing matters.

Critical illness insurance can help provide financial support when you need it most, helping you focus on recovery without the added stress of financial uncertainty. Connect with us to learn more.

Critical illness insurance can help provide financial support when you need it most, helping you focus on recovery without the added stress of financial uncertainty. Connect with us to learn more.

Watch video

Jonathan was a featured presenter at Sun Life Northern Alberta’s AGM yesterday in Edmonton, sharing perspective on why the client relationship matters before any product, strategy, or solution.

Trust isn’t built through transactions. It’s built through consistency, clarity, and professionalism.

Trust isn’t built through transactions. It’s built through consistency, clarity, and professionalism.

Jonathan was a featured presenter at Sun Life Northern Alberta’s AGM yesterday in Edmonton, sharing perspective on why the client relationship matters before any product, strategy, or solution.

Trust isn’t built through transactions. It’s built through consistency, clarity, and professionalism.

Trust isn’t built through transactions. It’s built through consistency, clarity, and professionalism.

We don't just work here. We live here.

Proudly serving Albertans with clear, experienced, accountable advice.

Proudly serving Albertans with clear, experienced, accountable advice.

We don't just work here. We live here.

Proudly serving Albertans with clear, experienced, accountable advice.

Proudly serving Albertans with clear, experienced, accountable advice.

Total Cost Reporting is changing what investors see.

Soon, your statement will show the full cost of your investments in dollars, not buried in percentages or fine print.

We have always disclosed fees upfront.

Clearly.

In plain language.

Not every advisor does.

If you’ve never reviewed this section of your statement or if you don't fully understand it, you’re not behind. You’re normal.

But transparency matters when you’re deciding whether the advice you’re getting is actually worth it.

Read the line that matters.

Then ask better questions.

Link in comments/bio

Soon, your statement will show the full cost of your investments in dollars, not buried in percentages or fine print.

We have always disclosed fees upfront.

Clearly.

In plain language.

Not every advisor does.

If you’ve never reviewed this section of your statement or if you don't fully understand it, you’re not behind. You’re normal.

But transparency matters when you’re deciding whether the advice you’re getting is actually worth it.

Read the line that matters.

Then ask better questions.

Link in comments/bio

Total Cost Reporting is changing what investors see.

Soon, your statement will show the full cost of your investments in dollars, not buried in percentages or fine print.

We have always disclosed fees upfront.

Clearly.

In plain language.

Not every advisor does.

If you’ve never reviewed this section of your statement or if you don't fully understand it, you’re not behind. You’re normal.

But transparency matters when you’re deciding whether the advice you’re getting is actually worth it.

Read the line that matters.

Then ask better questions.

Link in comments/bio

Soon, your statement will show the full cost of your investments in dollars, not buried in percentages or fine print.

We have always disclosed fees upfront.

Clearly.

In plain language.

Not every advisor does.

If you’ve never reviewed this section of your statement or if you don't fully understand it, you’re not behind. You’re normal.

But transparency matters when you’re deciding whether the advice you’re getting is actually worth it.

Read the line that matters.

Then ask better questions.

Link in comments/bio

What is high dividend-yield investing? A guide to passive income

High dividend yield investing works best when dividends are supported by earnings and cash flow, not declining share prices.

Yield alone doesn’t tell the full story. The source of the yield matters.

Yield alone doesn’t tell the full story. The source of the yield matters.

Wishing you a very Merry Christmas and a Happy New Year!

Wishing you a very Merry Christmas and a Happy New Year!

Have questions?

Here to help answer your questions, provide clarity about products and get you started on the road to achieving your goals.

We are contracted with Sun Life Financial Distributors (Canada) Inc., a member of the Sun Life group of companies. Mutual funds distributed by Sun Life Financial Investment Services (Canada) Inc.